By: Michael Hakes, CFA, MBA

Rethinking Disruption in Payments

Is fintech disruption truly a threat to Mastercard or could it ultimately reinforce its position?

Recent headlines have created a narrative that the payments landscape is on the verge of being reshaped by artificial intelligence, digital currencies, and regulatory pressure. The concern is that new payment rails will bypass traditional networks and erode the economics of companies like Mastercard. While this argument appears logical at first glance, it overlooks what Mastercard actually does and why its role becomes more important as the system evolves.

Mastercard does not manufacture a product that can be easily replaced. It operates a global infrastructure that enables secure and trusted transactions across millions of merchants, financial institutions, and consumers. As commerce becomes more digital and increasingly automated, the need for that infrastructure grows rather than declines.

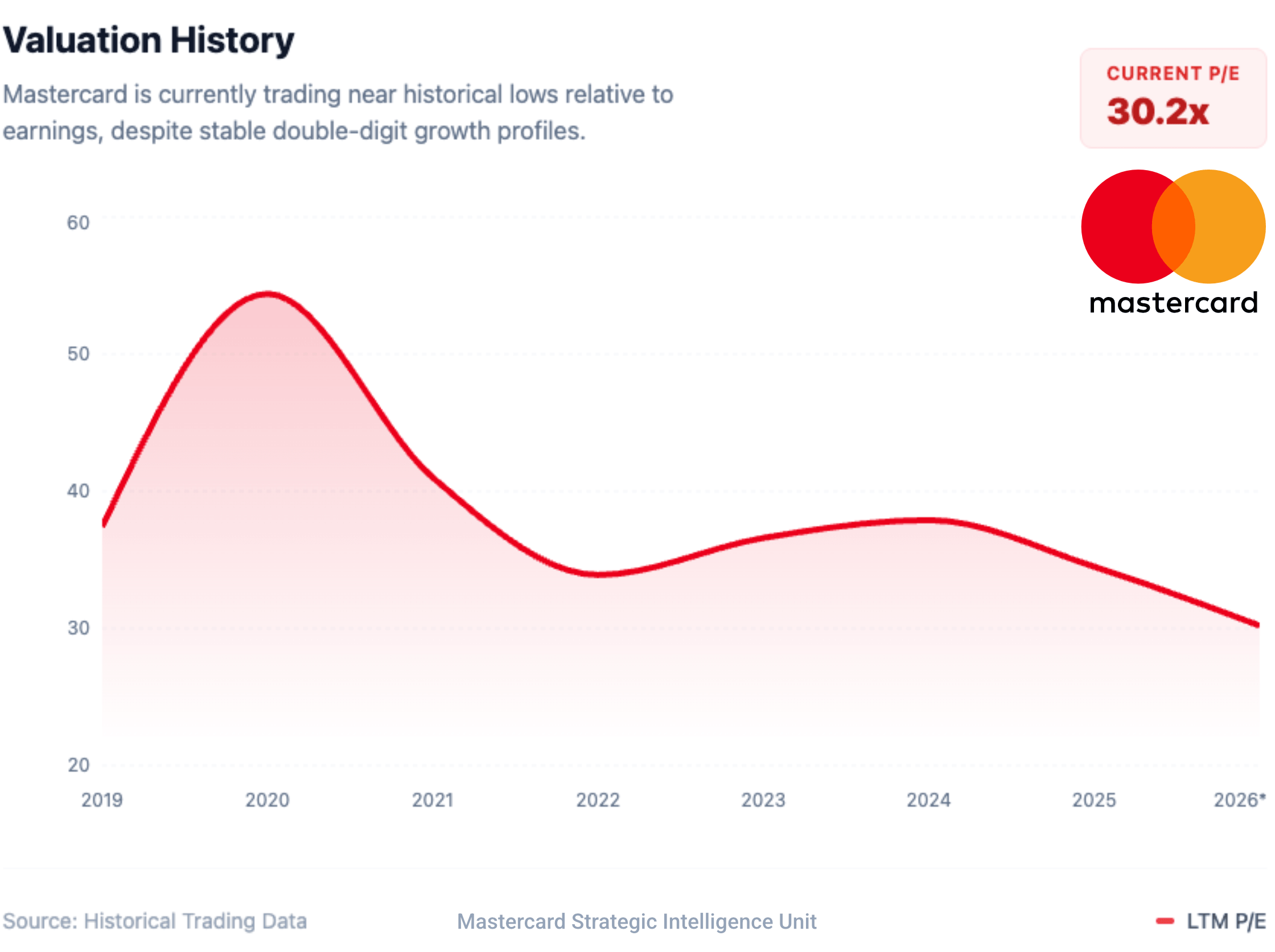

Figure 1: Valuation Range Chart

Mastercard is currently trading near the lower end of its historical valuation range despite consistent revenue growth and strong underlying fundamentals.

