By: Jamie Murray, CFA

Real estate has long been defined by a simple principle: location matters. Investors instinctively gravitate toward assets in established, high-demand markets, whether that is a beachfront property or a well-positioned hotel in a central district. What ultimately defines a “prime” location is the balance between supply and demand. Strong demand paired with limited availability tends to support both pricing and long-term value.

Over time, however, markets adjust. Rising prices attract new development, and what was once considered secondary can quickly evolve into the next area of focus. A nearby stretch of undeveloped coastline, or a newer, more modern asset can shift demand patterns in meaningful ways. This constant rebalancing is what creates opportunity for disciplined investors.

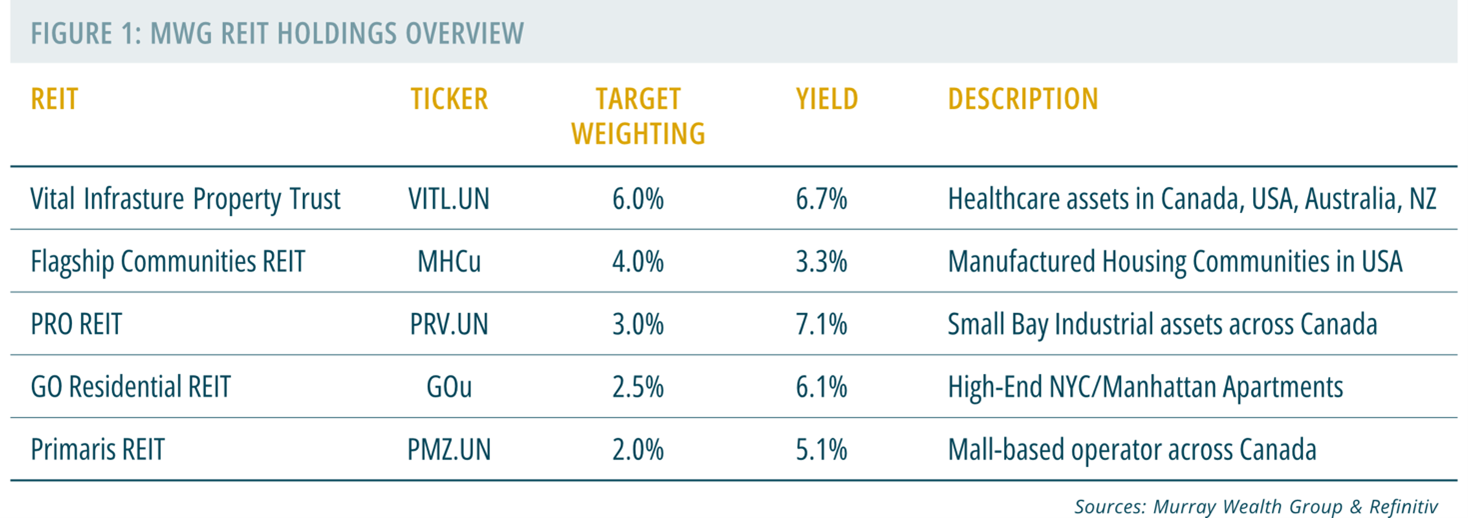

Within the MWG Income Growth Fund, we focus on high-quality income-generating businesses that also offer underappreciated growth potential. In recent months, we have been identifying compelling opportunities within the Real Estate Investment Trust (REIT) sector. Specifically, we are finding value in REITs where units trade at a discount to underlying property values, and where supply and demand dynamics within specific sub-sectors remain favourable.

