As autonomous vehicles move from concept to commercial reality, Uber may be uniquely positioned to become one of the most important physical AI platforms in the world.

Since the launch of ChatGPT in November 2022 brought large language models into the mainstream, most AI workloads have been defined by digital output. Whether generating text, images, recommendations, analysis, software code or agentic workflows, the end product has largely been bits on a screen. Most of the trillions of dollars that has gone into datacenter investment is targeting this output, aiming to replace or augment knowledge-based systems.

Behind this investment, however, the next leg of AI is already beginning to emerge. Physical AI refers to AI systems that produce real-world outcomes. Autonomous vehicles, factory automation and surgical robotics represent the intersection of AI models and physical output.

We believe physical AI will represent the next wave of the AI trade.

The challenge for investors is identifying where that value will ultimately accrue. In many cases, physical AI may simply improve existing processes. A factory becomes marginally more efficient. A tractor applies fertilizer more precisely. Useful innovations, certainly, but not necessarily transformational from an investment perspective.

A great investment needs to represent a step change in growth or profitability. We believe Uber represents one of the best investments to gain exposure to this theme.

We detailed Uber’s strong operations and financials in our previous article, Riding the Wayve: The Impact of Autonomous Vehicles on Uber, Nvidia and Microsoft. Despite financial results remaining largely in line with our original investment thesis, Uber’s Gross Merchandise Value, or total spend on its platform, has grown approximately 60% since 2023, and the shares have remained rangebound.

The culprit is Google’s autonomous vehicle division, Waymo, which is scaling rapidly and receiving rave reviews. We detailed why Waymo may be more foe than friend in that earlier note, when we wrote:

“If only one company (for example, Waymo) is able to commercialize AV technology, most of the value will likely accrue to it. Waymo would have all the power, given its ability to decide how to monetize the technology. For example, Waymo could exclusively serve its own ridesharing app and attract riders away from Uber with lower priced fares. This is certainly the worst-case outcome for Uber.”

At the time, this represented the central risk to the investment thesis. If autonomous driving evolved into a winner-take-all market, Uber could find itself disintermediated by the technology providers themselves.

Nearly two years later, Waymo remains the only robotaxi company operating at meaningful scale and continues to be the primary pushback against the Uber investment case. However, we believe the next five years will demonstrate why these concerns are misplaced and how Uber can emerge as one of the dominant physical AI companies globally.

Although Uber maintains partnerships with Waymo in Austin and Atlanta, the company’s autonomous vehicle strategy extends well beyond Waymo.

