By: Mike Hakes, CFA, MBA

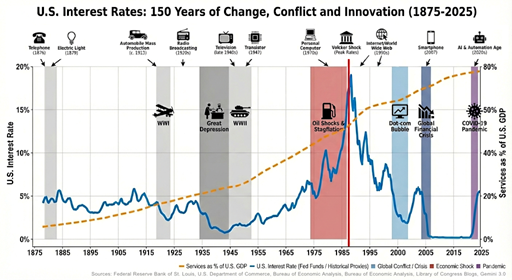

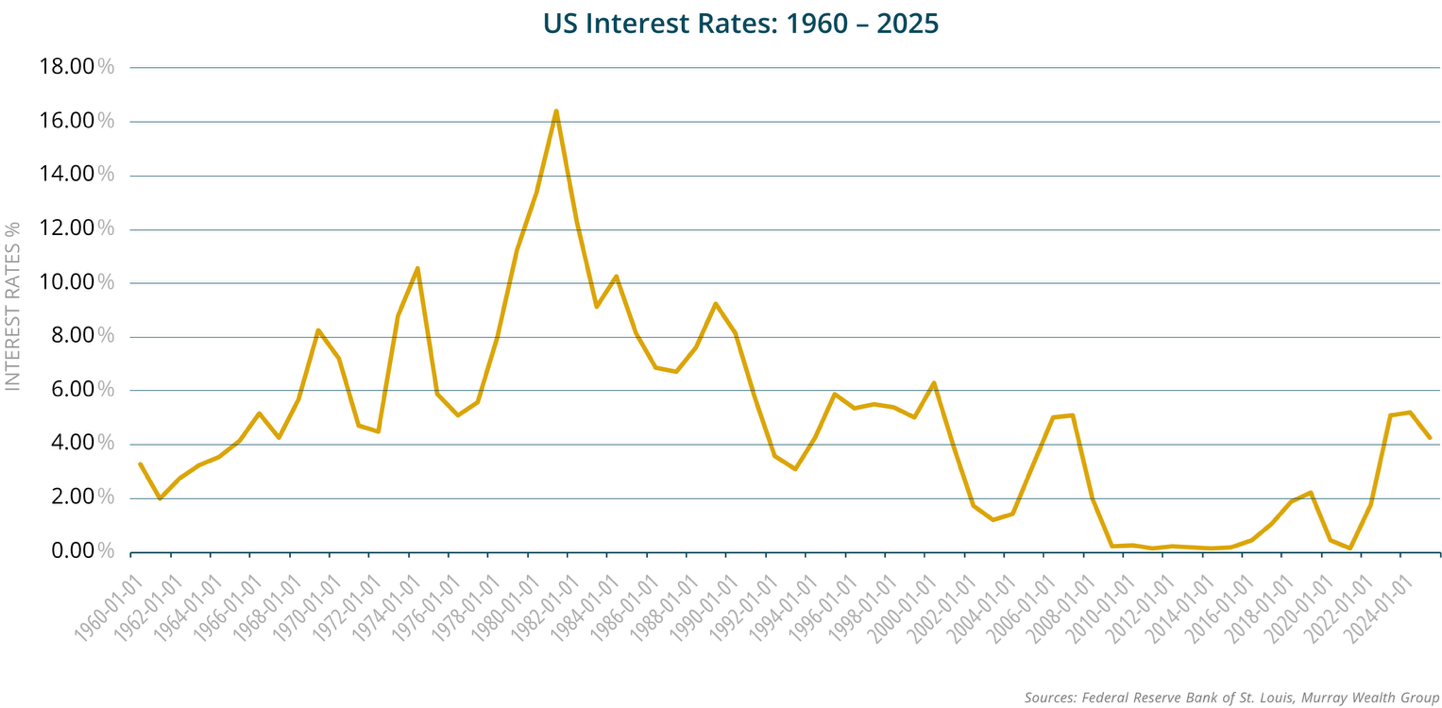

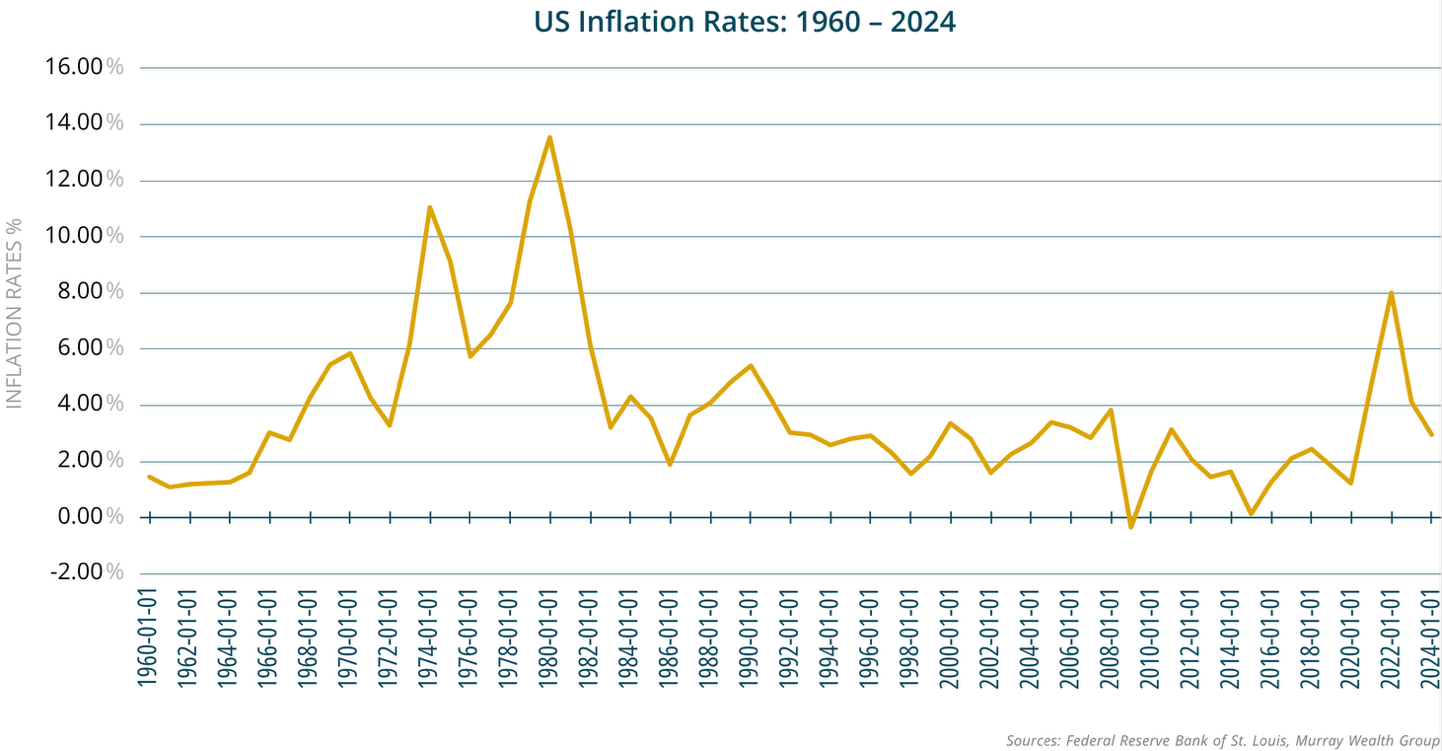

Over the past few years, many economists and central banks have come to believe that interest rates will remain higher for longer. The thinking is straightforward. Global trade is becoming less efficient. Governments are spending heavily. Supply chains are being rebuilt closer to home. All of these forces tend to push costs higher, which can lead to persistent inflation.

This view has become widely accepted in financial markets. Many investors now assume that the era of very low interest rates is behind us.

This assessment presents a different view.

While current policies and global events may support higher inflation in the short term, a powerful structural force is moving in the opposite direction. Advances in artificial intelligence are beginning to reduce the cost of knowledge-based work across the economy. Over time, this could slow inflation and eventually push interest rates lower again.

The Hypothesis

Artificial intelligence will reduce the cost of services, weaken wage growth and lower the economy’s need for borrowed capital. As a result, long-term interest rates are likely to fall back toward pre-pandemic levels within the next several years.

To understand why, it helps to begin with two concepts that central banks use to guide interest rate decisions.

The Two Benchmarks That Shape Interest Rates

Economists often refer to two theoretical benchmarks that help explain where interest rates and employment should settle in a balanced economy.

The first is the neutral interest rate, sometimes referred to as R-star. This is the interest rate that keeps the economy stable. At this level, borrowing costs are not so low that they fuel inflation and not so high that they slow economic growth.

