Jamie Murray, CFA, President

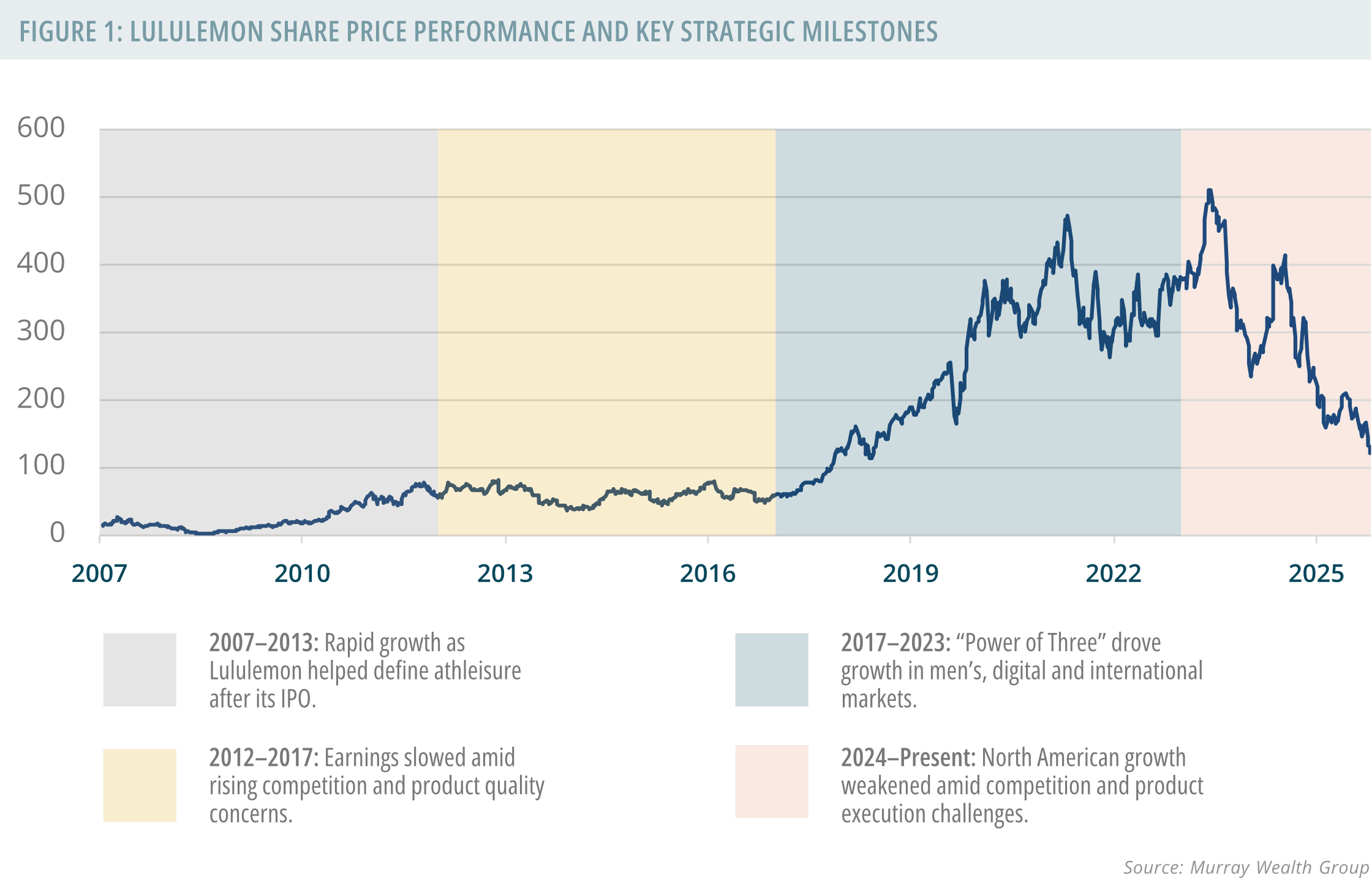

For more than a decade, Lululemon was one of the strongest growth stories in global retail. From its 2007 IPO through 2024, the company transformed from a niche yoga apparel brand into a global athleisure powerhouse. Its share price increased more than tenfold as the company expanded aggressively across North America and internationally, while helping define an entirely new category at the intersection of fitness, fashion and lifestyle.