Complexity Is Increasing, Not Decreasing

The shift toward digital commerce has not simplified payments. It has made them more complex.

Artificial intelligence is beginning to influence how consumers discover and evaluate products, yet most transactions still require layers of validation before they can be completed. As payments move from physical interactions to digital interfaces and now toward software assisted decision making, the number of variables involved in each transaction expands. Identity must be verified with greater precision. Fraud risks must be identified and mitigated in real time. Consumer consent must be clearly established. Disputes must be resolved within a framework that protects all parties involved.

These functions form the foundation of trust in modern commerce. They are also the areas where Mastercard generates its economic value. As transactions evolve from individuals interacting directly with merchants to systems interacting on behalf of individuals, the importance of governance and security increases. Mastercard sits at the center of that layer, which positions the business to benefit from rising complexity rather than be displaced by it.

A Business Model That Extends Beyond the Transaction

One of the more important developments within Mastercard’s business over the past several years has been the expansion beyond traditional transaction fees. While global payment volumes remain a key driver of revenue, the company has steadily built a portfolio of services that deepen its role within each transaction.

Tokenization has become a central component of this strategy. Instead of transmitting sensitive card information, transactions are increasingly processed using secure digital credentials. Each card can now support multiple tokens across digital wallets, subscription services, and online platforms. This not only enhances security but also creates additional revenue opportunities tied to each transaction.

Alongside tokenization, Mastercard has invested heavily in authentication, fraud prevention, and data analytics. These capabilities are embedded directly into the payment flow, allowing the company to generate value at multiple points rather than relying solely on the initial authorization. The result is a business model that is more resilient and less dependent on any single revenue stream.

This evolution reflects a broader shift. Mastercard is no longer simply facilitating payments. It is providing the infrastructure that enables payments to occur safely and efficiently in an increasingly complex environment.