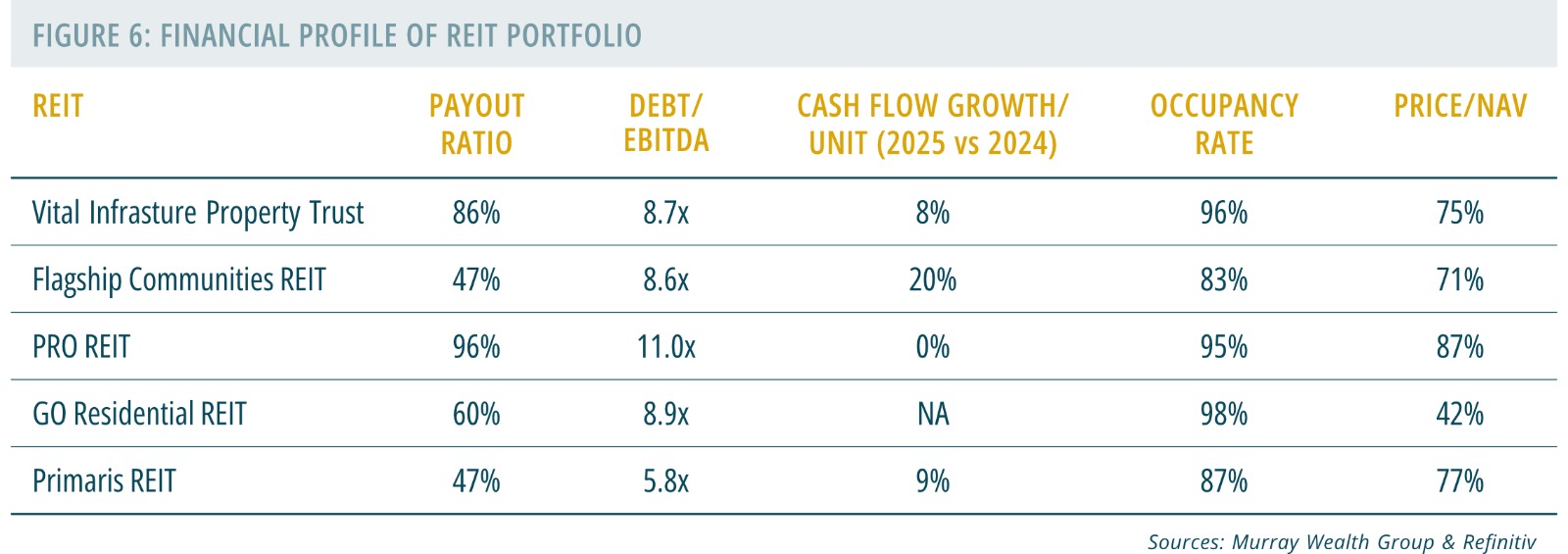

We have maintained positions in Vital Infrastructure Property Trust (formerly Northwest Healthcare Trust), PRO REIT, and Flagship Communities for several years. More recently, in February, we added positions in Primaris REIT and GO Residential REIT. In the sections that follow, we outline the underlying market dynamics that support our investment thesis across each of these holdings.

Vital Infrastructure Property Trust: Defensive Income in Healthcare Real Estate

Overview

Vital has sold numerous assets worldwide to simplify its business and reduce debt since we first published our views in late 2024. Meaningful steps have been taken to simplify its business and strengthen its balance sheet through the sale of non-core assets globally. As a result, the company is now better positioned to shift from restructuring toward disciplined growth. With established expertise in healthcare infrastructure, Vital is increasingly focused on partnering with healthcare authorities across Canada on new hospital development projects, an area where barriers to entry remain high.

Supply

Hospital infrastructure remains both capital-intensive and structurally undersupplied across developed Western economies. The significant cost, regulatory complexity, and long development timelines limit the pace of new supply, allowing new projects to be absorbed relatively quickly. While certain adjacent segments, such as smaller medical office buildings or outpatient facilities, may experience more supply elasticity, particularly in markets with private healthcare participation, core hospital assets continue to benefit from constrained supply dynamics.

Demand

Demand for healthcare infrastructure is inherently resilient. It is largely insulated from economic cycles and supported by long-term demographic trends, most notably aging populations. This stability is reflected in Vital’s operating metrics, including an 88 percent lease renewal rate, an average lease term of approximately 12 years, and minimal credit risk, with expected credit losses below 0.5 percent of rent. Together, these factors contribute to a highly predictable income profile.

