Air Canada is being priced for a problem it has already solved. The prevailing view still reflects a pandemic-era reality. Excess leverage, heavy dilution and structural fragility continue to define the narrative. That framing is increasingly disconnected from the underlying business.

Category Archives: Market Insights

2026 Market Outlook: Volatility, AI Investment and Geopolitical Risk

Why market volatility, earnings growth and global conflict are shaping investor strategy in 2026

This commentary reflects market conditions and available information as of Tuesday, April 7, 2026. Given the pace of recent geopolitical and market developments, some data points or events may have evolved since the time of writing.

Equity markets continue to demonstrate a clear underlying bias toward growth. However, geopolitical conflict and uncertainty surrounding artificial intelligence are creating hesitation among investors. The challenge is not a lack of opportunity, but a lack of clarity around outcomes.

Company Spotlight: Mastercard

Rethinking Disruption in Payments

Is fintech disruption truly a threat to Mastercard or could it ultimately reinforce its position?

Recent headlines have created a narrative that the payments landscape is on the verge of being reshaped by artificial intelligence, digital currencies, and regulatory pressure. The concern is that new payment rails will bypass traditional networks and erode the economics of companies like Mastercard. While this argument appears logical at first glance, it overlooks what Mastercard actually does and why its role becomes more important as the system evolves.

Mastercard does not manufacture a product that can be easily replaced. It operates a global infrastructure that enables secure and trusted transactions across millions of merchants, financial institutions, and consumers. As commerce becomes more digital and increasingly automated, the need for that infrastructure grows rather than declines. Read

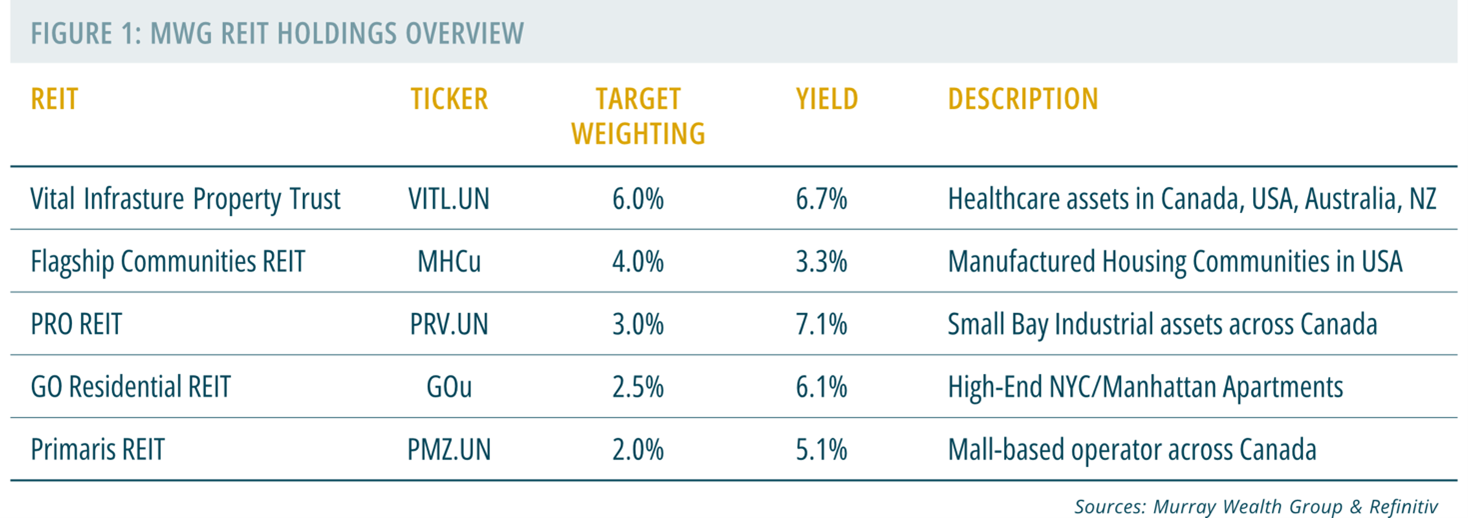

Industry Insights: Identifying Value in REITs Through Supply and Demand Dynamics

Real estate has long been defined by a simple principle: location matters. Investors instinctively gravitate toward assets in established, high-demand markets, whether that is a beachfront property or a well-positioned hotel in a central district. What ultimately defines a “prime” location is the balance between supply and demand. Strong demand paired with limited availability tends to support both pricing and long-term value.

Over time, however, markets adjust. Rising prices attract new development, and what was once considered secondary can quickly evolve into the next area of focus. A nearby stretch of undeveloped coastline, or a newer, more modern asset can shift demand patterns in meaningful ways. This constant rebalancing is what creates opportunity for disciplined investors.

