Should I Stay or Should I Go Now?

“Sell in May and go away” is one of the market’s most enduring pieces of conventional wisdom. The idea suggests investors should reduce equity exposure during the summer months because market returns have historically been stronger from November through April. Academic research around the sell in May phenomenon has debated whether this seasonal pattern is a meaningful signal or simply a statistical anomaly.

From 1950 through the financial crisis, the data largely aligned with the theory. During that period, markets generated roughly 7% returns from November through April versus approximately 2% during the May–October period. There were also several structural explanations that potentially supported the pattern, including lighter summer trading volumes, seasonal cash flow shifts and year-end allocation cycles.

Market structure, however, has evolved materially over the past fifteen years. Automatic payroll contributions, the rise of ETFs and increasingly efficient electronic trading have reduced many of the conditions that may once have contributed to seasonal market behaviour.

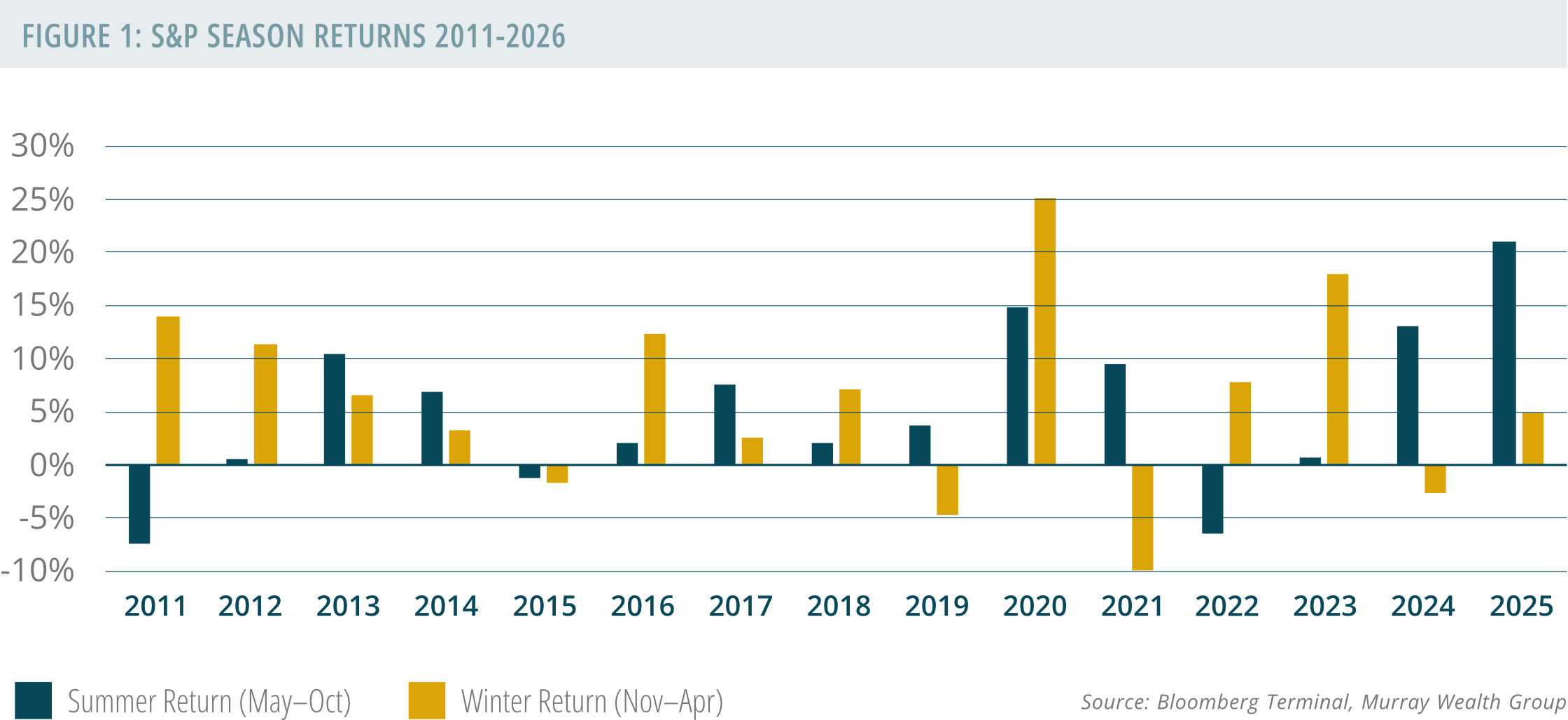

As Figure 1 illustrates, the S&P 500 delivered positive returns during the May–October period in 12 of the last 15 years, averaging roughly 5% annually. Summer performance exceeded winter performance in eight of those fifteen years, suggesting sitting on the sidelines has increasingly become a missed opportunity rather than a defensive strategy.

The last two years serve as a useful reminder that markets can advance when sentiment least expects it. The S&P 500 returned approximately 14% from May through October 2024 and roughly 22% during the same period in 2025.

For long-term investors, the takeaway remains consistent: stay invested, remain diversified and avoid allowing a memorable calendar slogan to interfere with a disciplined investment plan.

Market Update

Equity markets rebounded sharply in April, recovering much of the ground lost during the previous month’s sell-off. The S&P 500 gained approximately 10.4%, supported by renewed strength in large-cap technology and semiconductor stocks as the AI growth theme reasserted market leadership.

Canadian equities also advanced, with the S&P/TSX Composite Index finishing the month up roughly 3.1%. While gains in Canada were more measured than in the U.S., performance was supported by strength in base metals and steady contributions from the financial sector.

Commodity markets reversed some of March’s trends. Crude oil prices moved lower toward month-end as geopolitical risk premiums eased, while gold and silver posted modest gains as the U.S. dollar softened and Treasury yields declined slightly. Overall, April reflected a market environment beginning to stabilize following the volatility of the prior month.