Flagship Communities REIT: Structural Supply Constraints in Affordable Housing

Overview

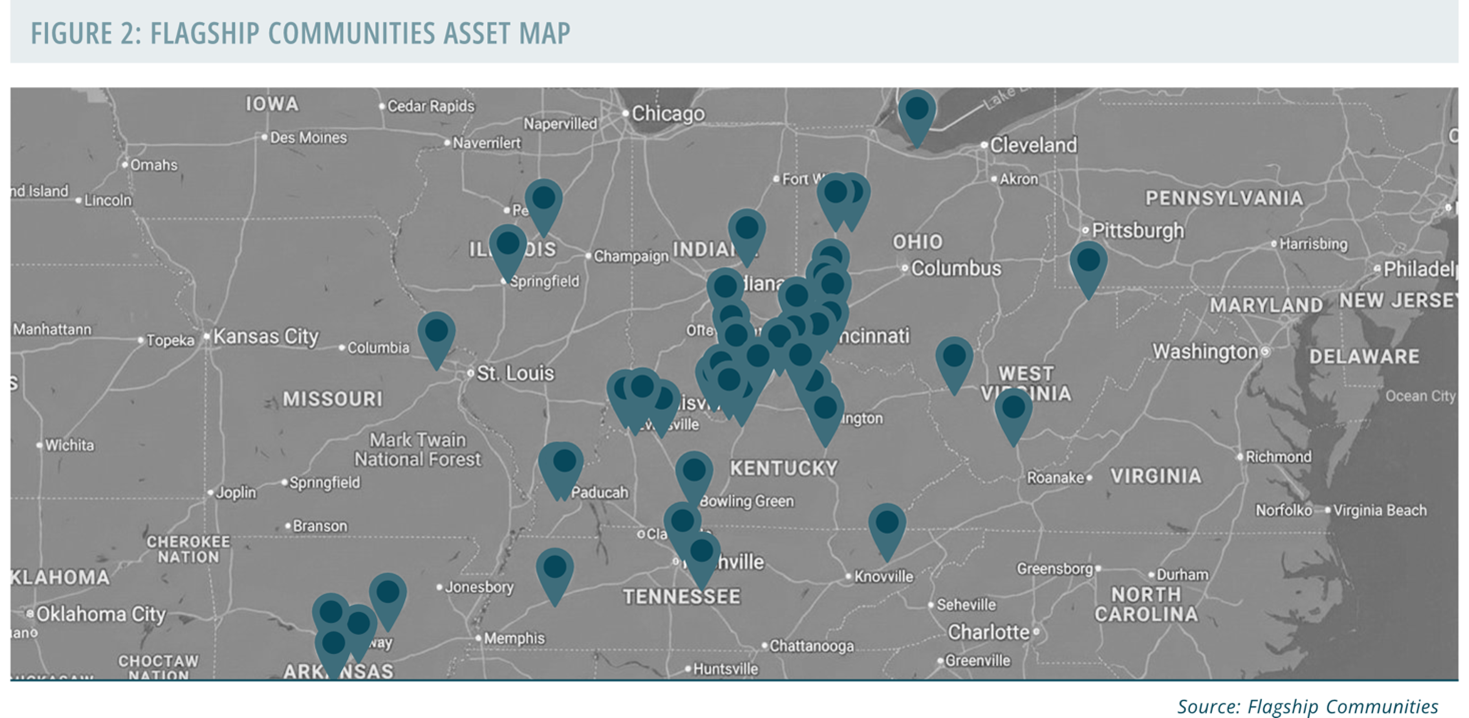

Flagship Communities REIT owns and operates manufactured housing communities across the U.S. Midwest and Southeast. We view this as an attractive and often overlooked segment of the residential market. Unlike traditional multi-family assets, Flagship primarily collects lot rental fees, which significantly reduces ongoing capital requirements, as residents own and maintain their homes. The company has also established itself as an effective consolidator within a highly fragmented market, acquiring smaller, independently operated communities and improving occupancy, operations, and overall asset quality over time.

