Michael Hakes, CFA, MBA

Air Canada is being priced for a problem it has already solved. The prevailing view still reflects a pandemic-era reality. Excess leverage, heavy dilution and structural fragility continue to define the narrative. That framing is increasingly disconnected from the underlying business.

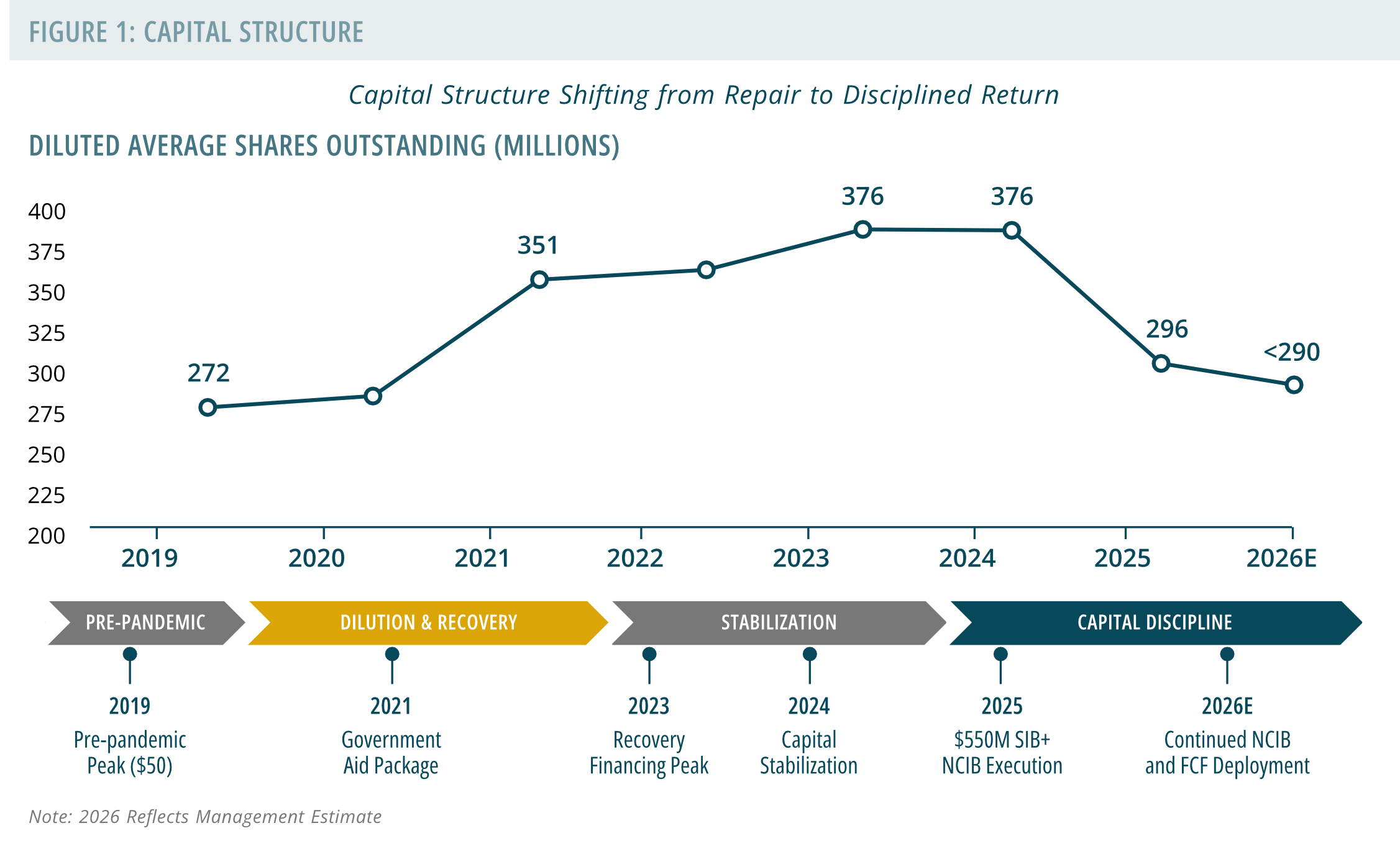

Over the past three years, Air Canada has undertaken a disciplined repair of its balance sheet, a process that came with meaningful trade-offs. The share count expanded by nearly 40 percent, weighing on per share performance even as operations steadily recovered. Market attention has largely remained on that dilution, rather than the progress it enabled.