Founder Chip Wilson has argued that Lululemon’s challenges are not primarily governance or scale issues, but rather issues tied to product innovation, technical credibility and cultural relevance. His proposed board nominees bring backgrounds more closely aligned with athletic apparel, creative brand-building and sport culture.

Meanwhile, the current board has emphasized operational discipline, governance and scaled global consumer-brand experience.

In many respects, the debate reflects a broader question facing the company: is Lululemon now primarily a mature global consumer brand, or is it still fundamentally a premium technical-athletic company that depends on product obsession, innovation and cultural relevance to maintain pricing power? In our opinion, the answer likely involves some combination of both.

Importantly, Lululemon’s success was never built on branding alone. The company established an early reputation for technical fabrics, comfort, fit and durability that resonated deeply with consumers. For years, competitors struggled to replicate the combination of premium positioning, community engagement and product credibility that allowed Lululemon to dominate the premium yoga and athleisure market.

More recently however, the company has lost momentum. Product misses, quality concerns, increased markdown activity and slowing North American growth have created pressure on margins and investor confidence. At the same time, newer competitors such as Alo Yoga and Vuori have gained traction by attacking different parts of the premium athleisure market. Alo has leaned further into fashion and cultural relevance, while Vuori has emphasized softness, comfort and technical versatility.

The market currently appears focused on what Lululemon has lost over the past several years as slower growth, weaker product cycles and increased competition have all contributed to a sharp change in sentiment around the stock. The more important question now is whether the brand still has the ability to reconnect with consumers in the way it once did. In our opinion, there are still enough signs of brand strength, customer loyalty and product credibility to suggest the answer may be yes.

