Bruce Murray, CFA, CEO & CIO

Why earnings growth, AI-driven productivity and corporate profitability continue to outweigh short-term market volatility

For the past several years, inflation has dominated financial headlines and investor sentiment. After remaining relatively stable between 2016 and 2019 at approximately 2%, inflation dropped sharply during the pandemic before surging to levels not seen in decades following extraordinary fiscal and monetary stimulus. Inflation reached 7.0% in 2021 and remained elevated at 6.5% in 2022 before beginning a more meaningful moderation trend through 2023, 2024 and into 2025.

In response, central banks raised interest rates aggressively. The U.S. 10-year Treasury yield moved from near historic lows around 1% in 2020 to above 4% by 2023, briefly approaching 5% before stabilizing in the 4% to 4.5% range.

Higher rates, persistent geopolitical instability, tariffs and ongoing conflict in several regions have understandably created periods of market volatility and investor unease. Markets have experienced pullbacks, sideways trading periods and rapid shifts in sentiment as investors attempt to assess the economic implications of each new development.

While inflation, interest rates and geopolitical events continue to influence short-term market sentiment, long-term equity performance remains primarily driven by corporate earnings growth. Current earnings trends suggest that backdrop continues to strengthen.

Markets Can Advance Without Higher Valuations

Over time, equity market returns are largely driven by two underlying forces: the growth rate of corporate earnings and the valuation investors are willing to assign to those earnings through price-to-earnings multiples.

During highly optimistic market environments, expanding valuations can amplify returns as investors become willing to pay increasingly higher multiples for future earnings expectations.

However, valuation expansion is not required for markets to move higher. When earnings growth remains durable and consistent, equity markets can continue advancing even if valuation multiples remain stable. In many respects, markets driven by earnings rather than speculative multiple expansion tend to produce healthier and more sustainable long-term outcomes.

Current market conditions increasingly reflect this type of earnings-led environment, where improving profitability is supporting equity returns even without significant valuation expansion.

