By: Bruce Murray, CFA

Investment Spotlight: Alamos Gold and the Case for Growing Production and cash flow

Gold prices have climbed sharply over the past two years, and while daily headlines often focus on tariffs, trade disputes and political tensions, the forces supporting gold today run deeper.

Across much of the Western world, governments are running larger deficits while defense spending rises meaningfully. NATO countries are expanding military budgets, while fiscal policy in the United States, Canada and Europe continues to support elevated government borrowing. At the same time, significant investment is being directed toward building AI infrastructure, another capital-intensive effort requiring large-scale funding.

Long term, AI-driven productivity gains should prove deflationary. In the near term, however, this combination of government spending, infrastructure investment and supply chain disruption creates inflationary pressure that is likely to persist over the next several years.

Add to this the impact of sanctions on Russian energy supplies and continued geopolitical uncertainty, and the case for sustained strength in gold prices becomes clearer. In that environment, gold producers capable of increasing production while managing costs effectively stand to benefit. One such company worth examining is Alamos Gold.

A Canadian-Centered Gold Producer

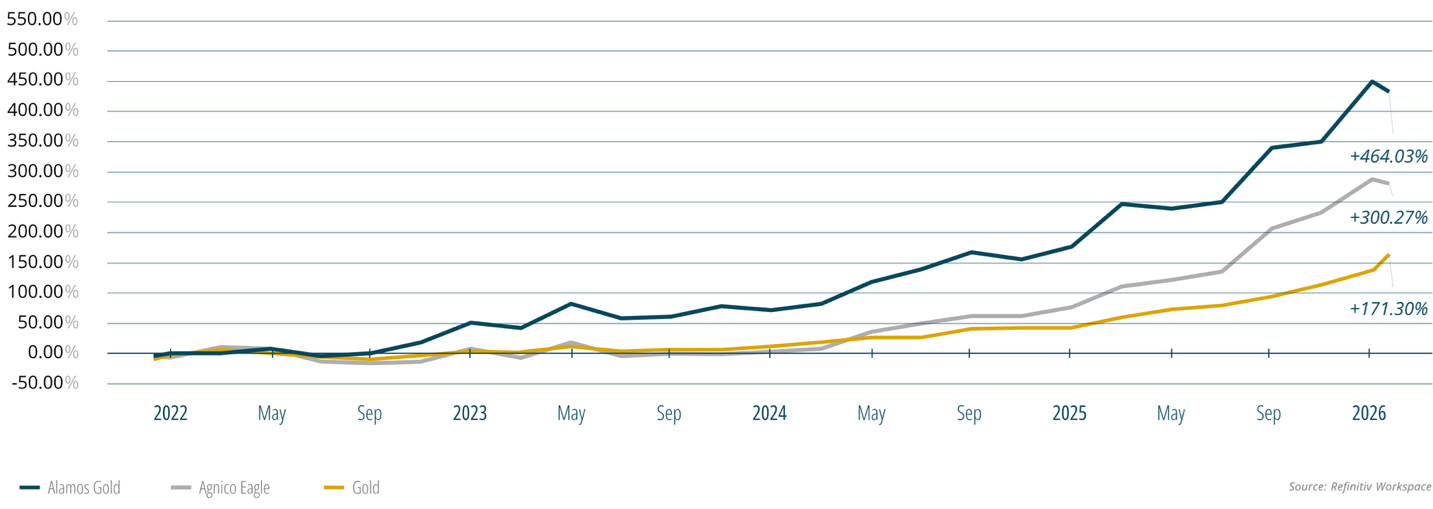

Alamos Gold has built a portfolio primarily centered in Canada, with one legacy operation in Mexico. For context, investors often compare the company with Agnico Eagle, widely viewed as the sector’s blue-chip benchmark.

Both companies have performed well as gold prices accelerated beginning in 2023, though Alamos still trades at a relative discount despite possessing several attractive assets and development opportunities.

Core Producing Assets

Island Gold District, Ontario

Located 83 km north of Wawa, the Island Gold Mine was originally discovered in 1985 and became part of Alamos through the acquisition of Richmont Mines in 2017. The transaction also added the nearby Magino property, first discovered in 1917.