The Brand’s Competitive Advantages Still Exist

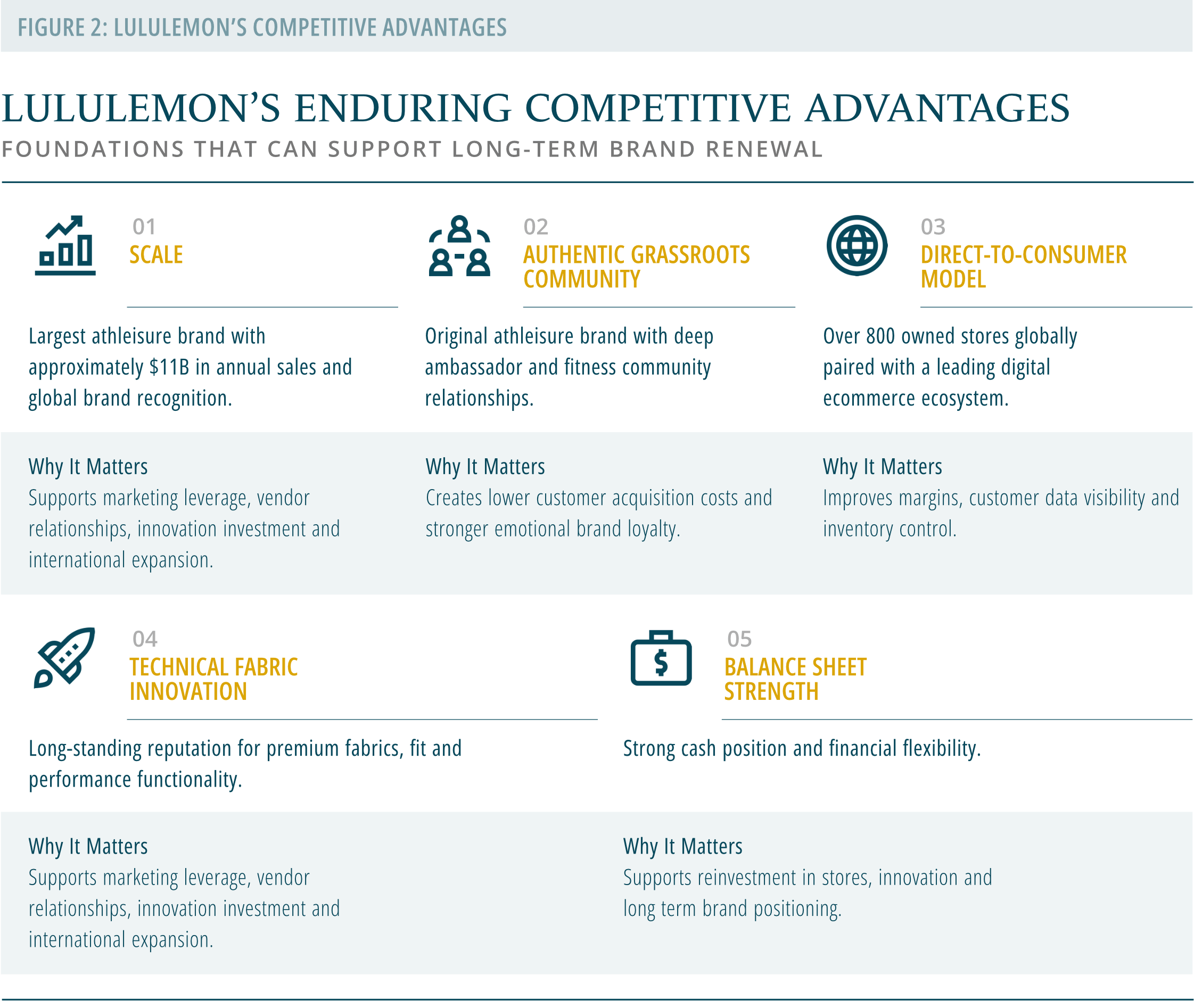

Despite the recent slowdown, Lululemon retains several competitive advantages that remain difficult to replicate at scale.

First, the company still operates from a position of financial strength. With approximately $11 billion in annual sales, a strong balance sheet and meaningful direct-to-consumer infrastructure, Lululemon retains the flexibility to reinvest in product development, store experience and brand positioning.

Second, the company continues to own one of the strongest direct-to-consumer ecosystems in global apparel retail. Unlike many competitors that rely heavily on wholesale distribution, Lululemon controls most of its customer experience through owned stores and digital commerce channels. This provides advantages in customer data, inventory management, merchandising control and long-term margin structure.

Third, the company still maintains meaningful technical credibility in athletic apparel. While competitors have narrowed the gap, Lululemon remains associated with premium fabrics, functional performance and fit innovation in a way many fashion-oriented athleisure brands do not.

Most importantly, the brand itself still carries significant value. Consumers have not abandoned premium athleisure, nor have they abandoned wellness-oriented lifestyle spending. The broader secular trends that helped drive Lululemon’s rise including health, fitness, hybrid work and comfort-driven apparel remain firmly intact.

The key question is not whether consumers still want premium athletic apparel. The key question is whether Lululemon can restore the technical innovation, product excitement and cultural relevance that originally made the brand dominant.

Refocusing on Core Does Not Mean Standing Still

One of the more important strategic debates surrounding Lululemon today is what it actually means to “return to core.” We believe this should not be interpreted as simply selling more of the same products with incremental seasonal adjustments. The real opportunity is to re-establish Lululemon’s core franchises as innovation platforms.

Products such as Align, ABC, Scuba and Wunder Train became successful because they solved specific consumer needs better than competitors. The opportunity now is to evolve those franchises through improved technical performance, stronger fit consistency, fabric innovation and more disciplined product storytelling.

The strongest premium brands rarely abandon their icons. Instead, they continuously elevate and refresh them. For Lululemon, the opportunity is not to dramatically reinvent the brand, but rather to make the core product assortment feel technically and culturally exciting again.

As we see it, the core is not stale because it is core. The core feels stale because it has not been sufficiently re-authored.

Premium Brands Have Recovered Before

The retail industry has seen several premium brands lose momentum, only to successfully reposition themselves through sharper product focus, stronger storytelling and improved operational discipline. In our opinion, Lululemon’s current position compares favourably to a number of those historical turnaround situations because the company still retains strong financial flexibility, premium pricing power and meaningful customer loyalty.

Three examples stand out in particular: Ralph Lauren, Tapestry and Abercrombie & Fitch. Each faced different challenges, but all three demonstrate how premium consumer brands can recover when management refocuses the business around product relevance, customer engagement and brand clarity.

