Jamie Murray, CFA, President

This week’s developments centre on three areas shaping current portfolio positioning: first quarter earnings from Big Tech and the continued buildout of AI infrastructure, followed by two company-specific events tied to recent additions across our strategies.

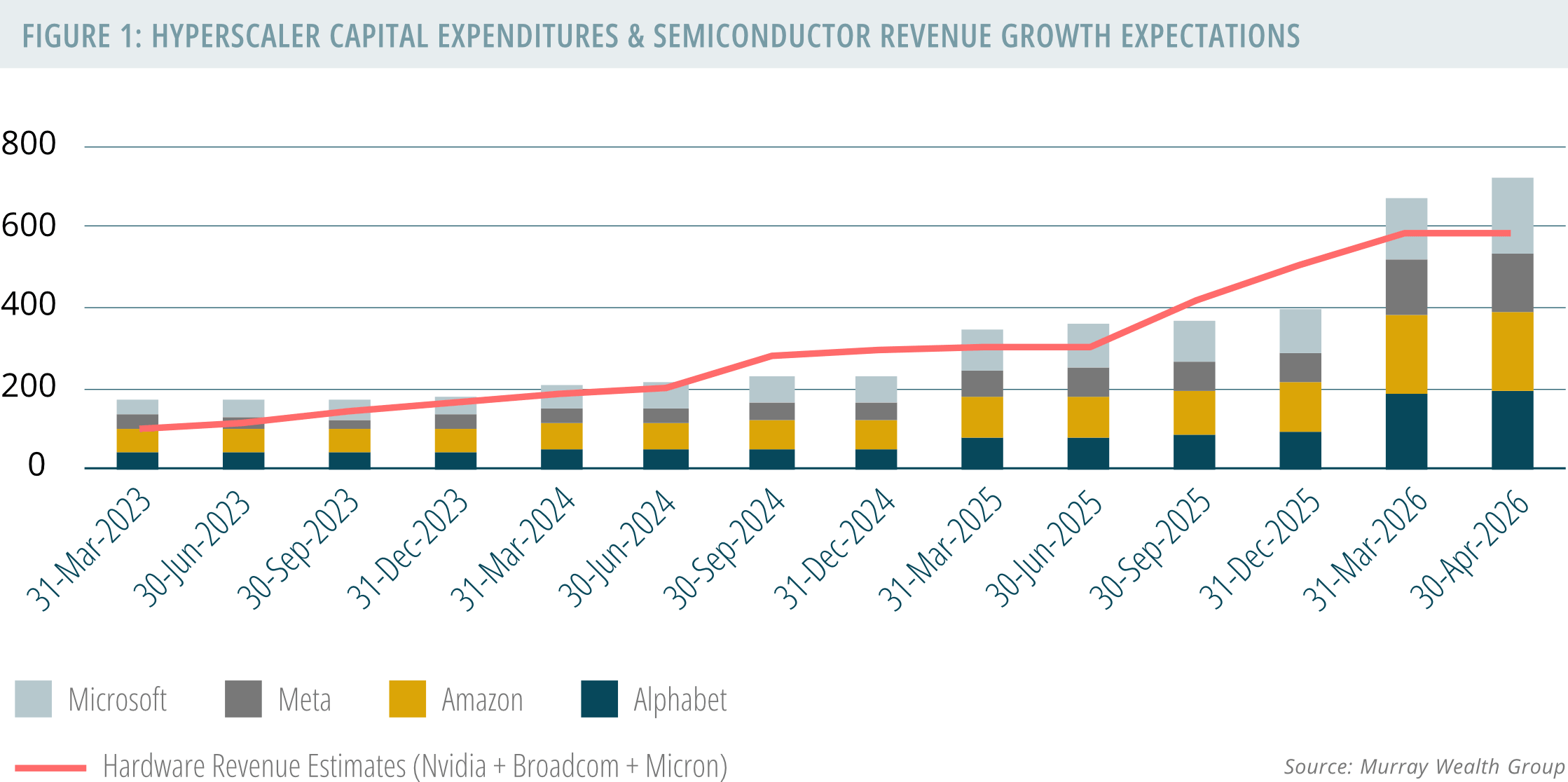

Big Tech Earnings and the Economics of AI Infrastructure

Amazon, Alphabet, Meta and Microsoft all reported first quarter earnings on the same evening, a rare alignment that offers a clear read on the pace and scale of investment behind generative AI. The message was consistent. Capital spending continues to move higher.

Across the group, projected capital expenditures now approach $725 billion in 2026, up materially from roughly $200 billion just three years ago. Alphabet, Microsoft and Meta each increased their forward investment plans, while Amazon remains the largest contributor with a program approaching $200 billion on its own.

This level of spending is not occurring in isolation. It is directly supporting revenue growth across the semiconductor and hardware ecosystem, particularly companies such as Nvidia, Broadcom and Micron. As expectations for annual capital expenditures increase, so do the expectations of annual sales by semiconductor/hardware companies.

The return side of the equation is beginning to show up in operating results. Cloud divisions continue to deliver strong growth at scale, with Amazon growing 28 percent, Alphabet 63 percent and Microsoft 39 percent on revenue bases that now sit near or above $100 billion. Meta, while not a traditional cloud provider, is leveraging its infrastructure to drive 33 percent revenue growth through AI-enabled advertising.

We are now seeing a shift from early generative AI applications toward more complex, agent-driven systems. These workloads require significantly more compute, and capacity remains constrained. In our view, this supports continued strength in pricing, utilization and margins across the value chain. The investment cycle is moving beyond its early phase, with returns now beginning to flow through in revenue growth and operating performance. The spending is real, the demand is measurable and the revenue response is already emerging.

Flowserve: Infrastructure Behind the Nuclear Buildout