The business is now entering a different phase. With the balance sheet stabilized, free cash flow is being redirected toward share reduction, while fleet modernization begins to reshape the underlying cost structure. The transition underway is less about recovery and more about refinement, with the operating foundation now in place.

Between 2019 and 2024, the share count increased from 272 million to approximately 376 million, a necessary step to preserve the business through an unprecedented period of disruption. As revenues returned to record levels, those earnings were distributed across a larger base, limiting the translation into equity performance.

That dynamic is now beginning to shift.

The inflection is not subtle. In 2025 alone, the company deployed over $850 million to shareholders, including a $500 million Substantial Issuer Bid, reducing the share count to approximately 296 million. Management continues to execute on the NCIB, with estimates pointing to fewer than 290 million shares in 2026.

This is the critical shift. The same earnings base is now being applied to a shrinking denominator. Even under conservative assumptions, this creates meaningful EPS expansion. The company no longer needs outsized growth to justify a higher share price. It needs consistency and continued capital return.

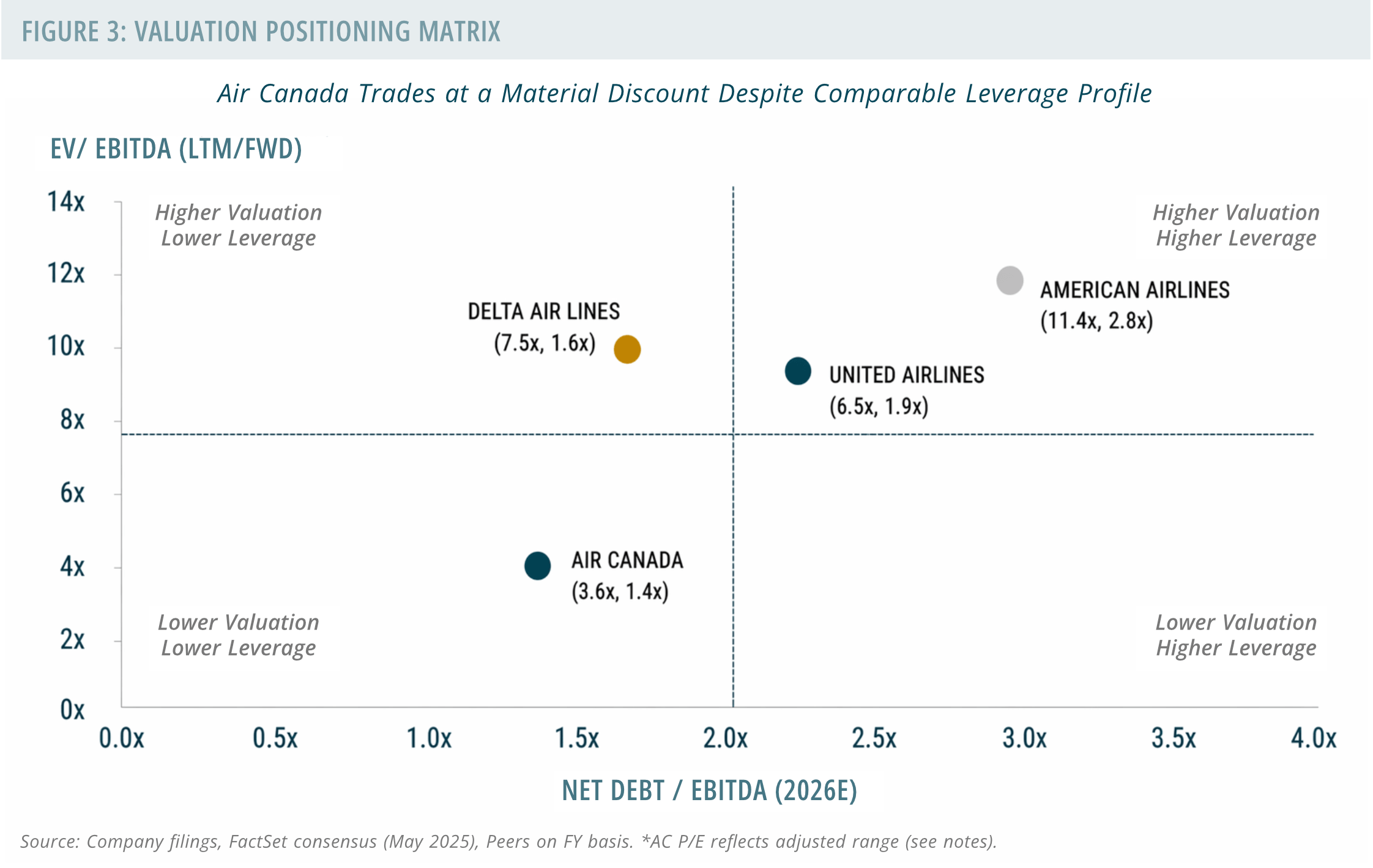

Leverage has also moved into a range that no longer supports a distressed narrative. Net debt to EBITDA has declined to approximately 1.3x to 1.6x, broadly aligned with United and within range of Delta. The balance sheet is no longer a limiting factor, though the equity has yet to fully reflect that shift.

Attention is now turning to the cost structure, where change is being driven by underlying economics rather than pricing. Air Canada is reshaping the profile of its long-haul network. Transatlantic and extended range routes have traditionally relied on wide-body aircraft such as the Boeing 787. These aircraft deliver strong unit economics when deployed at scale, but they carry higher trip costs and depend on consistently high load factors. That operating profile has historically constrained flexibility, particularly across secondary markets and in shoulder periods.