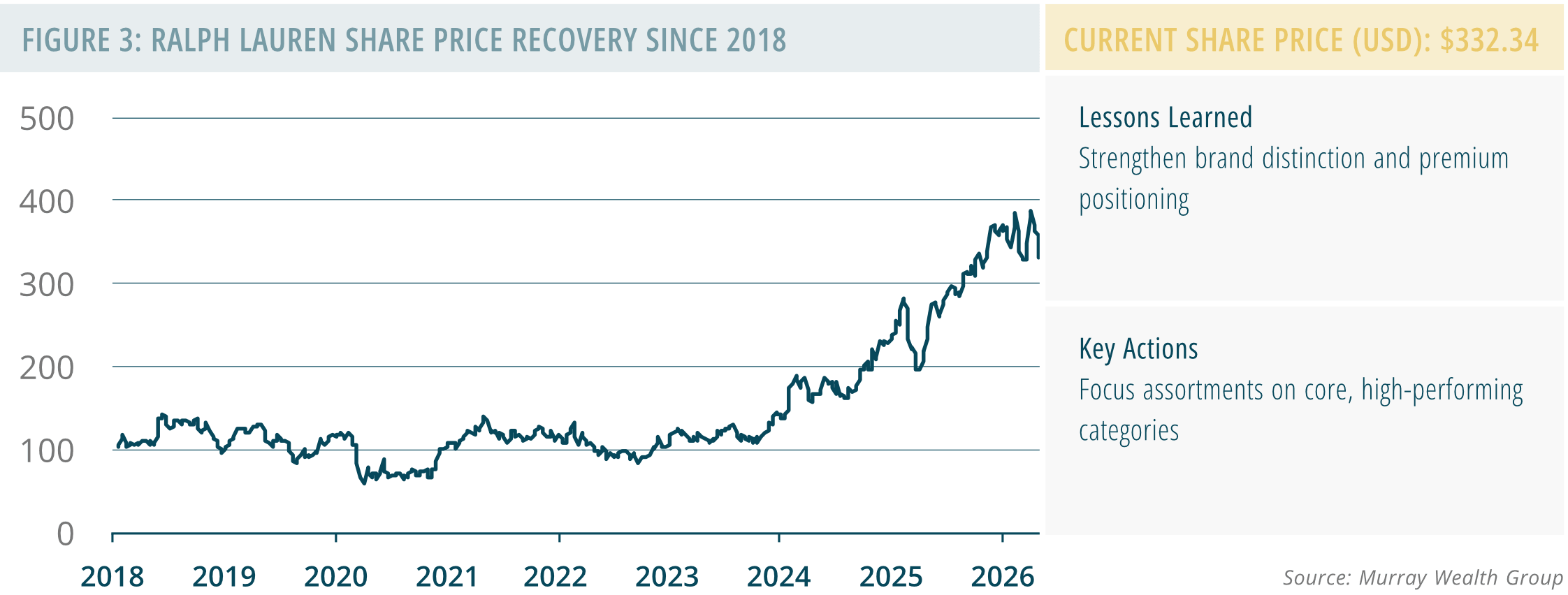

Ralph Lauren: Rebuilding Brand Elevation

Ralph Lauren’s challenge was largely tied to overexposure. Years of discounting, department store distribution and outlet expansion weakened the exclusivity that once defined the brand. Iconic products such as Polo shirts became increasingly commoditized and frequently appeared in off-price retail channels.

The company responded by rebuilding scarcity, reducing discounting and elevating its core product franchises. Importantly, Ralph Lauren did not abandon the products most associated with the brand. Instead, it improved the storytelling, tightened distribution and repositioned those products within a more premium framework.

There are clear similarities to Lululemon’s current situation. Products such as Align, ABC and Scuba remain highly recognizable consumer franchises, but some of the exclusivity and product excitement surrounding them has faded in recent years. A more disciplined product strategy focused on technical innovation, tighter merchandising and reduced markdown activity could help restore some of the premium positioning that originally differentiated the brand. In many respects, the lesson from Ralph Lauren is not to abandon the core product assortment. The lesson is to make the core feel elevated again.

