Digital Rent is Due!

A big investment theme for the next decade is the shift to digital living from physical. We are learning that we can complete many tasks more effectively through computing intermediaries. Remote meetings and online conferences eliminate travel and commercial space requirements, telehealth provides safe and quick access to medical professionals, and perhaps the largest category, e-commerce allows us to shop an unlimited selection of goods from our couch.

As eyeballs have swiftly moved to mobile, advertising dollars have also moved online. It makes sense – you can better tailor ads to the right target market and, unlike a newspaper or tv ad, a customer can mouse click ~10 times to have the item delivered (potentially in as quickly as 2 hours) versus remembering to purchase the item at the store next time they are out.

There are only so many pairs of shoes or Superpuff jackets to be sold, so it reasons that every item purchased online takes the place of an item that would have been purchased in the store. As marginal goods move online, physical store economics deteriorate. Over time, this pain will be shared by all who play in the physical retail space through a lowering of costs to ensure investment returns meet costs of capital (both retail brands and real estate affected– as prodigiously laid out by Simon Wolfson, CEO of Next PLC on pages 7-9 of his annual report).

Certainly, last-mile delivery costs eat into part of e-commerce profits but there are also economies of scale in distribution. Thus, e-commerce appears to be much more profitable than physical retail for many items. And as companies like Shopify and Zalando reduce barriers to entry with online storefronts and drop shipping, e-commerce is in the midst of a large land grab to establish brands online in a world of equitable distribution capabilities.

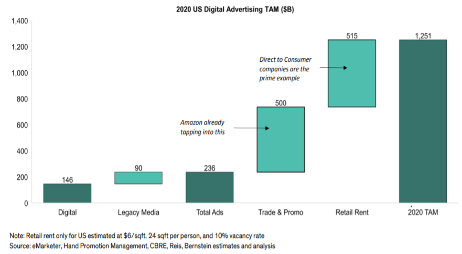

While digital provides better economics, brands still need to acquire customers. Enter Facebook and Google. Both companies are in position to help brands generate sales online; they are the de facto 5th Avenue of customer acquisition. Google has the ability to place services in front of customers to meet their needs. It is the ultimate sales tool. Facebook is slightly more traditional, although the company is making a strong push as a demand creator through Instagram shops. Adding it all up, Bernstein Research attempts to estimate the true size of the digital advertising market to have a TAM (Total Available Market) of $1251 billion. They estimate that not only traditional advertising dollars, but costs traditionally allocated to rent and trade promotions are up for grabs as well. This means we are still in the middle of a long cycle of digital spending. Facebook and Alphabet (Google’s parent company) are the two largest positions in our Global Equity Growth Portfolio.

This Focus Stock is written by our Head of Research, Jamie Murray.

The purpose of this is to provide insight into our portfolio construction and how our research shapes our investment decisions. As always, we welcome any feedback or questions you may have on these monthly commentaries.