There is a lot of talk comparing the current market to that of 1999-2000. True, technology is eating the world, and while the current outlook for further penetration is favourable, the same arguments could have been made about the millennium market (the dawn of smartphones, expanding internet access, better compute efficiency). However, we believe there are substantial differences that make today’s sector much more defensive. As the world entered the new century, there was fear (Y2K) that the large base of installed computer and communications systems was not programmed to handle the new millennium. This was accompanied by the rapid rise of the internet and a plethora of new issues based on ideas for how to use the internet. Many went to large valuations without any real business traction. We also saw a complete rebuild of the world’s communications networks, with a shift from copper to fibre transmission, which led to massive overcapacity. Nortel peaked at about 35% of the S&P/TSX.

Shopify: Consistently “overvalued” from $140 a share in 2018 to $1,400 today

Today, the largest Canadian company listed on the Toronto Stock Exchange is Shopify Inc. at just under 8% of the Index. Shopify powers many e-commerce websites, from large consumer brands like Heinz and Lindt to smaller e-commerce-focused start-ups like Gym Shark and Good American, and has layered in additional services such as payments and fulfillment (such as warehousing, inventory and shipping). The company generated US$1.6B in revenue in 2019, a number expected to grow to US$4.1B in 2022 (37% annual growth). Shopify has not made any profit to date because it re-invests all of its cash back into its growth, so earnings or cash flow-based valuations are not applicable.

In pre-cash flow companies, investors often focus on revenue multiples. On this basis, Shopify trades at an enterprise value/revenue multiple of 74x 2019 revenue. Due to its projected growth, the multiple falls to only 25x in 2022.

It is tough to understate how strongly multiples across the software technology space have expanded in the past three years. Shopify is the poster child for software success, with the shares appreciating by roughly 30x in the past four years. Its market cap of US$109B is US$60B less than Salesforce.com, a mature software superstar that generates US$20B of revenue with 80% gross margins. Salesforce is no old dog either; its revenue is growing 15% per year.

Some quick math: Shopify will need to grow at 30-35% per annum for the next eight years to achieve Salesforce’s current level of revenue. Assuming, for simplicity, that Shopify is valued at a similar multiple, Shopify’s shares will return 7% per annum over the next eight years.

Is it a bubble?

As the tech-heavy NASDAQ soars to new highs, this question is front and center of every investor’s mind. This is not just because many software stocks (like Shopify) have seen valuations expand to record levels; even companies like Amazon, Apple and Microsoft have returned over 100% in the past 18 months. The bull case for technology is simple: internet software is eating the world, and companies that can build a dominant position in large, expanding markets should reap benefits longer term. Today’s technology companies are leaders in innovation, leveraging internet, mobile and cloud computing technology to scale globally. Record low interest rates and government stimulus are also providing reasons to bid up long-term growth assets. It seems like a ‘no brainer’ to invest in technology.

However, when we review the technology bubble of the late 1990s, we find many similarities in both sentiment and opportunity. Below are some excerpts from 1999 annual reports.

- Qualcomm (cellular data chips) – As the wireless industry moves to the third generation (3G), we believe high-speed, high-capacity wireless data is a key driver to future growth.

-

Yahoo (internet search and advertising) – Of the total net revenues for the years ended December 31, 2000, 1999, and 1998, advertising revenue was $1.0 billion, $535.4 million, and $226.3 million, respectively. The increases from year to year are due primarily to the increasing number of advertisers purchasing space on the company’s online media properties as well as larger and longer-term purchases by certain advertisers.

-

Microsoft (personal computing) -The Company’s revenue growth rate was 32% in fiscal 1997, 28% in fiscal 1998, and 29% in fiscal 1999. Revenue growth rates reflected the continued adoption of Windows operating systems and Microsoft Office, particularly as Microsoft software is deployed across entire corporate, academic, and governmental organizations.

-

Amazon (e-commerce) – In the coming years, we expect to benefit from the continued adoption of online commerce around the world as millions of new consumers connect to the internet for the first time. As the online shopping experience continues to improve, consumer trust and confidence will increase, driving further adoption.

All four companies were leaders in technology verticals that have grown strongly from that point, and while Microsoft and Amazon have delivered strong returns over the long term, their shares failed to deliver much return for the next decade if purchased near the peak in 2000. Let’s explore the dynamics of the 2000 technology bubble and compare the past top to the present.

A note about the macro. Before exploring more sector specific themes, it’s worth highlighting a couple of macroeconomic factors that likely explain the technology sector’s higher valuations today and contrast them to 2000 factors.