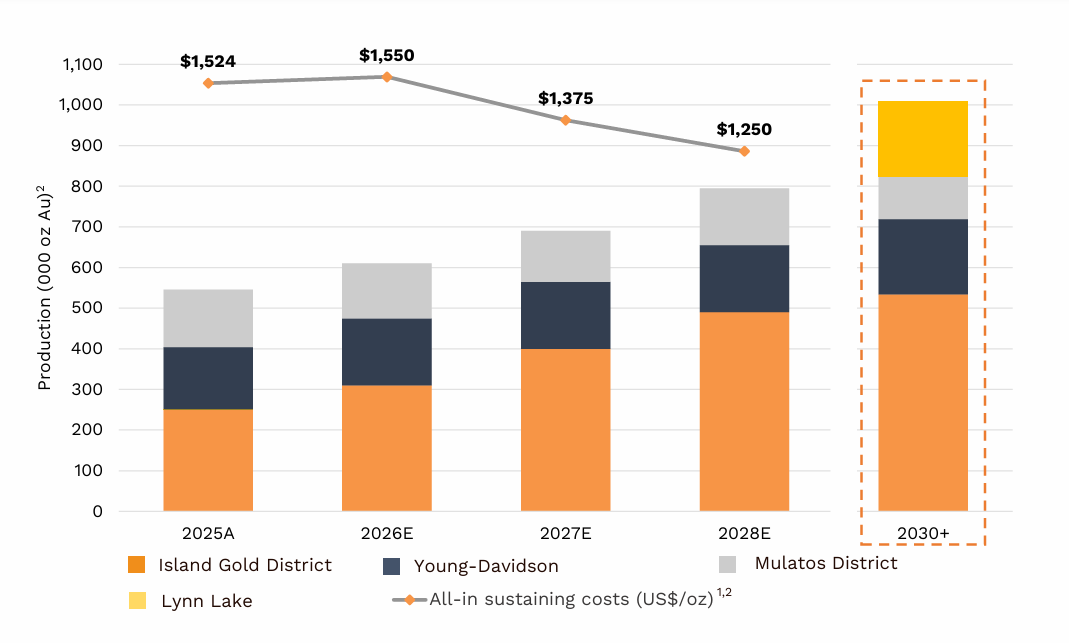

Mining activity in this district dates back to the 1930s, and today Island Gold has evolved into one of Canada’s largest and lowest-cost operations. The mine accounts for roughly half of Alamos’ production, with resources exceeding 10 million ounces. Production is expected to exceed 300,000 ounces in 2026, with continued exploration upside still present.

Young-Davidson Mine, Ontario

Discovered in 1917, the Young-Davidson mine produced approximately one million ounces between 1938 and 1957 before being restarted in 2010. Alamos acquired the asset through its merger with AuRico in 2015, marking the company’s first Canadian producing operation.

The mine currently contains more than four million ounces of resources and is expected to produce roughly 160,000 ounces in 2026.

Mulatos Mine, Mexico

Mulatos, located in north-central Mexico, is Alamos’ founding operation and an open pit mine that has produced more than three million ounces of gold since 2005. Over that period, the asset has generated approximately $900 million in free cash flow as multiple deposits have been developed and mined.

Development Pipeline Driving Future Growth

Alamos’ longer-term opportunity lies in its Canadian development projects, particularly the Lynn Lake project in Manitoba.

This region previously hosted significant gold, copper and nickel operations, including mines developed by Sherritt Gordon. Alamos has identified five deposits located close enough to existing infrastructure to support development, with total reserves exceeding four million ounces.

Projected all-in sustaining costs are expected to remain below $850 per ounce. If current gold prices persist, the project could generate approximately $16 billion in operational free cash flow over a ten-year production life.

Further exploration potential also exists in northern Quebec, where Alamos controls highly prospective properties extending across a 40 km strike. Development here remains several years away but adds optionality to the long-term portfolio.

Production Growth Outlook

Looking ahead, Alamos expects:

- Gold production to increase approximately 25 percent by 2028

- Cash operating costs to decline more than 10 percent

- Annual production to reach roughly 186,000 additional ounces between 2030 and 2040 following Lynn Lake start-up

In short, the company combines current production strength with visible growth ahead.

Source: Alamos Gold

Investment Perspective

Gold often performs best when economic uncertainty rises and inflation concerns persist. While market cycles shift, the structural drivers behind today’s gold market suggest prices may remain supported for several years.

In that setting, companies capable of expanding production efficiently and controlling costs deserve closer attention. Alamos Gold appears positioned to do exactly that, combining established operations with credible future growth.

For investors seeking exposure to gold through disciplined operators rather than simply relying on commodity price movements alone, Alamos offers a compelling case worth monitoring.