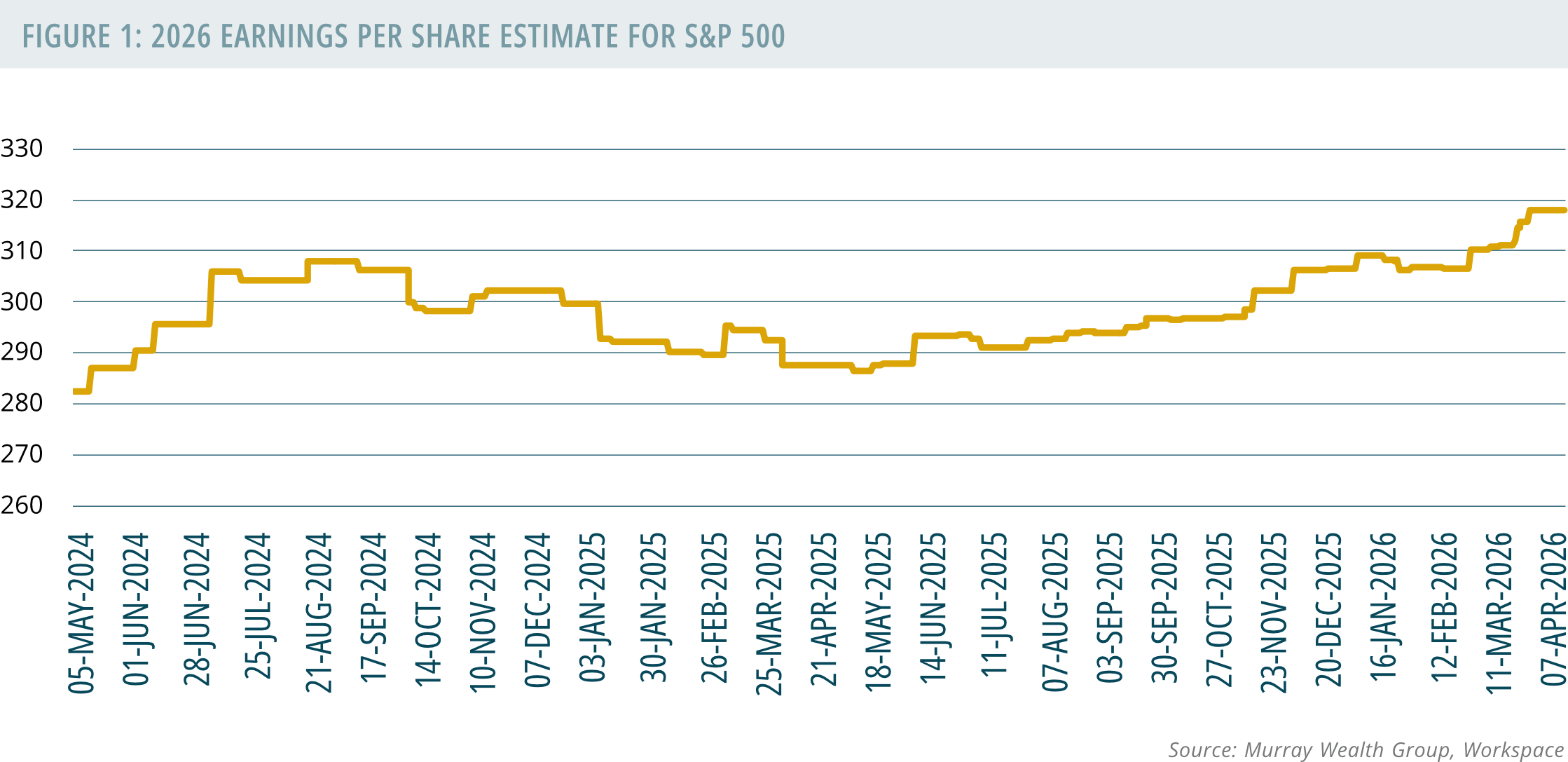

Figure 1 demonstrates the continued rise in 2026 earnings per share estimates for the S&P 500. Despite market volatility surrounding tariffs, oil prices and geopolitical events, analyst expectations for corporate profitability have continued moving higher and have recently accelerated further.

AI Is Becoming an Economic Productivity Engine

One of the most important contributors to accelerating earnings growth is the rapid adoption of artificial intelligence across the global economy.

Much of the public conversation surrounding AI remains focused on consumer-facing applications such as Amazon Q, Google Gemini and ChatGPT. While these tools are highly visible, the more significant economic impact is occurring inside large organizations where AI is increasingly embedded into core business operations.

Companies across industries are now using AI to:

- Automate labour-intensive operational processes

- Improve forecasting, logistics and inventory management

- Enhance pricing models and customer service efficiency

- Accelerate decision-making and data analysis

- Increase output without proportionally increasing labour costs or capital expenditures

These productivity gains are beginning to appear directly in corporate earnings results.

Historically, periods of major productivity expansion have created significant long-term economic value. AI increasingly appears positioned to become one of those transformational periods as companies capable of integrating AI effectively into their operations improve margins, increase efficiency and strengthen earnings power even within a higher interest rate environment.

For investors, the distinction between speculative enthusiasm and measurable earnings improvement is important because markets supported by real productivity gains tend to be significantly more durable over time.

Valuation Stability Is Supporting Market Durability

A frequent concern among investors today is whether markets have become overly expensive following the strong rally of the past two years. But context matters.