Supply

New supply in manufactured housing remains exceptionally limited. The majority of existing communities were developed in the 1960s and 1970s, and new development has been constrained for decades. Zoning restrictions, local opposition, relatively low property tax generation compared to higher-density housing, and rising infrastructure costs have all contributed to a structurally undersupplied market across Flagship’s operating regions.

Demand

Demand continues to be supported by persistent housing affordability challenges. Manufactured homes offer a pathway to ownership at a meaningful discount, often 30 to 50 percent below the cost of traditional housing. Flagship’s communities are typically located near major urban centres such as Cincinnati, Nashville, and Louisville, serving lower- to middle-income households with stable employment in sectors including government, healthcare, and essential services. Once a home is placed on-site, the cost and complexity of relocation create meaningful friction, supporting high occupancy levels and enabling consistent, incremental rent growth over time.

PRO REIT: Small-Bay Industrial Assets and Structural Supply ConstraintsOverview

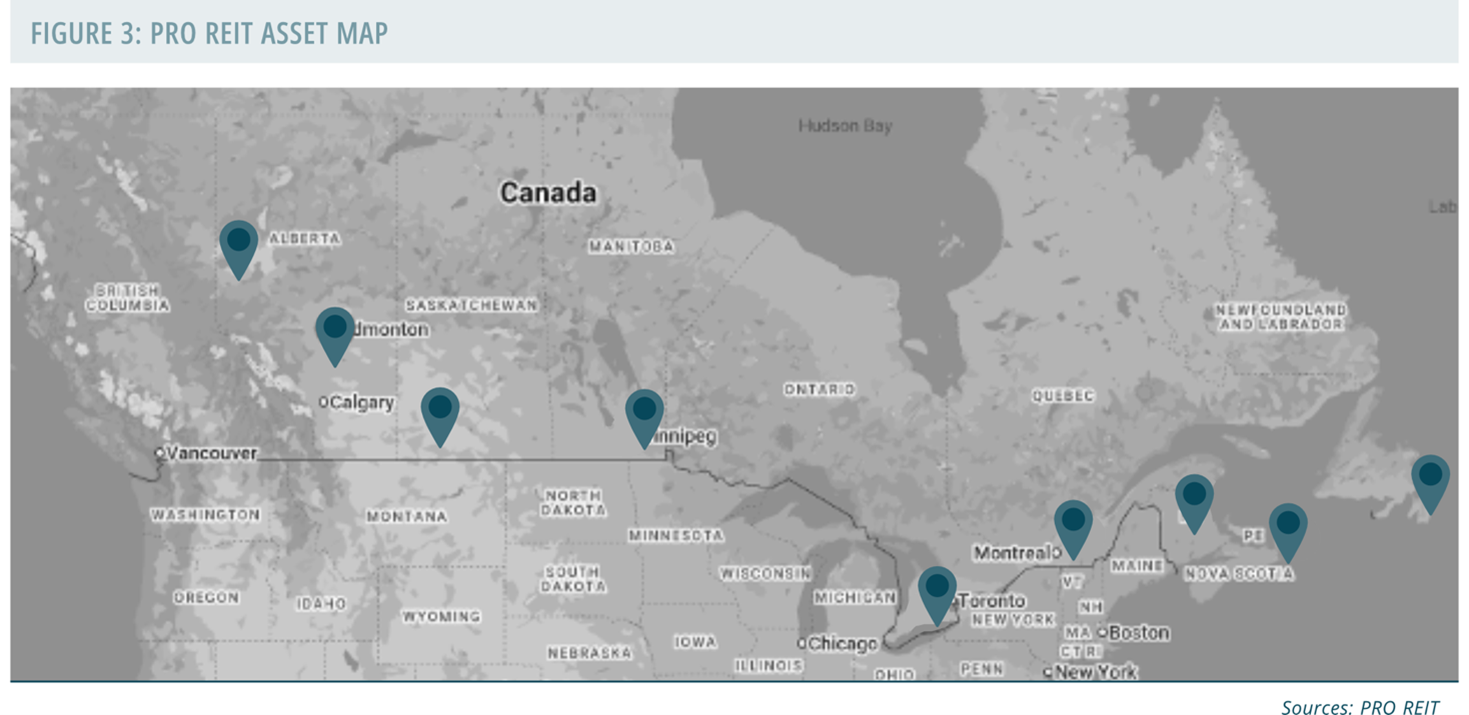

PRO REIT is a leading pure-play industrial platform, with small- to mid-bay assets representing over 90 percent of base rent as of early 2026. Unlike large, highly automated distribution centres that are more exposed to global trade flows, these properties function as essential urban infrastructure—supporting low-cost storage, light manufacturing, and service-based operations. The portfolio is strategically concentrated in high-conviction secondary markets such as Halifax, anchored by the Burnside Industrial Park, and Winnipeg, where PRO REIT has established itself as one of the largest industrial landlords. These locations benefit from proximity to key port and rail infrastructure, positioning the portfolio to capture localized, last-mile demand that larger-format facilities are less able to serve efficiently.

Supply

The small-bay industrial segment is characterized by a persistent imbalance between supply and demand. Historically dominated by fragmented ownership, the sector is now attracting increased institutional attention. However, the economics of new development remain challenging. Construction costs for small-bay assets are typically higher on a per-square-foot basis than large-scale logistics facilities, often ranging from $160 to $220 per square foot. This reflects the added complexity of demising walls, HVAC systems, and electrical infrastructure across multiple units. As a result, new supply remains constrained, particularly in land-limited urban markets, while existing assets, many of which are older, often trade below replacement cost. This dynamic creates durable barriers to entry and reinforces the competitive positioning of established operators such as PRO REIT.

