By Jamie Murray, CFA

FINDING VALUE IN A MARKET NEAR RECORD HIGHS

One of the most common questions we receive is whether it still makes sense to invest when markets are trading near all-time highs.

It is a reasonable concern. Investors naturally worry about committing capital after a strong run in equity markets, only to experience a correction shortly thereafter. While short-term market movements are impossible to predict consistently, we understand why many investors hesitate when headlines focus on record index levels.

Our investment philosophy stems from a longer-term assessment of the value of a business rather than an attempt to forecast market direction. We agree that constantly chasing stocks at all-time highs can be a losing strategy. It misses the “buy low” part of the classic principle of “buy low, sell high.”

What is often overlooked is that while market indices may be reaching new highs, many individual businesses are not. Our research process is designed to identify high-quality companies trading below our assessment of their intrinsic value. Through ongoing portfolio reviews and disciplined rebalancing, we continually allocate capital toward opportunities where we believe future return potential remains attractive.

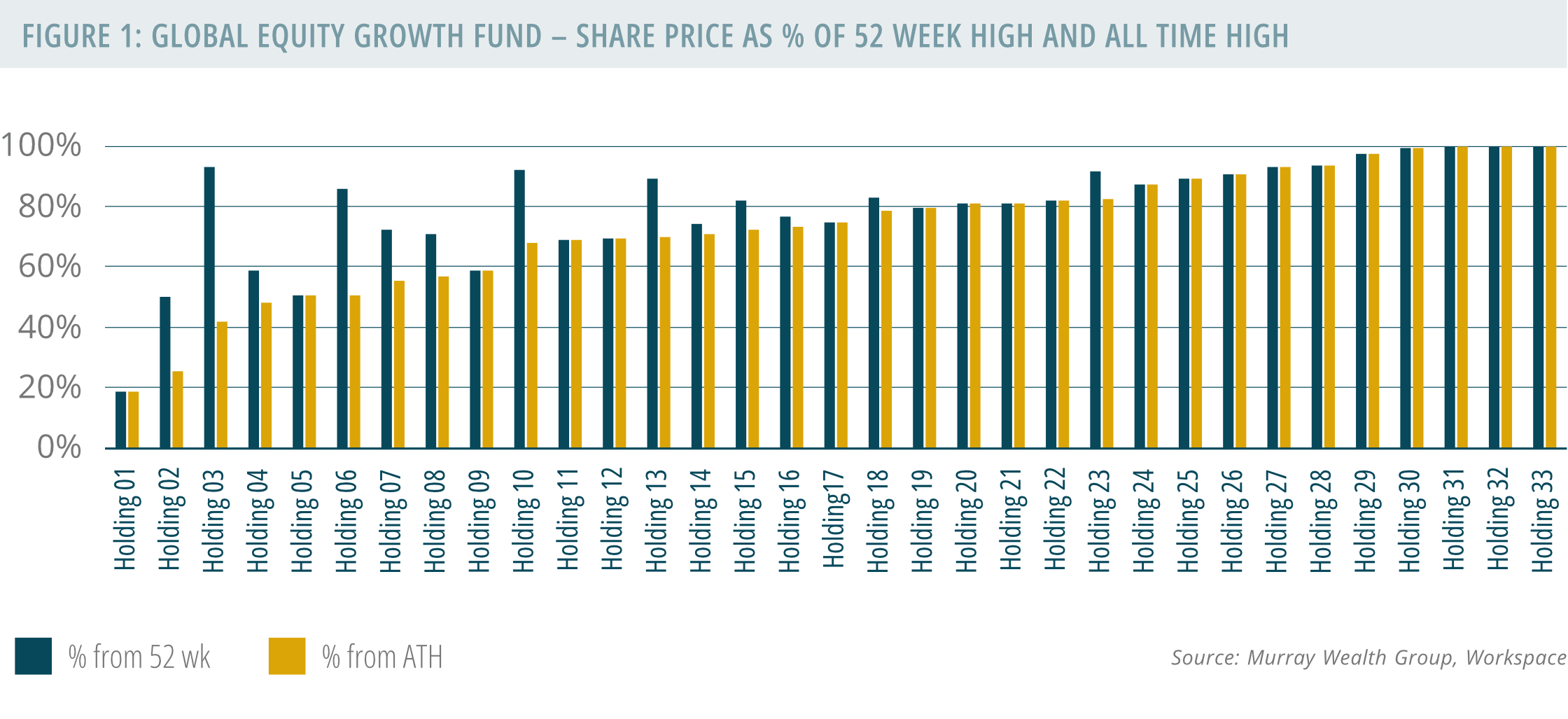

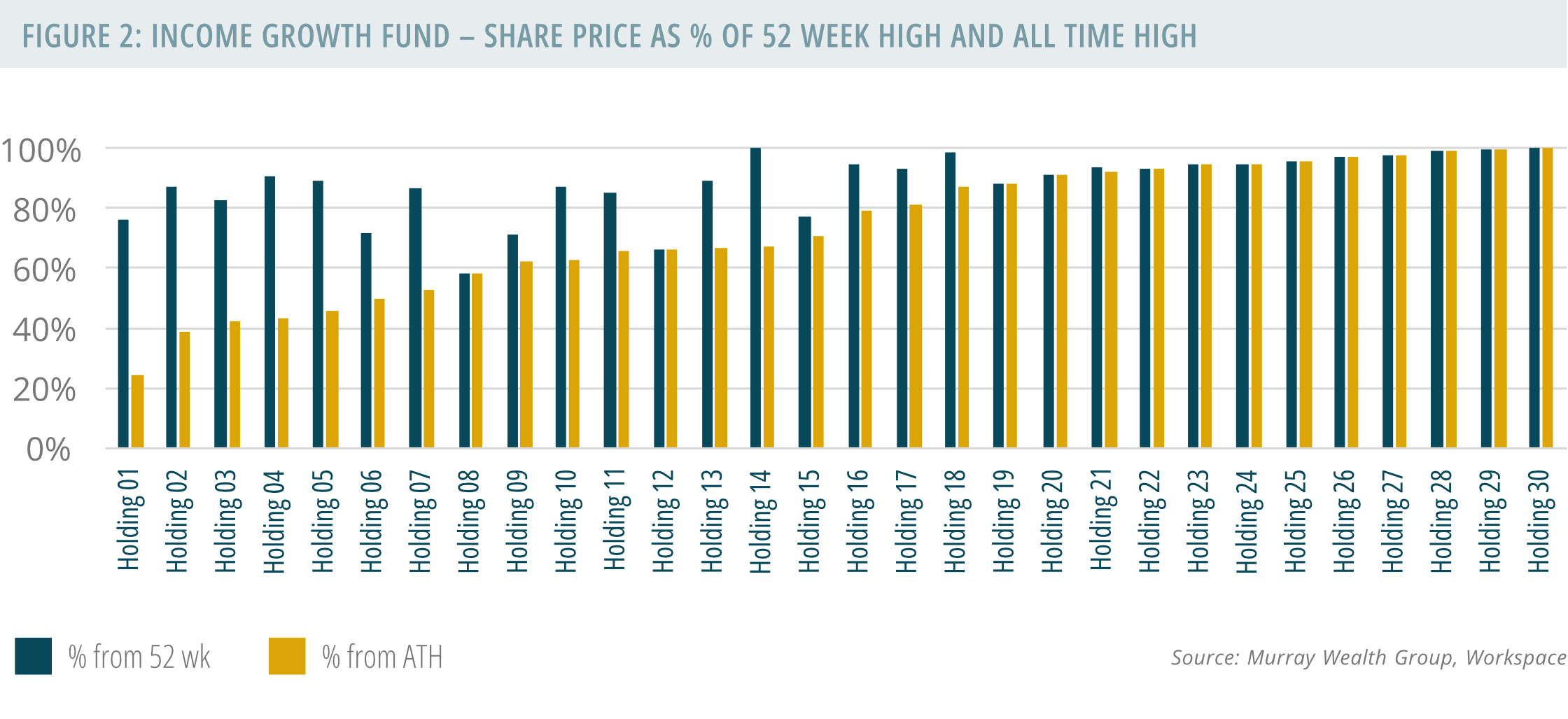

As our portfolios reached new highs at the end of May, we reviewed how each holding was trading relative to both its 52-week high and its all-time high. The results were revealing. Despite strong overall portfolio performance, the average holding in both funds continues to trade meaningfully below its historical peak valuation.