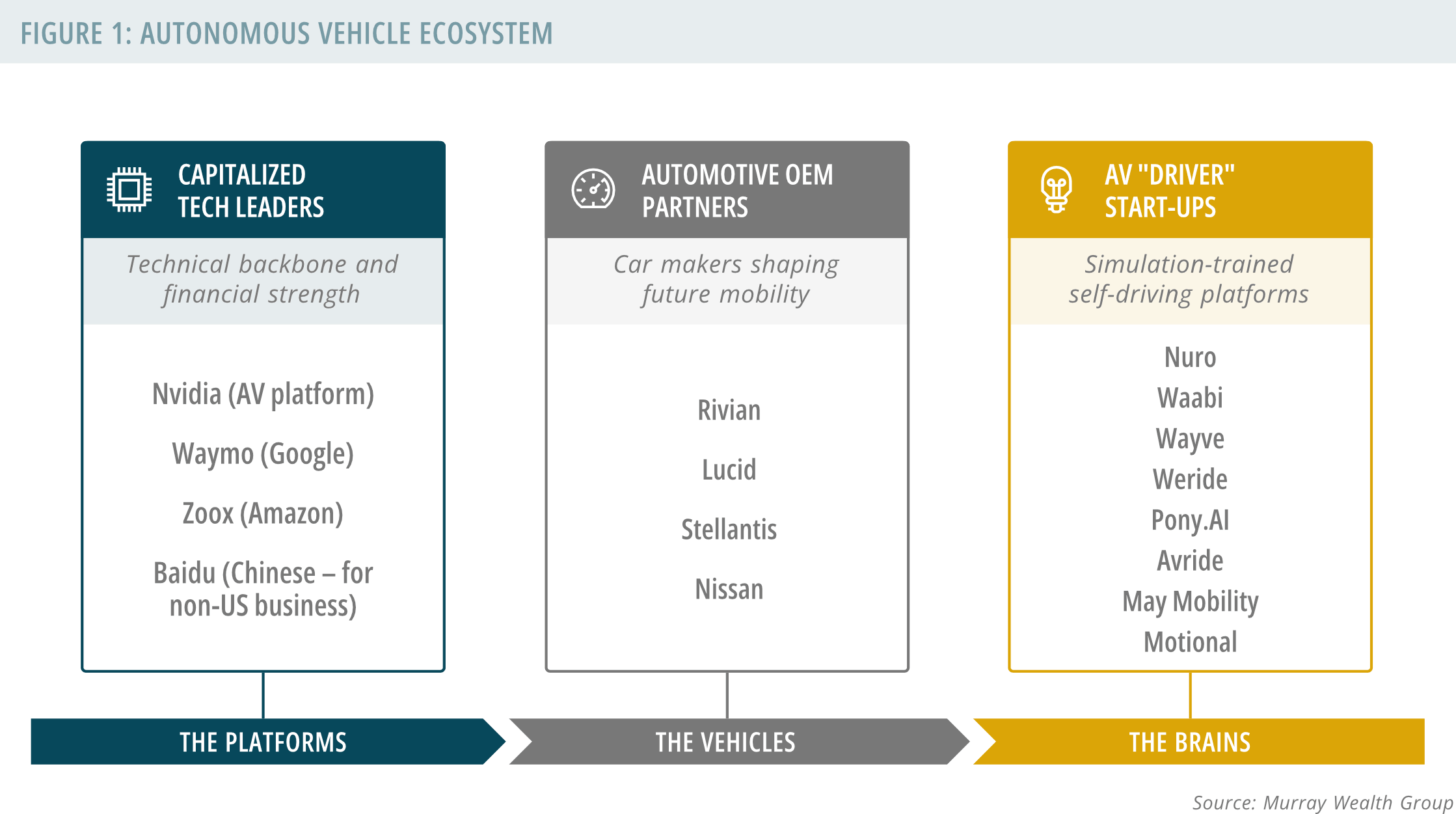

We estimate that Uber maintains ownership interests, investment partnerships or platform relationships with thirteen leading autonomous vehicle companies globally. These relationships span technology companies, automotive manufacturers and autonomous driving software developers, providing Uber with exposure to a broad range of technologies and operating models. We wrote about one of these companies, Wayve, last September.

For the purposes of this discussion, we group Uber’s autonomous vehicle partners into three categories: capitalized technology leaders, automotive OEM partners and AV driver start-ups.

Capitalized Technology Leaders: Companies with the technical backbone and financial resources required to commercialize autonomous transportation at scale, including Nvidia, Waymo, Zoox and Baidu.

Automotive OEM Partners: Vehicle manufacturers seeking to maintain relevance in the future of mobility, including Rivian, Lucid, Stellantis and Nissan.

AV Driver Start-Ups: Companies focused on developing the software and simulation environments that train autonomous driving systems, including Nuro, Waabi, Wayve, WeRide, Pony.ai, Avride, May Mobility and Motional.

Each brings a unique capability to the ecosystem, whether manufacturing expertise, hardware technology or autonomous driving software. What these companies generally lack is a direct relationship with riders. Uber’s platform provides access to demand at scale, helping bridge the gap between technological capability and commercial deployment.

The race to commercial operations is now underway.