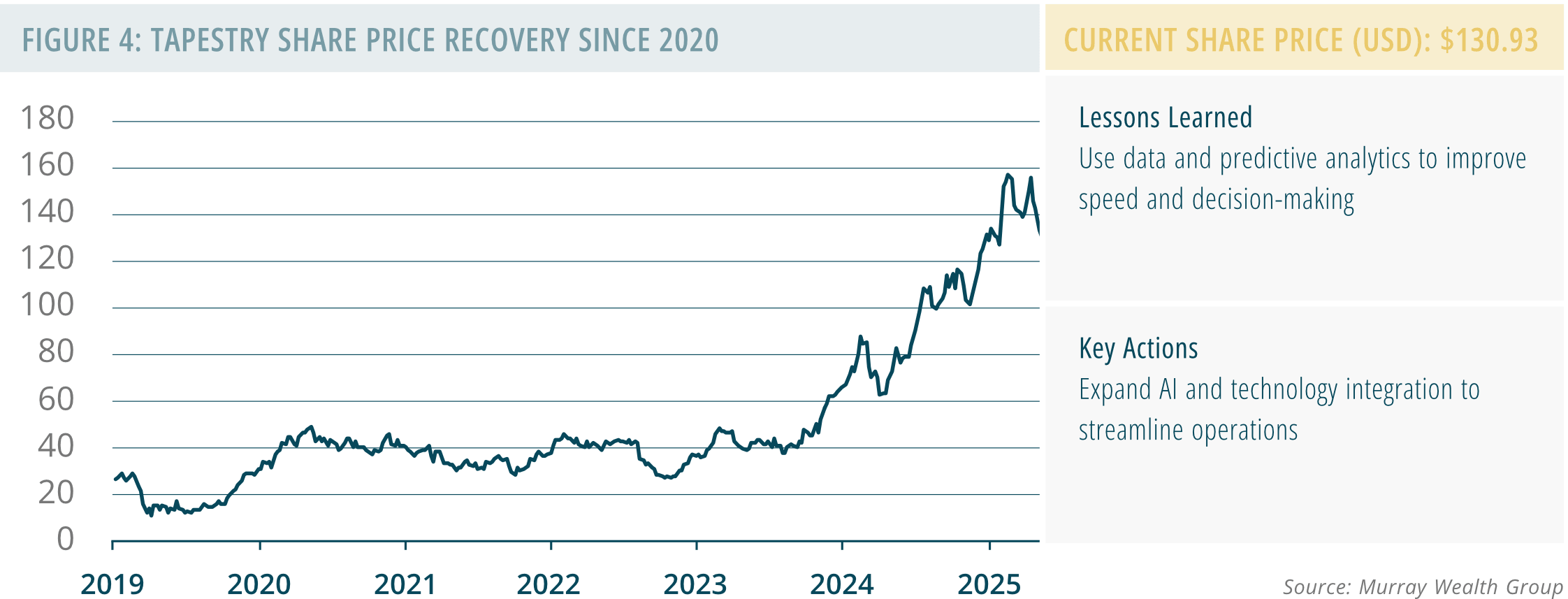

Tapestry: Using Data and Speed to Regain Relevance

Tapestry faced a different challenge. Brands such as Coach and Kate Spade had become overly reliant on outlet distribution, logo-heavy products and slower product cycles that struggled to keep pace with changing consumer preferences.

The company responded by leaning more aggressively into customer data, predictive analytics and faster product development cycles. By improving personalization and shortening design-to-market timelines, Tapestry became more responsive to consumer trends while also improving inventory discipline.

Lululemon already possesses many of the structural advantages Tapestry had to build toward. Its direct-to-consumer model provides access to significant customer data, while its digital ecosystem and membership base create opportunities for deeper customer engagement and faster feedback loops.

In our opinion, one of the more important opportunities for Lululemon over the next several years may involve using technology and customer data more effectively to improve product innovation cycles, inventory planning and consumer targeting. The company does not necessarily need to become more fashion-driven, but it may need to become faster, more precise and more responsive to shifting consumer preferences.