If central banks set interest rates above this neutral level, borrowing becomes expensive and economic activity slows. If they set rates below it, borrowing becomes easier and economic growth accelerates. Many policymakers believe this neutral level has permanently moved higher. The argument in this article is that the opposite is more likely.

The second concept is the natural rate of unemployment, sometimes called U-star. This represents the lowest level of unemployment that the economy can sustain without creating inflation.

When unemployment is extremely low, companies compete for workers and wages rise quickly. Businesses often pass these higher labour costs on to consumers in the form of higher prices.

If technological change allows companies to operate with fewer employees, the economy can grow without pushing wages sharply higher. This tends to reduce inflation pressures.

Artificial intelligence has the potential to influence both benchmarks in important ways.

Artificial Intelligence May Lower the Cost of Services

Technology has historically been one of the most powerful forces holding inflation down.

Over the past several decades, manufactured goods have become steadily cheaper. Televisions, computers and software all cost far less than they once did, even as their quality improved dramatically. This happened because automation allowed companies to produce more with fewer workers and lower costs.

Services, however, have remained expensive. Healthcare, legal advice and consulting services have continued to rise in price. These industries depend heavily on skilled human labour, and productivity gains have been limited.

Artificial intelligence may change this pattern for the first time.

Many service jobs involve tasks such as analyzing information, writing reports, reviewing documents and responding to clients. These activities are increasingly being supported or partially handled by advanced software systems.

When a task that once required a trained professional can be completed faster and at lower cost using technology, the overall cost of providing that service falls. Lower service costs translate into lower inflation across the economy.

Because services make up the majority of modern economic activity, even modest efficiency gains could have a significant impact on inflation over time.

Slower Wage Growth Could Ease Inflation Pressures

Labour costs are one of the most important drivers of inflation. When wages rise quickly across the economy, businesses often increase prices in order to maintain profitability.

Artificial intelligence is likely to affect wage growth by increasing worker productivity.

For example, a software developer who uses advanced software tools may be able to complete projects much faster than before. A financial analyst may be able to analyze large amounts of data in minutes rather than days. A marketing professional may be able to produce content in a fraction of the time.

In these situations, companies may need fewer employees to accomplish the same amount of work.

This does not necessarily mean large-scale unemployment. Instead, companies may simply grow without hiring as many people as they once would have. Hiring may slow and staff reductions may occur gradually through retirements and turnover.

If the supply of skilled workers grows faster than demand, wage growth tends to slow. Since wages are one of the most persistent sources of inflation, slower wage growth can significantly reduce inflation pressures. This would allow central banks to maintain lower interest rates without risking a surge in prices.

A Less Capital-Intensive Economy Could Push Rates Lower

Interest rates are influenced by the balance between savings and investment.

When businesses need to borrow large amounts of money to build factories or infrastructure, demand for capital rises and interest rates tend to increase. When businesses require less borrowed capital, interest rates tend to fall.

Many investors assume that artificial intelligence will require massive investment in new technology infrastructure. Some investment will certainly be required. However, many digital businesses require far less physical capital than traditional industries.

A software-based solution can often be expanded to serve millions of customers without the need for new factories or large physical assets. Once the core technology is developed, growth can occur at relatively low cost.

At the same time, households facing economic uncertainty often increase their savings. Higher savings combined with lower demand for investment capital tends to push interest rates lower.

This combination could gradually reduce the neutral interest rate over time.

What This Could Mean for Investors

The current belief in permanently higher interest rates reflects recent experience rather than long-term structural trends.

Inflation rose sharply after the pandemic due to supply disruptions, strong government spending and labour shortages. These forces are real, but they are unlikely to dominate the economic landscape indefinitely.

Artificial intelligence represents a different kind of force. Instead of increasing costs at the margins, it has the potential to reduce costs throughout the economy.

If productivity improves while wage growth moderates and capital requirements remain modest, inflation is likely to trend lower. As inflation falls, interest rates typically follow.

Over the next several years, investors may begin to see:

- Services inflation gradually slowing

• Wage growth stabilizing

• Central banks reducing interest rates

• Long-term borrowing costs moving lower

The widely held expectation of permanently higher rates may prove temporary.

If technological progress continues at its current pace, the global economy could once again find itself in a period characterized by modest inflation and lower interest rates. For long-term investors, that possibility deserves careful consideration.