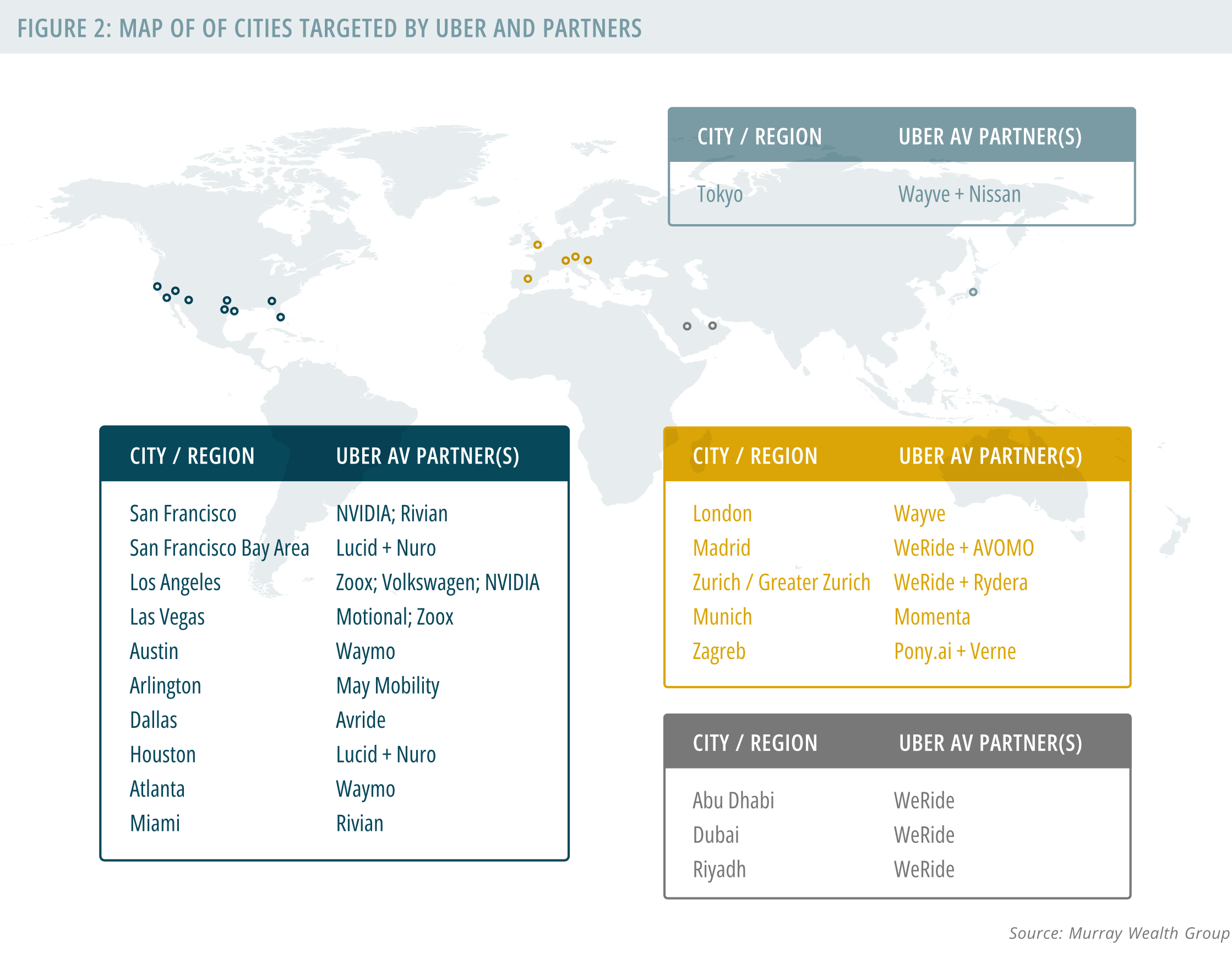

Waymo is targeting approximately 25 U.S. cities by the end of 2026 and could potentially expand to 40–50 cities by the end of 2028. Uber and its partners are expected to be active in roughly 15 cities globally by year-end 2026 and are targeting approximately 28 cities from the Nvidia partnership alone by 2028. Additional large-scale partnerships with Nuro, Lucid, Waabi and WeRide could ultimately bring Uber’s autonomous vehicle footprint in line with Waymo’s.

We believe the key question is where value ultimately accrues within the autonomous vehicle ecosystem. While considerable attention is focused on the companies developing the technology itself, Uber continues to strengthen its position as the marketplace connecting riders with autonomous transportation providers. As autonomous fleets scale, that position could become increasingly valuable.

Figure 2 highlights the geographic footprint Uber, and its autonomous vehicle partners, are targeting over the next several years.

Beyond Robotaxis

While robotaxis represent the most visible physical AI opportunity, we also see meaningful potential for Uber to apply autonomous technologies across its delivery business.

The company is already piloting sidewalk delivery robots in select markets, but the broader opportunity extends well beyond sidewalks and could eventually include autonomous road transportation and even aerial delivery.

Sidewalk Delivery Robots

Early pilot programs demonstrate how automation can improve efficiency along dense urban delivery routes while reducing delivery costs.

Autonomous Road Vehicles

Uber is supporting the development of self-driving delivery and freight solutions through partnerships with autonomous trucking companies such as Waabi and Aurora. Pilot programs are already underway in the Texas-to-Phoenix freight corridor.

Drone Delivery

By the end of the decade, advances in battery technology could make drone delivery economically viable in select markets where faster fulfillment carries a meaningful premium. Smaller high value items will initially be in focus with industrial and rural deliveries likely the near term uses

Where Value Ultimately Accrues

Physical AI has the potential to become the next major phase of artificial intelligence adoption.

While much of the market’s attention remains focused on digital AI applications and the infrastructure supporting them, autonomous transportation represents one of the clearest examples of AI creating tangible, real-world economic value.

For Uber, the opportunity extends beyond simply participating in autonomous transportation. By positioning itself as the marketplace connecting riders, vehicles and technology providers, the company may be building one of the most scalable physical AI platforms in the world.

Much of the current discussion around autonomous vehicles continues to focus on the risks they may present to Uber’s existing business model. Our view is that the company’s expanding network of partnerships and marketplace position may allow it to participate meaningfully in the growth of autonomous transportation over the coming decade.