Within the MWG Income Growth Fund, we focus on high-quality income-generating businesses that also offer underappreciated growth potential. In recent months, we have been identifying compelling opportunities within the Real Estate Investment Trust (REIT) sector. Specifically, we are finding value in REITs where units trade at a discount to underlying property values, and where supply and demand dynamics within specific sub-sectors remain favourable.

We have maintained positions in Vital Infrastructure Property Trust (formerly Northwest Healthcare Trust), PRO REIT, and Flagship Communities for several years. More recently, in February, we added positions in Primaris REIT and GO Residential REIT. In the sections that follow, we outline the underlying market dynamics that support our investment thesis across each of these holdings.

A More Strategic View of Tax Season

Reframing tax season as a moment to assess structure, not just settle outcomes.

Tax season is often approached as a retrospective exercise focused on filing, reconciling and moving on. In practice, it offers something far more valuable.

A completed tax return provides one of the most comprehensive financial snapshots available, capturing how income, investment decisions and structural choices have interacted over the past year. It often reveals inefficiencies that are otherwise difficult to identify.

While key contribution deadlines may have passed, the opportunity to refine strategy has not. For investors with growing and increasingly complex portfolios, this is the moment to shift from compliance to coordination.

The AI Selloff May Be Missing the Bigger Opportunity

Investors fear artificial intelligence could disrupt the technology sector. The evidence suggests it may strengthen it.

AI is wonderful. AI made this comic (after several re-prompts). However, the pace of improvement the technology is driving is beginning to worry investors. Artificial intelligence has quickly become one of the most powerful technological forces shaping the global economy. Its rapid advancement has delivered meaningful productivity gains and enormous wealth creation. Yet the same progress that excites technologists is beginning to unsettle investors.

As my colleague wrote last week, in his piece about the commoditization of white-collar work, markets tend to react negatively to uncertainty. When a new technology appears capable of reshaping entire industries, the first reaction is often fear that existing business models could become obsolete. Artificial intelligence is now triggering exactly that kind of response.

In recent months investors have begun asking a difficult question. Will AI simply improve productivity, or will it fundamentally disrupt the technology companies that built today’s digital economy?

That distinction matters greatly for markets. Read

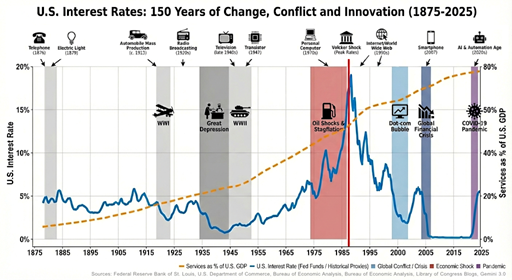

The Deflationary Horizon: Why Artificial Intelligence Could Bring Interest Rates Back Down

Over the past few years, many economists and central banks have come to believe that interest rates will remain higher for longer. The thinking is straightforward. Global trade is becoming less efficient. Governments are spending heavily. Supply chains are being rebuilt closer to home. All of these forces tend to push costs higher, which can lead to persistent inflation.

This view has become widely accepted in financial markets. Many investors now assume that the era of very low interest rates is behind us.

This assessment presents a different view.

While current policies and global events may support higher inflation in the short term, a powerful structural force is moving in the opposite direction. Advances in artificial intelligence are beginning to reduce the cost of knowledge-based work across the economy. Over time, this could slow inflation and eventually push interest rates lower again.

Alamos Gold and the Case for Growing Production and Cash Flow

Investment Spotlight: Alamos Gold and the Case for Growing Production and cash flow

Gold prices have climbed sharply over the past two years, and while daily headlines often focus on tariffs, trade disputes and political tensions, the forces supporting gold today run deeper.

Across much of the Western world, governments are running larger deficits while defense spending rises meaningfully. NATO countries are expanding military budgets, while fiscal policy in the United States, Canada and Europe continues to support elevated government borrowing. At the same time, significant investment is being directed toward building AI infrastructure, another capital-intensive effort requiring large-scale funding.

Long term, AI-driven productivity gains should prove deflationary. In the near term, however, this combination of government spending, infrastructure investment and supply chain disruption creates inflationary pressure that is likely to persist over the next several years.

Add to this the impact of sanctions on Russian energy supplies and continued geopolitical uncertainty, and the case for sustained strength in gold prices becomes clearer. In that environment, gold producers capable of increasing production while managing costs effectively stand to benefit. One such company worth examining is Alamos Gold.

Doman Building Materials: A Shelter from the Storm

The forestry sector is notorious for its boom/bust volatility, with 2025 proving to be no exception. Sinking lumber prices, tariffs and trade disputes, as well as an anemic homebuilding outlook in North America have driven the sector to multi-year lows. However, we believe there is an attractive opportunity in Doman Building Materials. The company offers a compelling counter-narrative: a steady, dividend-paying logistics play that is insulated from the violent swings of commodity prices.