Demand

Demand for small-bay space is highly diversified and operationally driven. Units are leased to a broad base of local businesses, including contractors, light industrial operators, and specialty distributors. This tenant mix tends to produce more stable cash flows, with less direct exposure to the volatility seen in consumer-driven logistics and large-scale distribution networks. This resilience is reflected in recent performance. As of Q4 2025, PRO REIT reported industrial same-property NOI growth of approximately 9 percent, with 2026 lease renewals achieving average rental spreads exceeding 33 percent. Tenants typically view these spaces as integral to their operations, valuing proximity to customers and affordability. As a result, rent is often treated as a non-discretionary business expense, supporting strong retention and consistent rental growth.

GO Residential REIT: Supply Constraints and Rent Growth in Manhattan

Overview

GO Residential REIT is a recently listed platform focused on modern apartment assets in New York City. The REIT was founded by Joshua Gotlib and Meyer Orbach, who retain meaningful ownership and have continued to acquire units in the open market, reinforcing alignment with unitholders. Recent unit price performance has been impacted by negative headlines and policy uncertainty in New York, including ongoing discussions around taxation and housing affordability initiatives. However, we believe these factors have created a disconnect between sentiment and the underlying fundamentals of GO’s portfolio. The REIT’s assets are concentrated in newer, luxury apartment buildings in Manhattan. These properties tend to attract higher-quality tenants, support above-average rental rates, and benefit from relatively lower maintenance and insurance costs compared to older housing stock.

Supply

Manhattan remains one of the most supply-constrained residential markets globally. High land costs, the expiration of key tax incentive programs, elevated construction costs, and an uncertain regulatory environment have significantly curtailed new development. Even projects that have entered the development pipeline are facing delays or abandonment. Approximately 30 percent of the city’s pre-development pipeline, representing roughly 47,000 units, has been stalled for more than five years and is widely considered inactive. With limited new supply expected to enter the market in the near term, upward pressure on rents is likely to persist. Notably, the majority of GO’s units are market-rate and not subject to rent control, providing greater flexibility in capturing this pricing power.