Airbus’ narrow-body platform is central to this shift. By extending its reach to 4,700 nautical miles, the A321XLR is a narrowbody (single aisle) that can service long-haul markets that were previously only accessible to larger, more expensive wide-body aircraft like the 787. While the A320neo keeps regional costs down, the A321XLR actively lowers the breakeven threshold for “thin” long-distance routes—allowing airlines to fly further with fewer passengers without sacrificing the maintenance benefits of a common narrow-body fleet.

The structure of the network is becoming more defined. Wide-body aircraft such as the 787 continue to support high-density, long-haul demand, while the A321XLR extends reach into thinner transatlantic markets where traditional economics have been more difficult to sustain. Alongside this, the A320neo reinforces efficiency across short- and mid-haul flying, supporting frequency and improving cost discipline across the broader network.

This combination expands the range of routes that can be operated profitably. Markets such as Montreal to secondary European cities become viable without relying on peak seasonal demand, allowing capacity to be aligned more closely with underlying demand patterns. The result is a network that is both broader and more flexible, with improved economics at the route level.

Deliveries of the A321XLR are expected to begin in 2026, with margin benefits becoming more evident through 2027 and 2028. While this represents a forward catalyst, the direction of travel is already visible in the evolving cost structure and network design. The current valuation continues to reflect a level of stress that is increasingly disconnected from the operating reality.

Air Canada currently trades at approximately 3.6x EV/EBITDA on a forward basis. Within the airline sector, that level of valuation is typically reserved for carriers facing liquidity concerns or structural decline. Neither applies here.

Delta trades at approximately 7.5x EBITDA with a comparable leverage profile, while United is closer to 6.5x with modestly higher leverage. American, despite carrying significantly more debt, continues to trade at levels that reflect durability rather than distress. The valuation gap relative to Air Canada remains wide.

Some of that discount can be attributed to structural factors, including a smaller domestic market and historically higher cost structures in Canada. However, the current spread suggests the market is still assigning risk that has largely been absorbed. A re-rating does not require a change in fundamentals so much as a shift in recognition. Even a move to 4.5x to 5.0x EBITDA, still below U.S. peers, would imply meaningful upside.