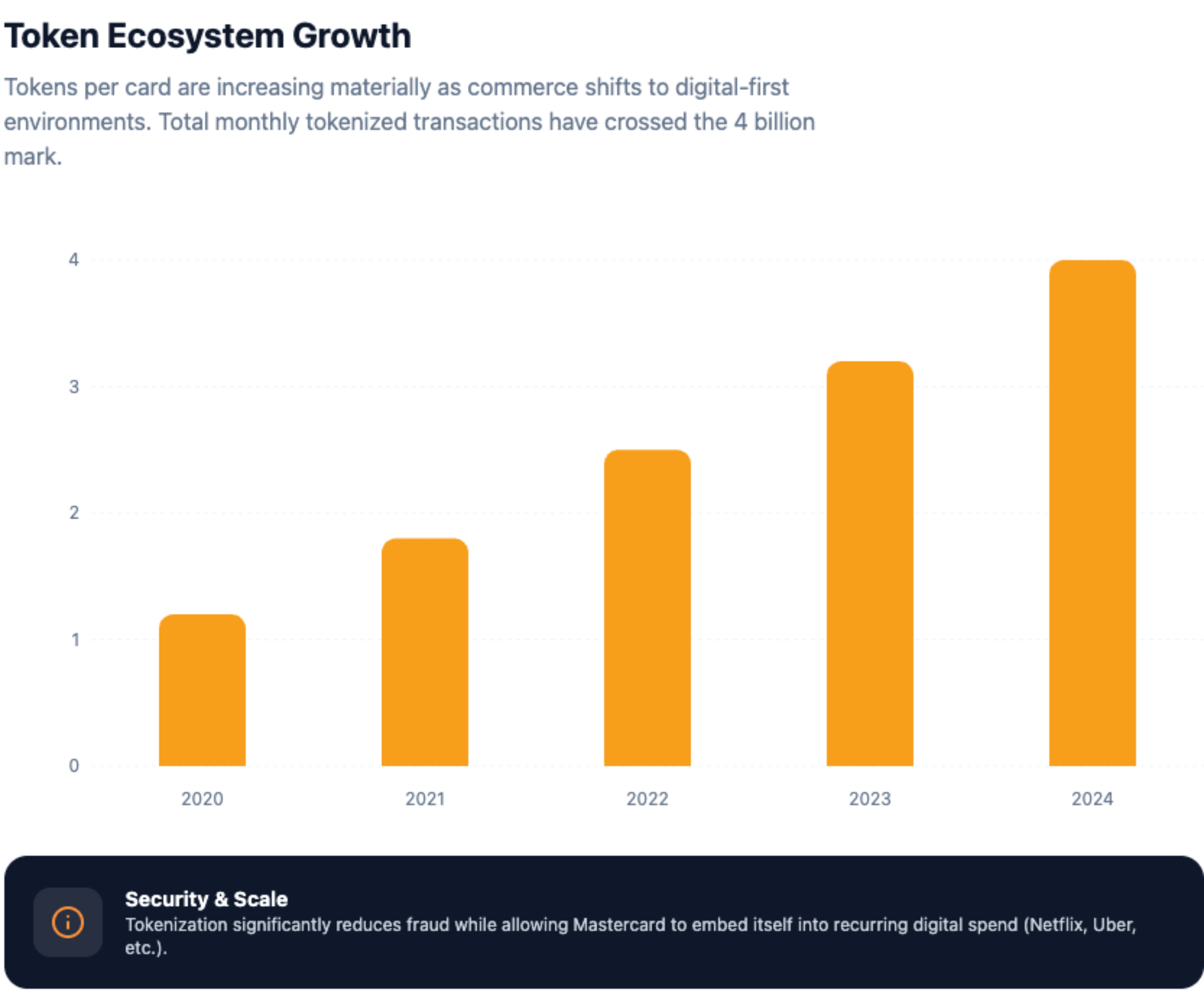

Figure 2: Token Growth / Tokens per Card Graphic

The number of secure tokens linked to each card continues to grow, reflecting Mastercard’s expansion into digital credentials, subscriptions, and embedded payment experiences.

Digital Currencies as an Incremental Opportunity

Digital currencies and blockchain based settlement systems are often presented as alternatives to traditional payment networks. In practice, their adoption in everyday consumer transactions remains limited.

Challenges related to consumer protection, dispute resolution, and user experience have slowed broader acceptance. The absence of chargeback mechanisms and the complexity of managing digital assets create barriers that are not easily overcome, particularly in retail environments where trust and convenience are critical.

Mastercard’s approach has been to integrate rather than compete. The company is building capabilities that allow digital assets to move across its network while maintaining the same standards of security and reliability that underpin its core business. This includes expanding cross border payment solutions and developing infrastructure that supports settlement, foreign exchange, and treasury management.

By incorporating digital currencies into its existing ecosystem, Mastercard positions itself to capture value as these technologies evolve. Rather than representing a disruptive force, digital currencies become an additional layer of growth within a broader and more established system.

Valuation and Market Perception

Despite continued operational strength, Mastercard’s valuation has recently reflected a more cautious outlook from investors. Concerns around regulatory intervention and technological disruption have weighed on sentiment, even as the underlying business continues to perform.

Historically, periods where high quality businesses trade at lower relative valuations have often been driven by uncertainty rather than a deterioration in fundamentals. In Mastercard’s case, revenue growth remains steady, margins continue to benefit from the expansion of higher value services, and cash flow generation remains strong.

This disconnect between perception and performance is worth noting. It suggests that the market may be placing greater emphasis on potential risks than on the company’s demonstrated ability to adapt and execute.