- Interest rates – the U.S. 10-Year government bond current yields 0.6%. In 2000, the yield peaked at 6.6%. Lower interest rates mean future cash flows are more valuable in present value calculations. Thus, high growth companies see their value appreciate at a stronger rate than during higher interest rate environments.

-

COVID Digitization – The COVID-19 pandemic has accelerated the digitization of corporations as jobs and services must be delivered remotely. Historically, a recession would negatively affect demand as corporates reduce their spending and headcounts, but the unique nature of the COVID pandemic (and government stimulus) has moved many office-based jobs to a work-from-home environment. In 2000, the technology industry was impacted by a reduction in spending from the Y2K preparation initiatives that occurred prior to the January 1, 2000 calendar rollover and a more traditional business cycle recession.

Revenue Durability extremely strong due to business model and industry improvements.

Then: In 2000, Yahoo generated $1 billion of advertising revenue, an 87% increase from the prior year. One would naturally expect that as internet usage continued to expand at a high rate, revenue would continue to grow strongly. Unfortunately, 2001 proved less successful. Revenue fell 44% as the global recession affected advertising budgets and reduced pricing. As well, spending by other internet companies fell or disappeared completely as many companies were financed primarily through equity markets and had no cash flow (or revenue in many cases) to fund marketing.

Telecom and internet routing hardware providers like Cisco also experienced large revenue declines. After growing revenue at 46% per year from 1995-2001, revenue fell 15.2% in 2002. Cisco cited the U.S. economic slowdown, over-capacity and customer constraints as reasons for the decrease. As well, its margins were impacted by inventory write-downs and higher marketing expenses.

Some companies with strong franchises fared better financially. Microsoft and Amazon both saw their revenue continue to increase, but at a much slower rate. As shown below, both companies witnessed strong decelerations in growth in the 1999-2001 period versus the 1995-1999 time frame. As a result, despite their continued growth, the shares of both companies underperformed the broad markets as valuation multiples contracted. Year 2000 Amazon and Microsoft may prove most insightful when analyzing the sector today.

Figure 1: Microsoft and Amazon growth rates (1998-2005)

")

Now: The first significant change from 2000 is the use of the public cloud, which has allowed many companies to reduce their fixed costs and invested capital (by scaling on Amazon AWS or Microsoft Azure). Secondly, many software companies have pivoted to software-as-a-service (SAAS) models where users pay ongoing fees for use and support, providing them with recurring revenue. Previously, licensing models were used, which resulted in prolonged sales cycles and lumpy revenue. Finally, the COVID-19 pandemic, despite its economic turmoil, is accelerating demand for many digital services (work-from-home, e-commerce, etc.), which are more broadly accepted than in 2000. It is worth noting that technology hardware in many cases is correctly viewed as commoditized products, with the attendant declining prices and margins, and thus, companies in this sector have generally not seen their share prices rise proportionally to software stocks.

Thus, we believe the risk to technology equities is a deceleration of growth versus expectations of revenue, rather than an outright decline. Growth could slow from a further weakening of the economy or a post-COVID deceleration as demand is pulled forward from future years.

Case Study – Workday

A perfect current example of the multiple compression that can take place when a company’s growth rate declines can be found in Workday (WDAY). Workday is a very well run company, and this commentary is not an opinion on its future stock price returns. Workday’s revenue has nearly quadrupled from just over US$1B to US$4B in the past five years. Its human resource

and accounting software products are used by leading enterprise clients (such as Netflix, Target and Bank of Montreal, just to scratch the surface). The company is well positioned with best in class products built in the cloud to scale quickly at any organization.

The chart below highlights how attractive an investment in Workday has been over the long term. An investment four or five years ago would be worth double today. However, shares purchased in the last 12 to 18 months are roughly flat (or even down 15% if purchased near the July 2019 peak). In that same period, the NASDAQ 100 is up 40-50%, with other technology and software companies benefitting from the same trends as Workday (Figure 2).

So why has Workday underperformed?

Workday’s quarterly revenue growth accelerated in early 2019 from the high-20% range to the mid-30%. With this acceleration, investors bid up the shares, causing the Enterprise value/Revenue multiple to expand from approximately 7x to a peak of 11x (Figure 3). However, Workday was unable to sustain this high rate of growth (Figure 2). Revenue growth in the next three quarters was in the low to mid-20% range (note that 2020 revenue growth was further exacerbated by COVID-19). Despite the still healthy rate of growth, the deceleration in the growth rate resulted in a 30% drop in the share price. Workday checked all the boxes in the golden age of cloud software but is a reminder that valuation and expectations ultimately drive share price returns.