In other words, investors in our portfolios are not simply buying a collection of stocks trading at record highs. They are gaining exposure to businesses where we continue to see meaningful upside potential based on our assessment of long-term value.

This distinction is particularly important in today’s market environment, where much of the market’s recent performance has been concentrated within a relatively small group of companies, particularly those associated with artificial intelligence. While the market appears increasingly confident that the biggest AI winners have already been identified, we are less certain.

History suggests that transformative technologies create opportunities far beyond the companies developing them. The internet and mobile technology generated value across countless industries, and we believe artificial intelligence will follow a similar path. Many of the businesses best positioned to benefit from AI adoption are receiving far less attention than the companies currently dominating market headlines.

Figures 1 and 2 illustrate how holdings within both portfolios are currently trading relative to their 52-week highs and all-time highs. Within the Global Equity Growth Fund, the average holding is trading at approximately 80% of its 52-week high and roughly 73% of its all-time high. Companies such as Lululemon and Air Canada have traded at materially higher valuation levels in previous years and serve as examples of businesses where we continue to see attractive long-term opportunities despite recent market strength.

The Income Growth Fund exhibits a similar pattern. The average holding is currently trading at approximately 88% of its 52-week high and 74% of its all-time high. Although the fund has delivered strong performance over the past year and year-to-date, many holdings continue to trade below previous valuation levels.

We believe these observations reinforce an important point: record index levels do not necessarily mean attractive investment opportunities have disappeared. In many cases, the companies we own continue to trade well below previous valuation peaks despite improving business fundamentals and long-term growth prospects.

MARKET UPDATE

Equity markets continued their advance through May, with major U.S. indices reaching fresh all-time highs. The S&P 500 gained approximately 5% during the month, supported by strong corporate earnings and continued enthusiasm surrounding artificial intelligence. Market leadership remained highly concentrated, with technology and semiconductor companies accounting for a significant portion of overall gains.

The S&P/TSX Composite Index also moved higher, advancing approximately 2.6% during the month. While Canadian equities once again lagged their U.S. counterparts, financials and industrials provided support and helped offset weakness within the energy sector.

Commodity markets delivered mixed results. Crude oil prices declined by more than 12% as supply growth outpaced demand expectations and geopolitical concerns continued to ease. Precious metals paused following a strong start to the year, while industrial metals remained resilient, reflecting continued confidence in the broader economic outlook.