Demand

Demand for high-quality rental housing in Manhattan remains exceptionally strong. As of February 2026, median rents exceeded $5,000 for the first time, supported by vacancy rates below 2 percent in prime, full-service building segments. Several structural factors continue to reinforce this demand. Tenant retention remains elevated, with a significant majority of residents opting to renew leases rather than re-enter a competitive rental market. At the same time, higher mortgage rates have kept many high-income professionals in the rental market longer than anticipated, effectively creating a “renting by necessity” cohort. In parallel, the continued normalization of office attendance, now approaching pre-pandemic levels, has reinforced demand for centrally located, amenity-rich buildings. GO’s portfolio is well positioned within this segment, benefiting from both location and asset quality.

Primaris REIT: Scale Advantage in Canada’s Constrained Mall Market

Overview

Primaris REIT is the largest owner and operator of enclosed shopping centres in Canada. The REIT has been actively repositioning its portfolio, recycling capital out of lower-performing assets and concentrating investment in larger, more productive regional centres. This scale provides a meaningful competitive advantage. National and premium retailers such as Apple, Aritzia, and Lululemon increasingly prefer to partner with landlords who can offer consistent access across multiple markets. Primaris is well positioned to meet this demand. The REIT also benefits from an internally managed structure, allowing for greater control over leasing strategy, operations, and redevelopment initiatives.