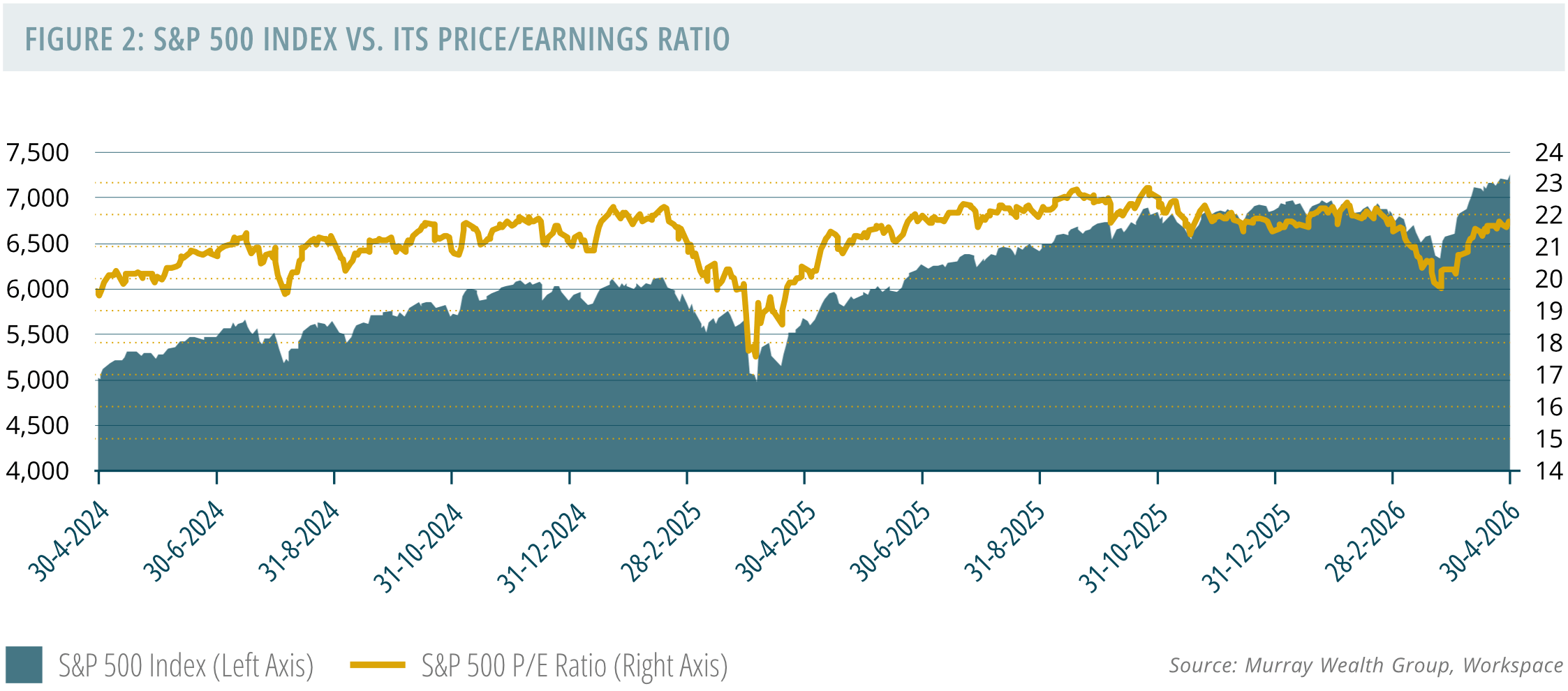

Since late 2023, the S&P 500 has risen substantially, moving from approximately 5,000 to above 7,000. However, the majority of that increase has been driven by improving earnings power rather than dramatic valuation expansion.

Our analysis suggests that approximately 80% of the market’s advance during this period can be attributed to higher corporate earnings, while only a relatively modest increase in valuation multiples contributed to the remainder. Figure 2 highlights the relationship between the S&P 500 Index and its price-to-earnings ratio over the recent market cycle.

Markets supported by earnings growth historically demonstrate greater resilience during periods of macroeconomic uncertainty because profitability provides a stronger long-term foundation than speculative valuation expansion alone.

Today’s market environment appears fundamentally different because the current advance is being supported by improving corporate profitability rather than purely speculative valuation expansion. The market continues to benefit from stronger productivity trends, durable earnings momentum and improving operational efficiency across several sectors of the economy.

Portfolio Positioning Continues to Focus on Earnings Power

Our investment discipline remains centered on identifying companies capable of generating sustainable long-term earnings growth.

We continue to favour businesses with:

• Strong and accelerating earnings growth

• Balance sheets capable of funding innovation internally

• Durable competitive advantages

• Clear exposure to AI-driven productivity expansion

• Management teams capable of adapting to rapidly evolving economic conditions

We maintain meaningful exposure to several of the world’s largest hyperscale technology companies including Amazon, Alphabet, Meta and Microsoft. These businesses possess the financial resources, infrastructure and technological capabilities necessary to convert large-scale AI investment into long-term earnings growth as adoption broadens across the economy.

Beyond technology, we also continue to see growing opportunity across industrials, infrastructure, materials and energy businesses that stand to benefit from the downstream economic effects of AI-related capital investment and productivity improvements.

We are also beginning to see improving earnings momentum across parts of the industrial sector as supply chain disruptions and product shortages created during the pandemic continue to normalize. Many businesses spent the past several years working through operational bottlenecks, delayed capital projects and inventory constraints that persisted well beyond the initial COVID recovery period. As those pressures ease, industrial companies are increasingly benefiting from both improving operating conditions and rising demand tied to large-scale AI infrastructure development, including data centres, power systems, electrical equipment and broader industrial buildouts.

Importantly, the current market environment does not require further valuation expansion to support future returns. If earnings growth continues moving higher, markets can continue advancing even within a relatively stable valuation framework.

Over long investment horizons, equity returns continue to be grounded in fundamentals such as earnings growth, productivity improvement and capital allocation discipline rather than short-term market narratives. Our focus remains unchanged: identify businesses capable of converting productivity gains into durable profitability while avoiding companies unable to adapt to structural economic change.