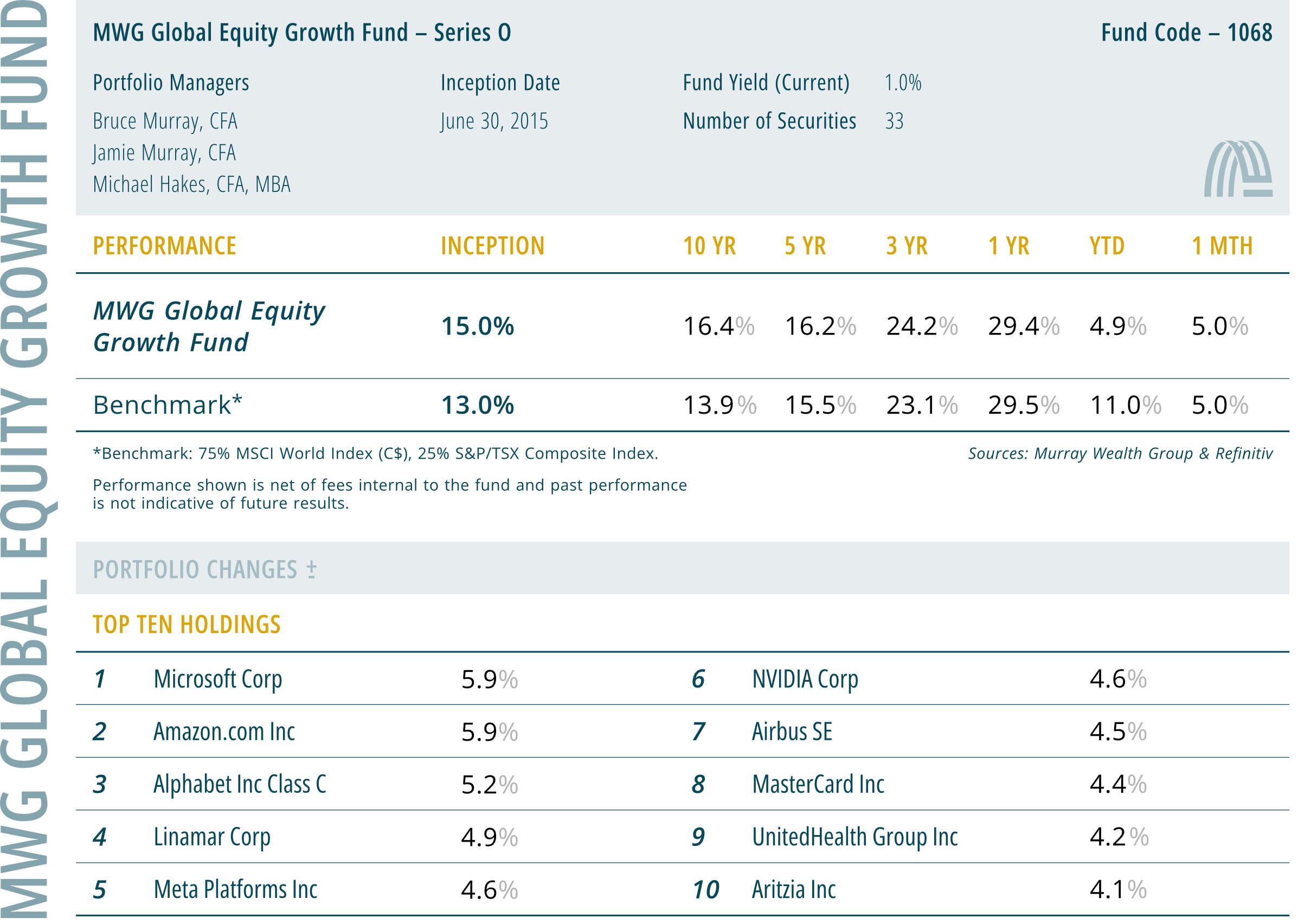

MWG GLOBAL EQUITY GROWTH FUND

The MWG Global Equity Growth Fund Series O returned 5.0% in May, matching the benchmark return for the month. The fund is up 4.9% percent year-to-date, compared to an 11% percent year-to-date return in the benchmark. Performance was supported by ServiceNow (+43%), Eli Lilly (+20%) and Air Canada (+18%). Detractors included Vital Farms (-26%), 3i Group (-12%) and Nu Holdings (-8%).

Portfolio Manager Summary

ServiceNow benefited from continued investor confidence in enterprise software and AI-enabled productivity solutions. Eli Lilly continued to gain momentum as demand for its diabetes and weight-loss treatments remained strong, while Air Canada benefited from improving travel demand and lower fuel costs.

The portfolio also benefited from improving market sentiment as geopolitical tensions eased. The ceasefire between Israel and Iran reduced concerns surrounding higher energy prices and their potential impact on consumer confidence and economic activity. Travel-related businesses were among the beneficiaries of this shift in sentiment.

While much of the market’s attention remains focused on the companies building artificial intelligence infrastructure, we continue to find opportunities among businesses positioned to benefit from AI adoption across the broader economy. Rather than pursuing the most crowded areas of the market, we are focused on companies where we believe the long-term benefits of AI are not yet fully reflected in share prices.

Our view remains that artificial intelligence will enhance productivity across most industries rather than render existing businesses obsolete. Companies such as Mastercard, Aon, Accenture, ServiceNow and Uber possess the scale, customer relationships, proprietary data and competitive advantages required to deploy AI effectively. In many cases, we believe the market is not fully recognizing the long-term value these businesses may create through improved efficiency, stronger customer engagement and enhanced profitability.