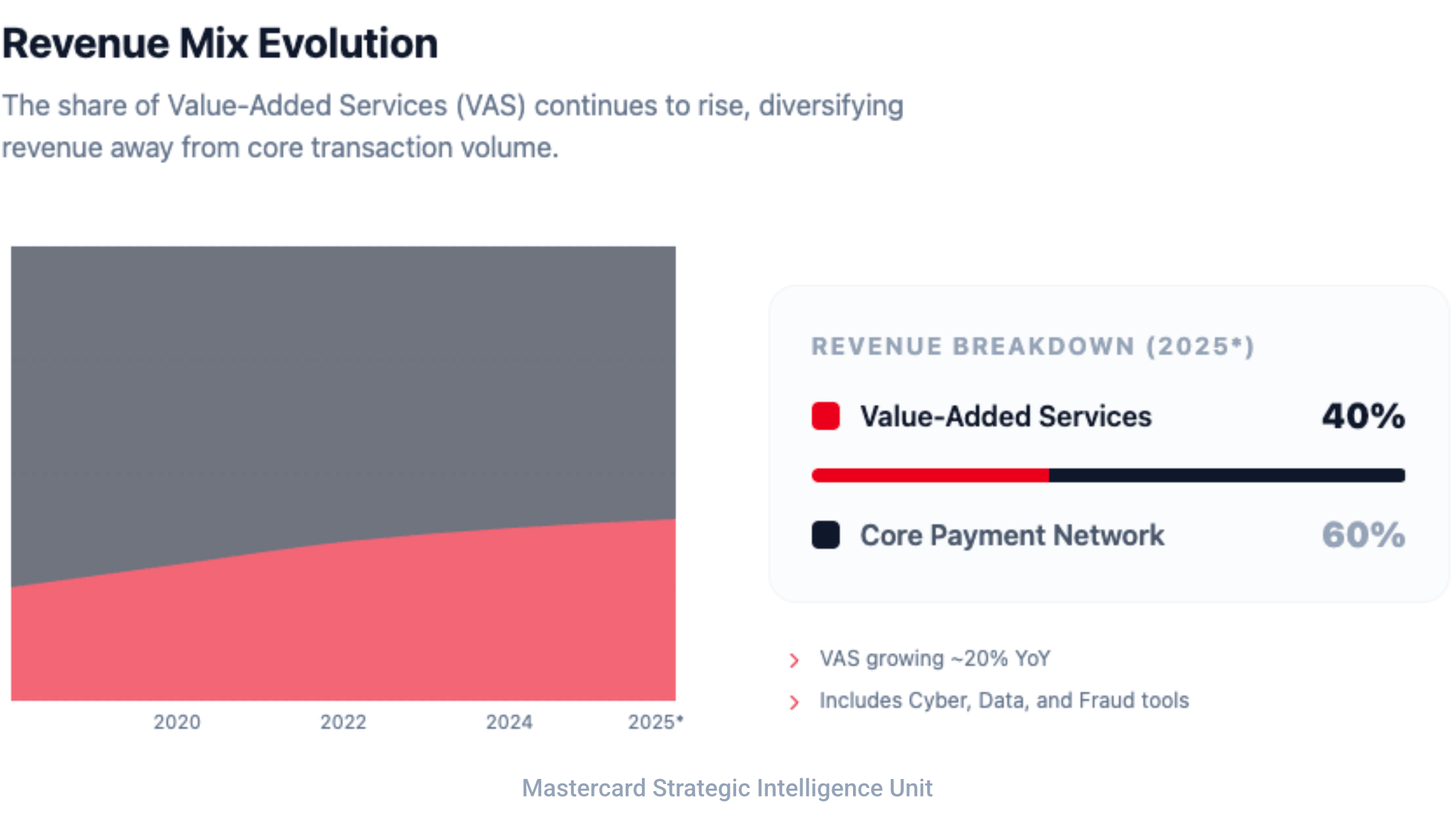

Figure 3: Revenue Mix Chart

Value added services represent a growing share of Mastercard’s revenue, supporting margin expansion and increasing the durability of the business model.

Regulatory Considerations

Regulation represents the most visible near-term risk. Ongoing discussions around merchant fees and competition within payment networks have introduced uncertainty, particularly in North America and Europe.

It is important to recognize that regulatory processes tend to move slowly and often result in incremental change rather than immediate disruption. Even in scenarios where fee structures are adjusted, Mastercard’s global network, relationships with financial institutions, and investment in value added services provide a level of resilience that is difficult to replicate.

The company’s scale and infrastructure mean that any changes are more likely to reshape the economics at the margin rather than fundamentally alter its role within the payments ecosystem.

Our Perspective

At Murray Wealth Group, we focus on identifying businesses that combine durable growth with disciplined execution. Mastercard fits this framework through its global scale, strong pricing power, and ability to generate recurring revenue from multiple sources.

The company’s position within the payments ecosystem allows it to benefit from long term trends that are unlikely to reverse. Commerce continues to shift toward digital channels. Transactions are becoming more automated. The need for security and trust continues to increase.

These are not short-term dynamics. They are structural changes that support sustained growth over time. The payments industry is not being simplified by technology. It is becoming more complex, more interconnected and more dependent on trusted infrastructure.

Mastercard remains central to that infrastructure. Its role is expanding as the system evolves, not diminishing. While near term narratives have introduced volatility, the long-term characteristics of the business remain intact.

For investors who focus on fundamentals rather than headlines, this environment can present opportunities to own high quality businesses at more attractive valuations.