Playing the Supply Chain Recovery Through Linamar

We continue to get reports from across the industrial sector that supply chain issues are still restraining production to below pre-pandemic levels. Recent news like the Nexperia chip shortage and NY aluminum plant fire are reflective of these reports. The automotive industry is the largest in the industrial sector, accounting for 3.5% of the US GDP. Thus, we decided to take to look at available statistics for the industry.

Read

Aritzia: Rise of the Flagship

In an era defined by digital commerce, Aritzia is proving that the in-store experience is more critical than ever. The brand is making a significant investment in experiential retail with the launch of massive, beautifully designed flagship stores that act as powerful brand billboards. This deep dive into Aritzia’s expansion sets out how this physical retail strategy is central to its success, creating an immersive environment that drives brand loyalty, captures high-value customers, and creates a halo effect that boosts its online sales and supports its ambitious plans for international growth.

Flagships on the rise

We recently had the opportunity to visit Aritzia’s new Flagship Boutiques in New York City. Aritzia has a strong presence in New York City, with four locations in Manhattan (its first NYC store opened in 2012). The two flagship stores commenced operations in late 2024 and represented the strategic relocation of established boutiques within their respective areas. A third Flagship is slated to open in the Flatiron District this fall. Read

The Bedrock of Earnings: Why Profits Justify Prices

The current market, with a few technology giants driving U.S. equities to record highs and the excitement surrounding Artificial Intelligence (AI), has led many to question whether we are seeing a repeat of past irrational exuberance, or if this rally is built on a solid foundation. In our view, a financial bubble is defined by rapidly rising asset prices, extreme valuations disconnected from profits and increased systemic risk. The central thesis of this analysis is that the current bull market is being primarily propelled by an extraordinary expansion in corporate earnings and cash flow rather than a widespread investment in unprofitable ventures.

Today’s market’s leaders, which now account for 40% of the index’s market capitalization, possess immense financial strength and are funding innovation sustainably through their own cash flow, establishing a crucial anchor to value. The engine of this growth is clearly the “Magnificent 7” ,which in 2023 were responsible for the entirety of the S&P 500’s net earnings growth; without them, aggregate earnings would have been negative. This highlights that the market’s strength is not from broad-based speculation, but a concentrated surge in the profitability of a select few dominant enterprises. This two-tiered market indicates that the primary vulnerability of today’s market is a downturn in a few key names rather than the systemic froth of a speculative bubble. Read

Canadian Banks: What is the Upside

Canadian banks have rallied to the highest multiples since 2011. At that time, our Canadian banks were viewed as a safe bet as much of the rest of the world faced the hangover from a global financial crisis triggered by excessive real estate pricing and lending in the U.S. housing market. Canada, which avoided the 2008 crisis, may now face the consequences of overvalued housing here at home. Banks have traditionally commanded lower P/E multiples due to the substantial leverage inherent in borrowing and lending large sums. Given the leverage built into global banking systems, when things go wrong, they can unravel quickly, with equity capital disappearing within weeks, as happened in 2008.

Read

Into the autumn, here we go. A slowing economy will get lower rates

The markets have had an impressive year to date despite the panic associated with “Liberation Day” and the massive tariffs imposed on so many of the USA’s trading partners. While fear of economic collapse mounted, it has thus far not materialized. Delays in implementing the tariffs and corporate stockpiling have kept the economy moving along. As you are aware, here at The Murray Wealth Group, we wrote about the panic selling in the late spring a buying opportunity.

Read

Canada’s Hidden Growth Engines: Energy, Gold, and Resilient Consumers

Read

Note From Bruce: Donald Trump’s Tariff War – Should I sell or should I buy?

|

Investor Update: U.S. Tariffs and Global Trade Tensions

Written by President, Jamie Murray, CFA.

Yesterday, the Trump Administration enacted an executive order imposing tariffs ranging from 10% to 54% on imports from most countries. Canada and Mexico were spared in this latest round, continuing to trade tariff-free under USMCA for most goods — though steel and aluminum remain exceptions. Equity markets responded sharply, posting their worst single-day performance since the early days of the COVID-19 pandemic. In light of this, we wanted to share our perspective with investors.

Read

MWG Focus Stock: Northwest Healthcare REIT

Northwest Healthcare REIT

Written by Head of Research & Portfolio Manager, Jamie Murray, CFA.

We own units of Northwest Healthcare Properties REIT (NWH) in our Income Growth Fund. NWH is a globally diversified healthcare real estate investment trust (REIT) focused on owning and managing a portfolio of healthcare facilities such as medical office buildings (MOBs) and hospitals. The REIT has operations in Canada, the United States, Brazil, Australia/New Zealand and Europe (it recently divested its operation in the United Kingdom). Read

MWG Focus: Interview on Stockpick.com!