Figure 2: Workday shares remain below its summer 2019 high while the NASDAQ soars to record highs as its revenue decelerated…

This past earnings season, several cracks in the armour appeared in the software-as-a-service sector, with financial modelling company Alteryx experiencing a 37% drop in its share price as its EV/Revenue multiple fell from 21x sales to 13x sales after it lowered its financial guidance. Other high-flying tech companies have similarly experienced pullbacks in their shares despite posting earnings results that were above expectations.

Figure 3: Revenue Multiple Compression at Workday and Alteryx.

The path forward from here.

It is normal for stocks to consolidate after a strong move higher, which can lead to under-performance and lower the probability of triple-digit returns for a short period of time. But the secular trend towards digital, usage-based, recurring sales models being adopted by tech companies today provides much stronger visibility going forward. Thus, we don’t see a bubble. We do, however, believe it is important to continuously evaluate the future growth expectations of these companies to have confidence in their potential for strong investment returns.

Global Growth Fund Technology Holdings

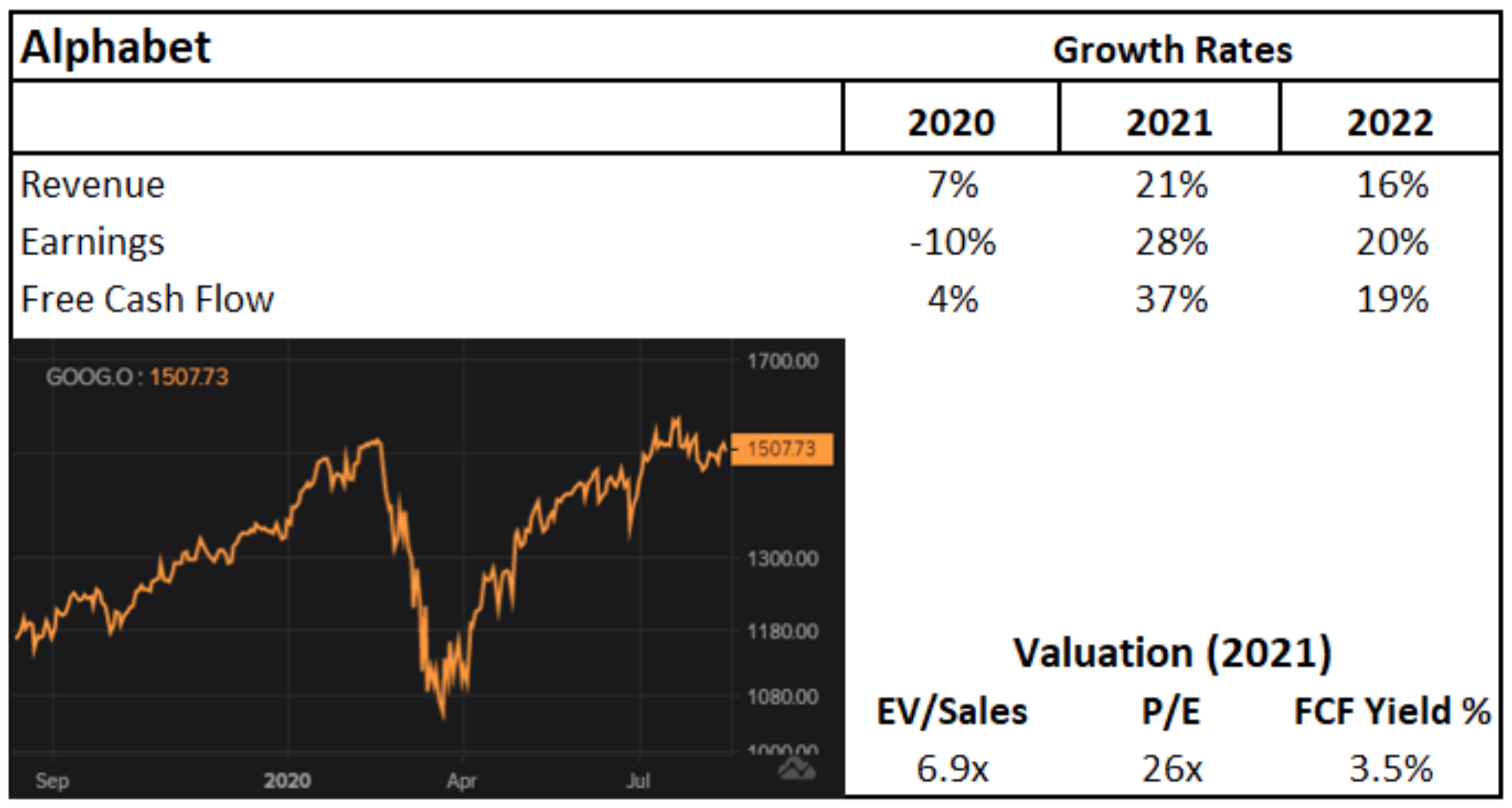

Alphabet

Alphabet is our largest holding in the Global Growth Portfolio, with a 6.5% weight. Revenue growth has slowed due to the impact of COVID-19, but its core Google search property should retain its leadership position with additional monetization from its Google Maps property. Youtube and Google Cloud are additional growth drivers. The company has historically grown its revenue close to 20% per year. However, its valuation has compressed as the market starts to look at a mid-teens growth rate in the near term. At a 26x P/E and with a core product that remains the basis of finding things on the internet, we do not see risk of a large pullback.

Facebook has emerged from its data privacy issues stronger and with a renewed focus on revenue growth. The company has created additional monetization opportunities with its Shops (online storefront) and Reels (Tik Tok clone). The company’s low P/E ratio relative to its growth rate implies that the market has low expectations regarding the durability of Facebook’s revenue growth. However, we believe in CEO Mark Zuckerberg’s capital allocation abilities and expect Facebook will continue to dominate small business marketing as COVID-19 strengthens its competitive position.

Microsoft

Contrary to Alphabet and Facebook, Microsoft has seen its multiple expand from a P/E of 10x in 2011 to 25x in 2018 to 32x in 2020. The multiple expansion is due to its Azure Cloud Services division, which along with Amazon AWS, dominates cloud computing and is integral to the digitization movement. The division is now on a $20B revenue run-rate, and margins continue to grow as its datacenter utilization improves. We view moderate risk of a pullback in Microsoft shares as its PEG ratio (P/E ratio divided by earnings growth rate) is now solidly over 2.0x. However, we believe consensus estimates for revenue growth may still prove conservative.