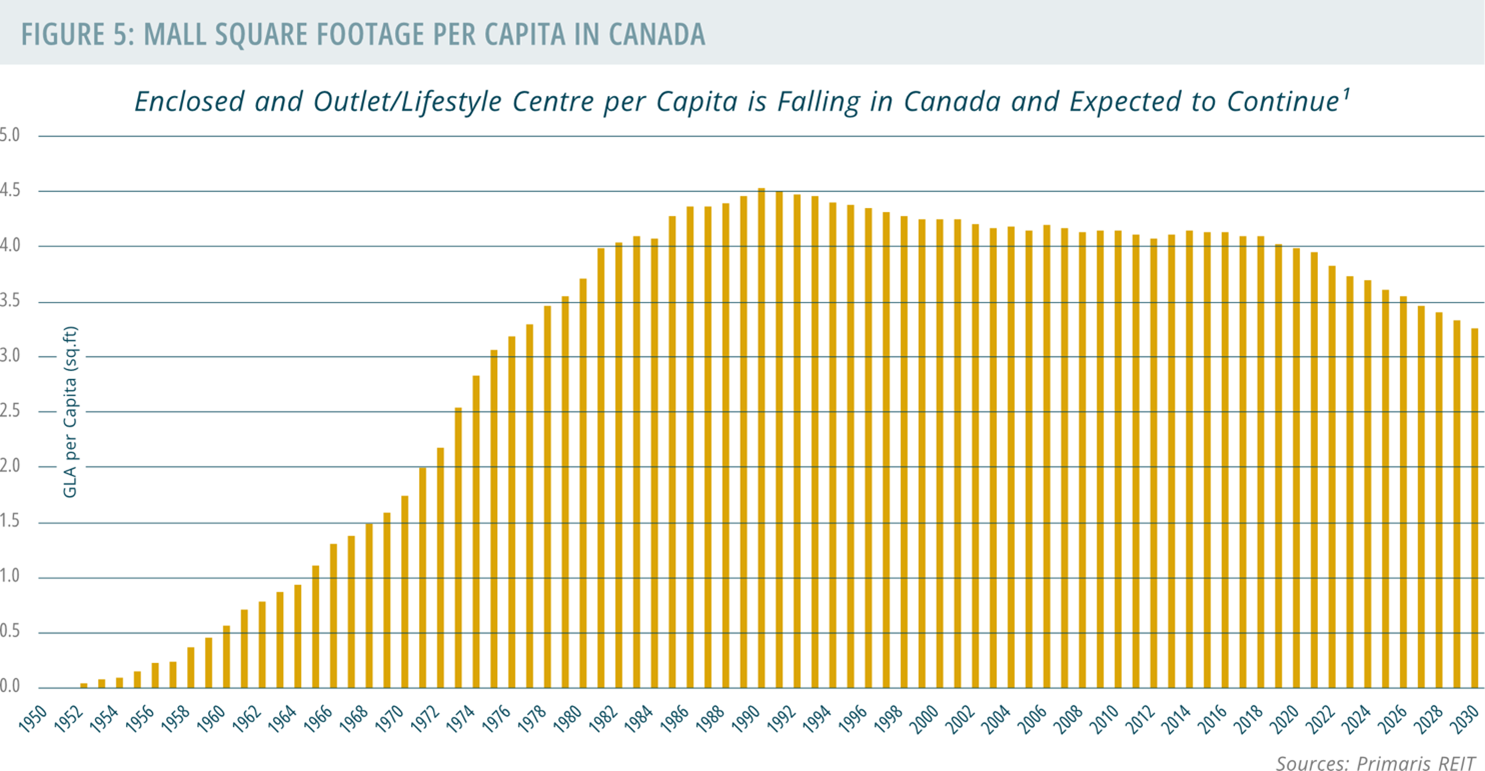

Supply

New enclosed mall development has been limited for decades, with the majority of Canada’s existing mall infrastructure built between the 1960s and 1980s. Over the past 15 years, the rise of e-commerce has accelerated the rationalization of lower-quality retail assets, leading to closures and redevelopment across North America. Recent high-profile department store bankruptcies have further reduced anchor tenancy across weaker centres. At the same time, new retail development has largely shifted toward outlet formats located outside major urban cores. The ownership landscape for enclosed malls remains fragmented, creating an opportunity for scaled operators such as Primaris to consolidate high-quality assets and drive operational efficiencies across their portfolios. We expect this consolidation trend to continue.

Demand

Retail demand within well-located regional malls remains resilient. Increasing population density in major Canadian urban centres continues to support higher foot traffic and rising sales per square foot for retailers. In an environment where new supply is limited, retailers are focused on expanding within proven, high-performing locations. This dynamic has supported Primaris’ leasing activity, with recent renewals achieving rental rate increases of approximately 11 percent. The combination of strong tenant demand and constrained supply continues to support rent growth and asset productivity across the portfolio.

REIT Portfolio Outlook: Income Stability and Long-Term Growth

Across our REIT portfolio, we see consistent evidence of favourable supply-and-demand dynamics supporting underlying asset performance. These conditions are expected to drive continued growth in rents, occupancy, and overall cash flow across our holdings.

Importantly, balance sheets and debt structures have largely adjusted to reflect the higher interest rate environment. As a result, we believe current distributions are well supported by underlying cash flows, with the potential for excess capital to be allocated toward reinvestment or incremental returns to unitholders over time.

All of our REIT positions benefit from internal management structures, providing greater control over operations, leasing, and capital allocation. This alignment, combined with disciplined cost management, reinforces our confidence in the long-term durability and growth profile of the portfolio.

The REIT sector is currently trading at a discount to net asset value (NAV), with our holdings positioned at an even wider discount. In practical terms, this suggests that the market is assigning a lower value to these businesses than the estimated worth of their underlying real estate, net of debt.

Over time, we would expect well-managed REITs to grow NAV on a per-unit basis through disciplined capital allocation and operational performance. As this occurs, market pricing has historically moved closer to underlying asset value.

Until that gap narrows, we believe the current disconnect presents an attractive entry point. We are comfortable maintaining exposure to these positions at valuations that, in our view, do not fully reflect the quality of the assets or the durability of their cash flows.