Mid-Month Market Insights

Investors Club: StockPick.com interview with Senior Portfolio Manager, Michael Hakes, CFA, MBA.

MWG Focus: September Volatility

September’s Volatilty

We believe it’s a buying opportunity

Written by CEO & CIO, Bruce Murray, CFA.

MWG Focus Stock: Uber

Uber and the Age of Autonomy

Written by Head of Research & Portfolio Manager, Jamie Murray, CFA.

MWG Focus: Market Timing

Perfect Timing for the Mid Month

Written by Senior Portfolio Manager, Michael Hakes, CFA, MBA.

This month, we are taking a break from our usual discussion of individual stocks. What better time than now, during a new paradigm (Gen AI), economic uncertainty, political uncertainty and climate change to talk about market timing? Read

MWG Focus Stock: Qualcomm

Qualcomm (QCOM-Nasdaq)

Written by CEO & CIO, Bruce Murray, CFA.

Qualcomm was founded in the mid-1980s and emerged as the leading cellphone technology company with its branded “Snapdragon” line of communication chips in the 1990s. Its CDMA (code-division-multiple-access) technology, patented in 1986, became the standard for leading cellphone networks. Cell phone manufacturers such as Apple and Samsung became Qualcomm’s major customers. Ericsson’s competing TDMA (time-division-multiple access) technology fell by the wayside as it could not match CDMA’s network capacity. CDMA can carry a massive volume of wireless data and differentiate by assigning a code to each call or data user, simultaneously allowing large numbers of network users. TDMA assigns network time to each user thus restricting volumes. Qualcomm’s fortunes moved forward with each leap (generation) of cellphone technology. The rally in the stock price from 2020 to 2022, as seen in Figure 1, was reflective of the rollout of 5G technology, which you likely have in your cellphone if it was purchased in 2020 or later. Read

MWG Focus Stock | Aritzia

Aritzia

Written by Portfolio Manager & Head of Research, Jamie Murray, CFA.

Aritzia – Refreshing Our U.S. Growth Thesis.

MWG Focus Stock: Kingfisher

Kingfisher

Written by Senior Portfolio Manager, Michael Hakes, CFA, MBA.

MWG Focus: Technology Investing

Technology Investing

Written by our CEO & CIO, Bruce Murray, CFA.

Today vs. dot-com & Y2K

Thirty years ago, we were witnessing the adaptation of the internet in the early stages of acceptance as a tool to enhance work and leisure. This led to a plethora of ideas as to what this new technology could do! All it took was an idea and the ability to code and you too could change the way the world worked. By the year 2000, we were at the peak of the dot-com bubble. Like a horse race, Yahoo, based upon “search” software developed in Waterloo by OpenText, surged to the lead, only to be overtaken by a better idea, Google. For a while, @AOL.com was the hottest email host to have, but it then crashed and burned as internet service providers offered complementary addresses as part of their service. Everything was moving online, and providers were going public. By the spring of 2000, it became clear that many of these ideas were not commercial and even the good ones were overvalued. Shareholder enthusiasm quickly plunged into despair. Read

Focus Stock: 3i Group plc

3i Group plc

Written by Head of Research & Portfolio Manager, Jamie Murray, CFA.

Maximizing Tax Efficiency in 2024

Maximizing Tax Efficiency in 2024: A Comprehensive Guide

Written by The Murray Wealth Group

As we begin 2024, it’s prime time to strategize and ensure you’re making the most of available tax-saving opportunities. Read

MWG Focus Stock: Target (TGT)

Target

Written by Senior Portfolio Manager, Michael Hakes, CFA, MBA.

Not Your Average Growth Stock

We recently added Target to the Global Growth portfolio at a 2% weight. The stock has pulled back from its high of $260 in late 2021 and is now trading around $110. Target is not a typical growth company per se as it is a mature retailer in a competitive market. We believe, however, there is the potential for substantial cyclical recovery over the next 12-18 months. As part of our risk control process, we monitor the overall characteristics of the portfolio to ensure it continues to maintain a strong secular growth profile. Read

MWG Focus Stock: Whitecap Resources

Whitecap Resources dollar cost averaging into its inventory.

Dollar cost averaging (DCA) is a simple investment strategy first coined by Benjamin Graham in his book The Intelligent Investor. A DCA strategy calls for investing an equal dollar amount every period, which helps diversify the purchase price (or book value) of an investment. It reduces the effect of market timing and ensures new purchases are made throughout the investment cycle. It has been shown to be an effective strategy for generating steady long-term returns when used consistently. Read