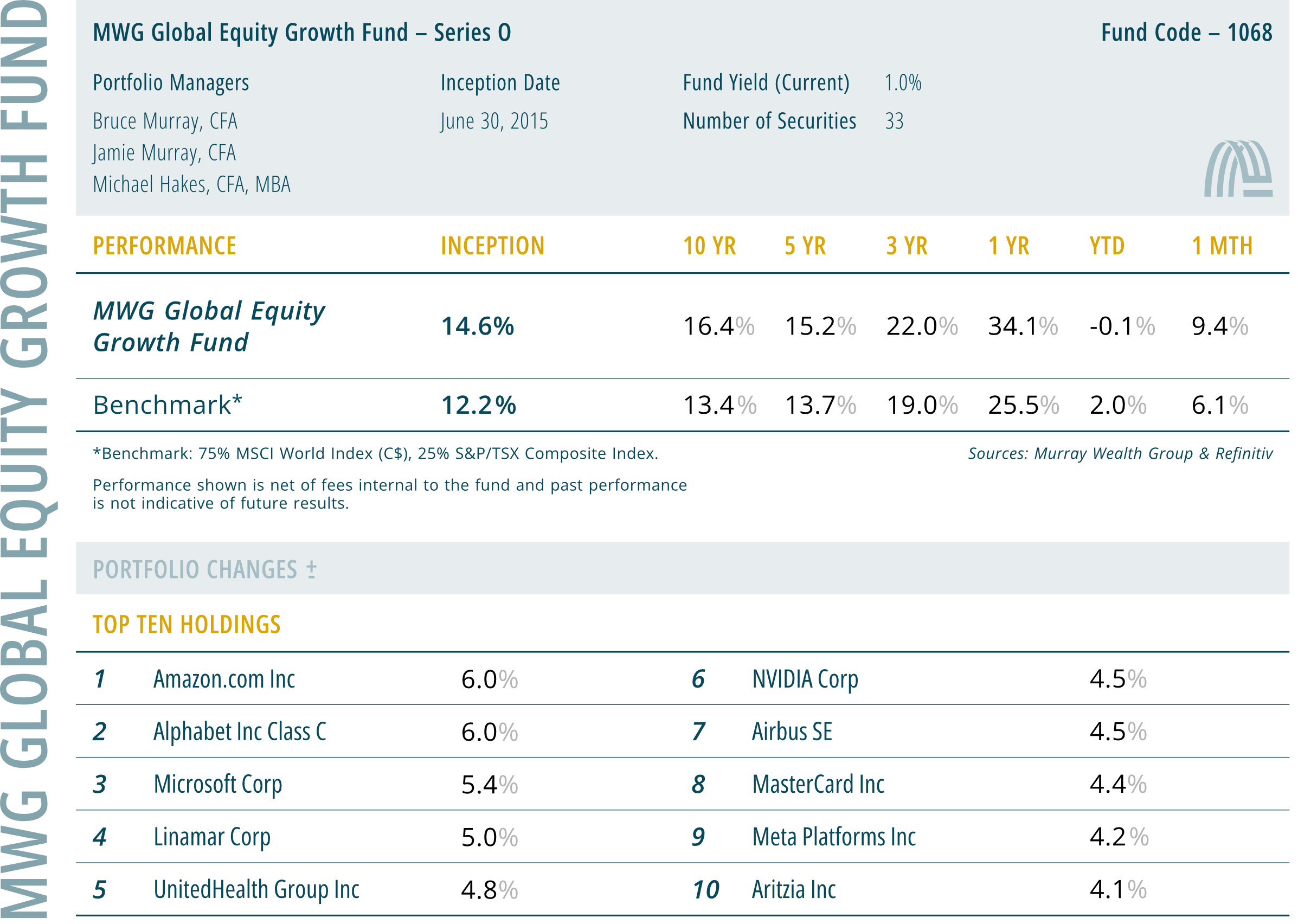

MWG Global Equity Growth Fund

The MWG Global Equity Growth Fund Series O delivered a strong April return of 9.4%, outperforming its benchmark return of 6.1%. Year-to-date, the Fund was down 0.1%, compared with a 2.0% gain for the benchmark. Performance was supported by strength in Hammond Power Solutions, UnitedHealth Group and Broadcom. The main detractors were ServiceNow, Alamos Gold and Lululemon.

Portfolio Manager Summary

After a six-month pause, the AI trade regained momentum in April. Several holdings most directly tied to the theme, including Nvidia, Broadcom, Amazon, Alphabet and Hammond Power Solutions, moved to new highs. Microsoft and Meta remain more than 20% below their 52-week highs despite strong financial results and we have added to these positions where we continue to see valuation opportunity.

Software stocks, by contrast, continue to trade poorly as investors weigh the potential impact of AI disruption. We believe the market is beginning to distinguish between businesses positioned to benefit from AI adoption and those more vulnerable to business model pressure.

Consumer markets remain highly bifurcated. Momentum brands such as Aritzia continue to show strong growth, while established brands such as Lululemon and LVMH face slower demand and competitive pressure. In select cases, we believe market pessimism may be creating attractive long-term opportunities.