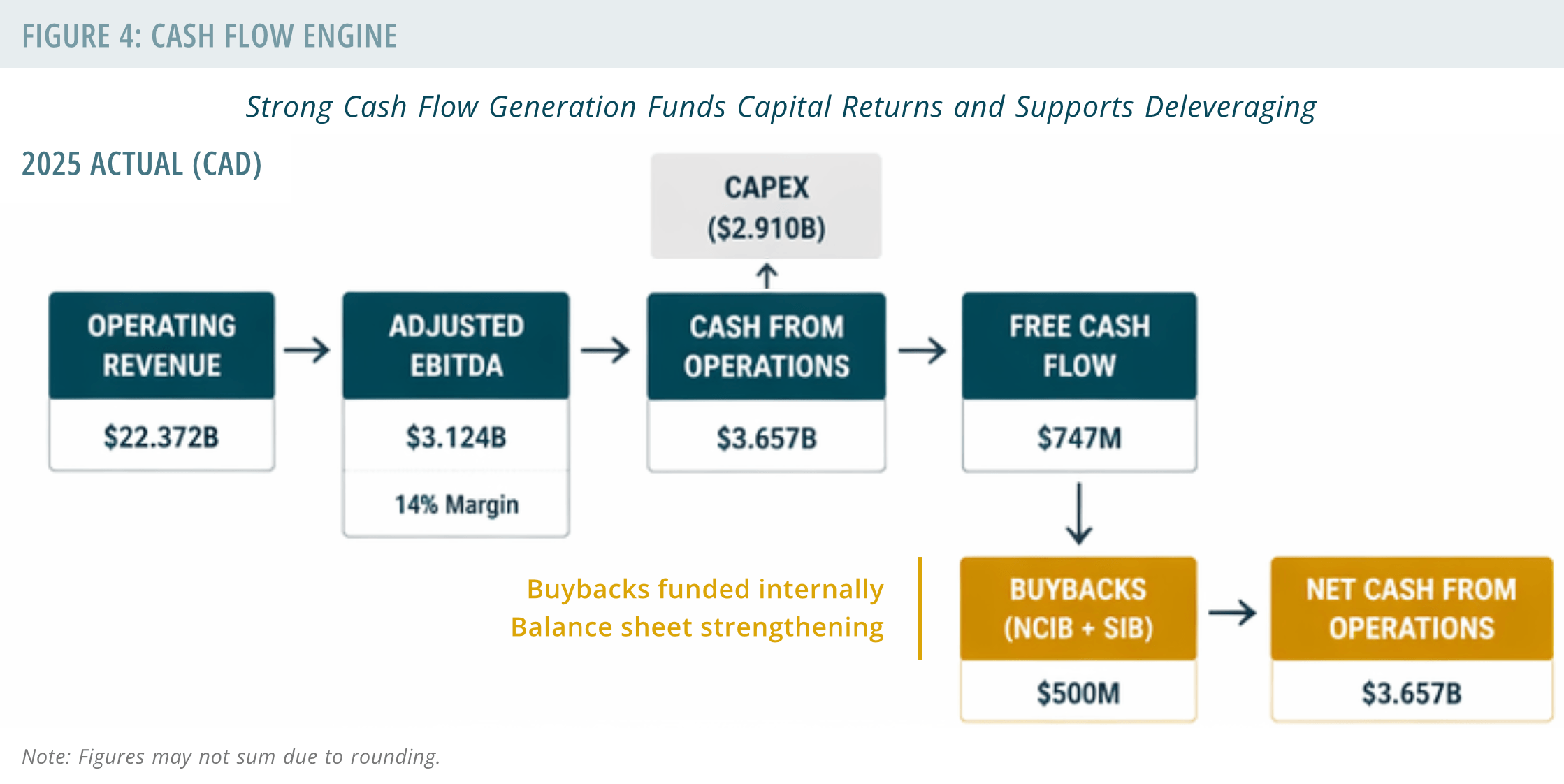

The most compelling evidence sits in the company’s ability to perform under pressure. 2025 was not a clean operating environment. Labour disruptions alone reduced operating income by approximately $375 million. At the same time, the company was in the peak phase of its capital expenditure cycle tied to fleet renewal. Despite this, Air Canada generated $22.4 billion in revenue, $3.1 billion in adjusted EBITDA and $747 million in free cash flow.

The business is now demonstrating an ability to fund capital returns internally, even alongside elevated investment. Net cash from operations reached approximately $3.7 billion, supporting both fleet modernization and shareholder returns without adding pressure to the balance sheet. Air Canada entered 2026 with operating momentum and a more stable financial foundation.

There are, however, risks that warrant attention. Fuel costs remain sensitive to geopolitical developments, particularly in the Middle East. The CAD/USD exchange rate continues to influence operating costs and debt servicing, while recent labour agreements have reset portions of the cost base higher and will take time to be fully offset through efficiency gains.

These factors may introduce near-term volatility, particularly through the first half of 2026, but they do not alter the underlying trajectory. The balance sheet has been repaired and leverage now aligns more closely with global peers. The share count is beginning to decline through internally funded buybacks, and fleet modernization is steadily improving the cost structure while increasing network flexibility.

These developments are already visible in the business. What remains is a valuation that continues to reflect uncertainty rather than progress. The stock is still being assessed through a lens of risk that has, in many cases, already been addressed.

The next phase is less dependent on external conditions and more on continued execution and market recognition. As earnings translate more consistently into per share value and the balance sheet narrative recedes, the foundation for a re-rating is in place. The opportunity now lies in recognizing the shift that has already occurred.