We recently added Flowserve to the Global Equity Growth Fund to gain exposure to a developing theme within industrials: the need for reliable, dispatchable power.

Nuclear energy remains part of that discussion. More than 30 countries have committed to tripling nuclear capacity by 2050, alongside increasing interest in small modular reactor technology.

Flowserve operates at the infrastructure level of this buildout. The company currently supports more than 300 nuclear reactors globally and recorded approximately $400 million in nuclear-related awards in 2025. Its February 2026 acquisition of Trillium Flow Technologies’ valves division expands its footprint further, adding exposure to 115 operating reactors and an installed base exceeding 200,000 units.

This is a classic “picks and shovels” position. Flowserve is not dependent on any single project outcome. Instead, it participates across both the maintenance of existing fleets and the development of new capacity. That combination provides durable exposure to a multi-decade investment cycle in energy infrastructure.

Kimberly-Clark and the Repricing of Kenvue

We initiated a position in Kenvue in October within the Income Growth Fund based on a view that market concerns surrounding Tylenol were overstated. Subsequent developments have supported that thesis.

Kimberly-Clark has announced a friendly acquisition of Kenvue at a 46 percent premium, effectively crystallizing value that had not been fully reflected in the share price. The transaction brings together a portfolio of established consumer brands, including Tylenol and Listerine, with Kimberly-Clark’s global scale and distribution capabilities.

The outcome is straightforward. The premium provides immediate value realization, while the combined entity offers a more diversified and lower volatility earnings profile. The strategic rationale is also clear. Kimberly-Clark expects approximately $2.1 billion in synergies, driven by distribution efficiencies and the integration of Kenvue’s specialized health capabilities. The transaction also reduces company-specific risk by absorbing Kenvue into a significantly larger balance sheet, with combined revenues of approximately $32 billion.

Shareholders will receive $3.50 in cash and 0.14625 shares of Kimberly-Clark for each Kenvue share held. We expect to transition our position accordingly upon closing.