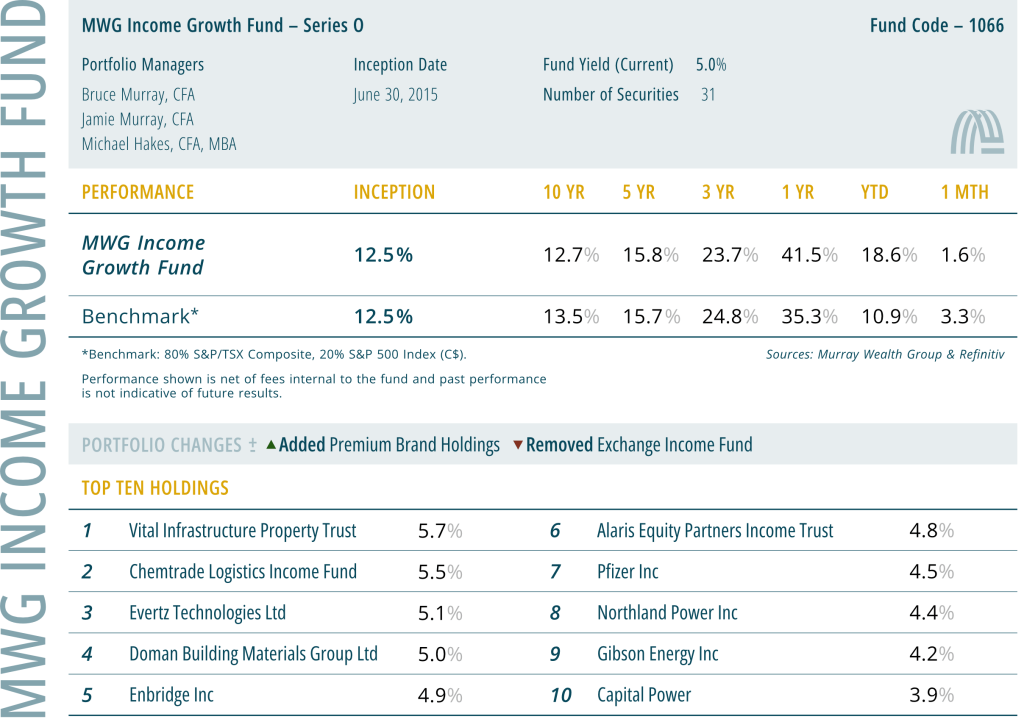

MWG INCOME GROWTH FUND

The MWG Income Growth Fund Series O returned 1.6% in May compared to the benchmark return of 3.3%. Despite trailing the benchmark during the month, the fund remains ahead on a year-to-date basis, returning 18.6% compared to 10.9% for the benchmark. May’s performance was driven by Power Corp (+10%), Exchange Income (+10%) and Capital Power (+9%). Weakness was seen in Wajax (-12%), PHX Energy (-11%) and BP (-10%).

Portfolio Manager Summary

Relative performance was impacted primarily by weakness within the energy sector, where the fund maintains an overweight position. Although energy prices softened during the month and geopolitical tensions eased, our long-term outlook for the Canadian energy sector remains positive.

We continue to favour midstream businesses that benefit from growing production volumes rather than relying solely on commodity price appreciation. Companies such as Enbridge, Pembina Pipeline and Gibson Energy remain well positioned to benefit from growing demand for transportation, storage and export infrastructure. We believe Canada will continue to play an increasingly important role in supplying energy and natural resources to global markets.

During the month, we initiated a position in Premium Brands Holdings, a diversified specialty food company with operations spanning prepared foods, specialty meats and food distribution. The shares have been under pressure due to weaker consumer spending, elevated beef prices, higher debt levels and a period of significant investment in new production capacity.

We believe many of these challenges are temporary. As utilization rates improve and recent investments begin contributing more meaningfully to earnings and cash flow, we expect financial performance to strengthen. The potential sale of certain distribution assets could further reduce debt and strengthen the balance sheet.

Premium Brands fits well within our investment philosophy of identifying high-quality businesses facing temporary challenges where the market may be underestimating future earnings power.