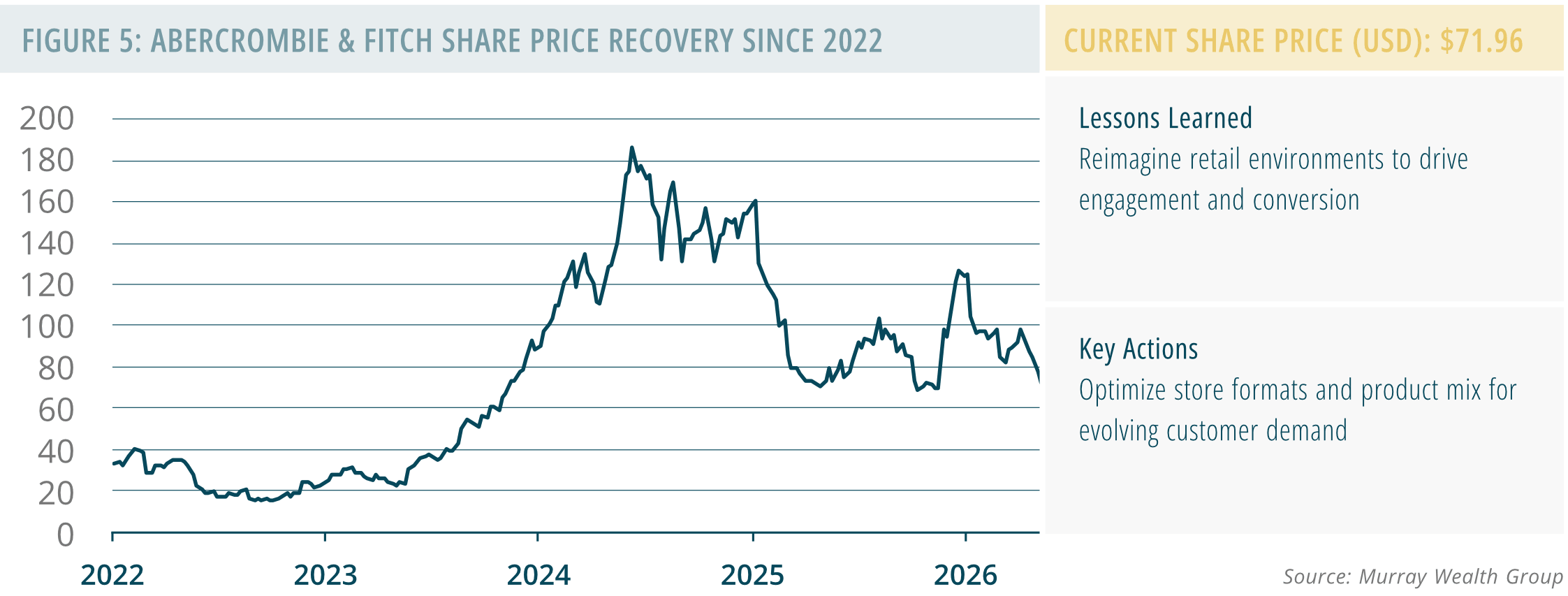

Abercrombie: Repositioning the Brand for a New Consumer

Abercrombie & Fitch’s turnaround may be the most dramatic of the three. By the mid-2010s, the brand had become heavily associated with a narrow early-2000s identity that increasingly felt out of touch with younger consumers. Store environments, merchandising and marketing all contributed to a perception that the brand had become stale and culturally disconnected.

Management responded by modernizing the product assortment, improving store presentation and repositioning the brand around a more inclusive and contemporary lifestyle identity. The company also invested heavily in store upgrades and clearer merchandise segmentation.

While Lululemon’s situation is far less severe, there are still useful parallels. As competition within athleisure has intensified, consumers now have far more alternatives across performance apparel, wellness wear and lifestyle-focused athletic brands. Maintaining relevance increasingly requires more than simply offering technically functional products. It also requires a strong emotional and cultural connection with consumers.

Lululemon’s local ambassador network, community positioning and experiential retail model remain important strengths. Reinvesting in those areas while modernizing store environments and refining merchandise storytelling could help the company reconnect more effectively with consumers, particularly in North America where growth has slowed most meaningfully.

Why We Believe Lululemon Still Has a Path Forward

Lululemon’s recent challenges should not be dismissed. Slowing North American growth, increased competition and product inconsistency are meaningful concerns.

At the same time however, the company still possesses many of the characteristics often present in successful premium-brand recoveries including a globally recognized brand, strong financial flexibility, a loyal customer base, meaningful direct-to-consumer infrastructure, technical product credibility and multiple long-term international growth opportunities.

The market currently appears focused on what Lululemon has lost over the past several years. The more important question may be what the company is still capable of rebuilding.