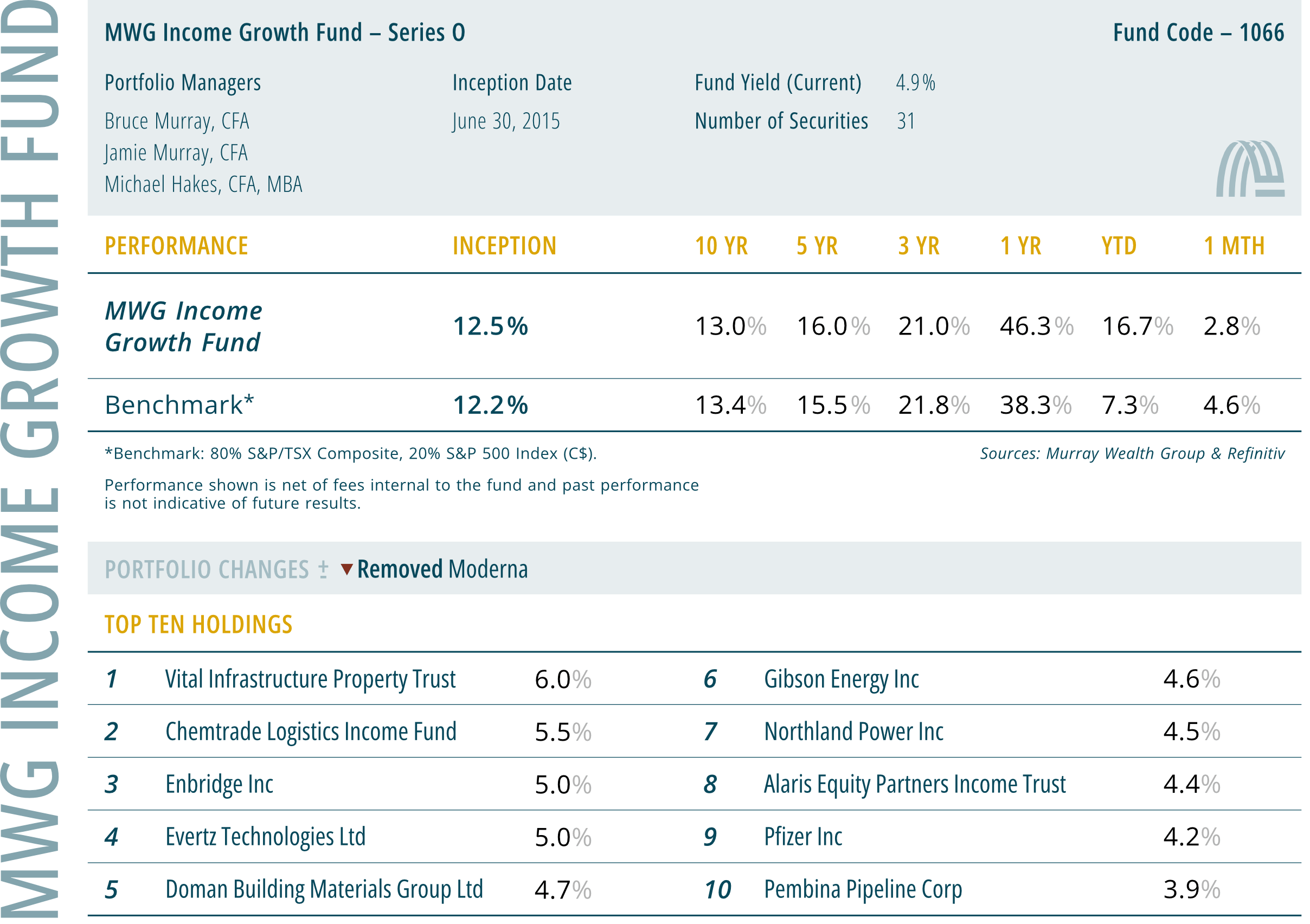

MWG Income Growth Fund

The MWG Income Growth Fund Series O rose 2.8% in April compared with a 4.6% benchmark return. Year-to-date, the Fund has returned 16.7%, ahead of the benchmark return of 7.3%.

April performance was led by Opera, Propel Holdings and Toronto-Dominion Bank. Detractors included Pfizer, PHX Energy and Telus.

Portfolio Manager Summary

The Fund continued to deliver strong year-to-date performance despite weakness in energy-related holdings as oil prices moved lower from March highs.

Canadian bank stocks were among the strongest performers in April, with the equal-weight Canadian Banks ETF up approximately 12% for the month. As we noted last fall, Canadian banks appear closer to fair value, although continued demand for shares remains constructive.

We continue to see opportunity in Canadian alternative lenders such as Alaris and Propel Holdings. These businesses serve areas of the market outside traditional banking channels and recent results continue to support our investment thesis. Following a strong rally over the past year and several prior trims to the position, we exited Moderna entirely during the month.