Amazon

Amazon has always been a controversial stock as the company reported very little profit or free cash flow even just five years ago. Great managers know that turning a profit carries only one certainty: a tax bill. However, the growth of both its advertising and AWS cloud computing divisions, as well as inroads in its core retail businesses (prime, delivery and 3rd party retail), has created a tsunami of cash flow that the company is unable to fully re-invest (its current cash balance is a company-high US$71B). Amazon has always been difficult to value on a fundamental basis, but at a 2.8% cash flow yield, it is in line with its mega-cap technology peers despite its strong year-to-date performance (up 72%).

Netflix

As we move down the company maturity curve, we typically hold smaller weights, as we believe there is increased volatility. Our 2% weighting in Netflix versus 5.5-6.5% for larger, more mature, cash-flowing companies is in line with this rationale. However, it is clear that Netflix is going to be a dominant player in the media space and is benefitting from COVID-19. Moreover, while its subscriber additions can be volatile, it is unlikely the company will see a collapse in demand as it produces more content than any other media company and leverages its global distribution base.

Twilio

Twilio is the company that could easily be described as frothy from a valuation perspective. The shares have risen 150% from our initial purchase in late April. The company, which provides communication abilities to website and app developers, has benefitted from the digitization trend as a rush of companies expedite online services. The company grew revenue through the first half of 2020 by 50% over 2019. However, looking to 2021/22, consensus estimates are calling for 25% and 23% revenue growth. If Twilio cannot meaningfully outgrow larger technology companies like Facebook and Netflix over the long term, its multiple will likely compress (the stock was more attractive at our initial purchase price of US$120 than its current price of US$240). We remain cognizant of this risk and have been reducing our exposure to Twilio by rebalancing to our target weight of 2% at opportunistic prices. We have nearly recouped our initial investment in Twilio while maintaining a 2% position weight.

This time, “it’s different” is a dangerous phrase in investing, and we are cognizant of the excesses in today’s market such as electric truck or space companies valued at billions of dollars with no revenue in sight. However, unlike 2000, today’s technology companies are providing mission-critical software to corporations or are new age media companies, dominating advertising and content consumption. We still see lots of running room in advertising, content, cloud services and e-commerce. This, combined with our companies’ strong financial positions, leads us to believe that positions in these companies will benefit our investors in the next decade.