Category Archives: Portfolio Updates

February 2026 Portfolio Review

Markets Navigate Geopolitics and Sector Rotation

Geopolitical tensions returned to the forefront of global markets in February as conflict involving the United States, Israel and Iran introduced renewed volatility across energy markets and broader risk assets.

Oil and gasoline prices moved higher as markets reacted to potential disruptions to Persian Gulf supply. While the situation remains fluid, recent intelligence suggests Iran’s military capabilities may be deteriorating. Should this lead to a normalization of regional energy exports in the coming weeks, some of the recent pressure on oil markets could ease and help stabilize investor sentiment.

Looking further ahead, the macroeconomic backdrop continues to reflect a combination of geopolitical realignment and fiscal expansion. Governments around the world are increasing defense spending and infrastructure investment, trends that are likely to keep inflation modestly elevated over the medium term.

While inflation has moderated from peak levels, tariffs, commodity costs and ongoing supply chain adjustments continue to place upward pressure on prices. At the same time, uncertainty surrounding U.S. trade policy has weighed on corporate capital spending decisions and may partially explain the softer pace of job growth observed in recent economic data.

Despite these headwinds, several structural growth drivers remain firmly in place. Large-scale infrastructure investment tied to artificial intelligence (including data centers, power generation and semiconductor manufacturing) is expected to support economic activity for years to come.

Against this backdrop, we continue to see compelling long-term opportunities across sectors linked to AI infrastructure, natural gas, defense, healthcare innovation and commodities, while maintaining a disciplined approach to managing macroeconomic risk within the portfolios.

January 2026 Portfolio Review

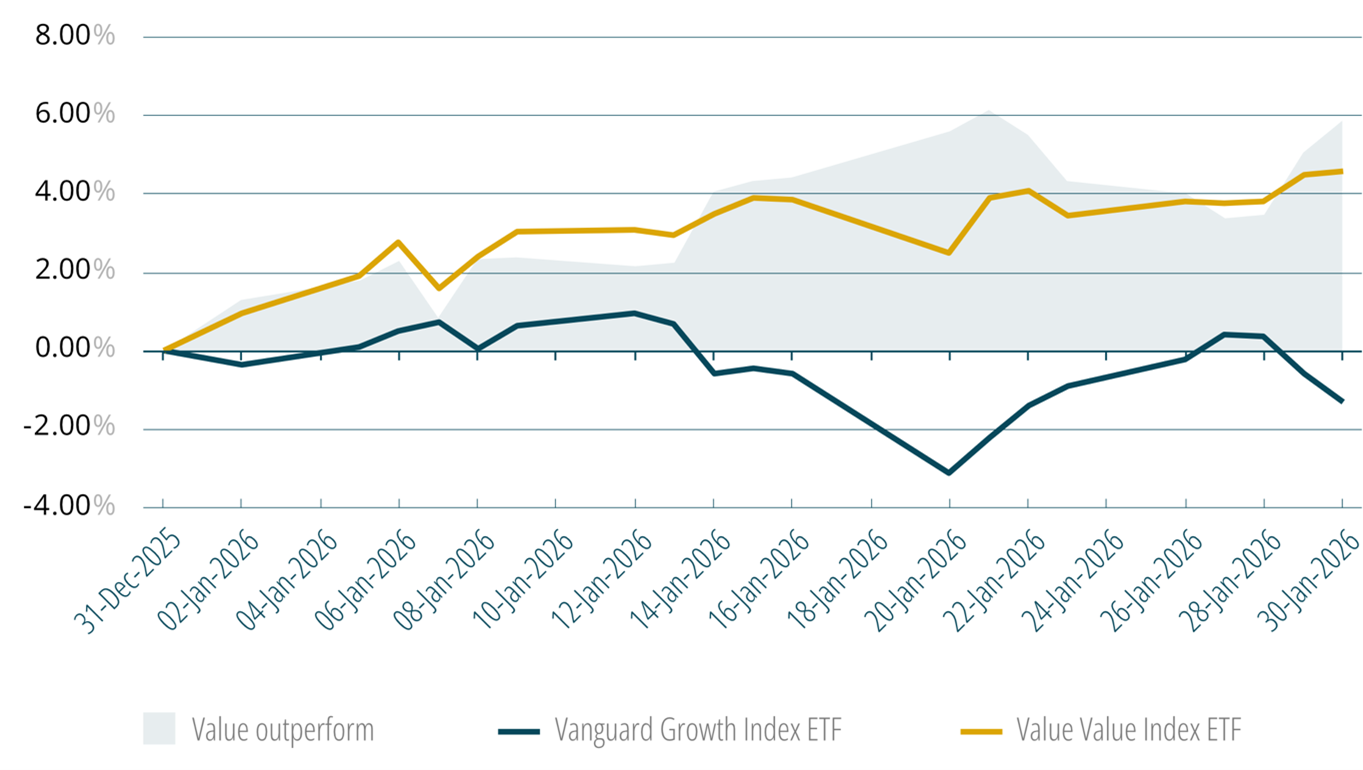

Any seasoned bargain hunter knows the best deals often appear just after the holidays, when unwanted inventory is marked down because, by spring, no one is looking for fuzzy socks or eggnog candles.

Markets saw a similar dynamic this January. Investors stepped in to purchase value stocks — companies trading at meaningful discounts to faster-growing technology names and premium global franchises.

In January, the Vanguard Value Index ETF rose 4.6%, led by commodity, mining, and financial stocks. Growth stocks, represented by the Vanguard Growth Index ETF, fell just over 1%, resulting in a notable 6% outperformance by value stocks.

International markets, particularly Europe and Japan, tend to carry more value characteristics, so their outperformance was not surprising, especially with the weakening U.S. dollar providing an additional tailwind.

Figure 1. Value outperformed Growth by 6% in January 2026

Source: Murray Wealth Group, Refinitiv Workspace

December 2025 Portfolio Review

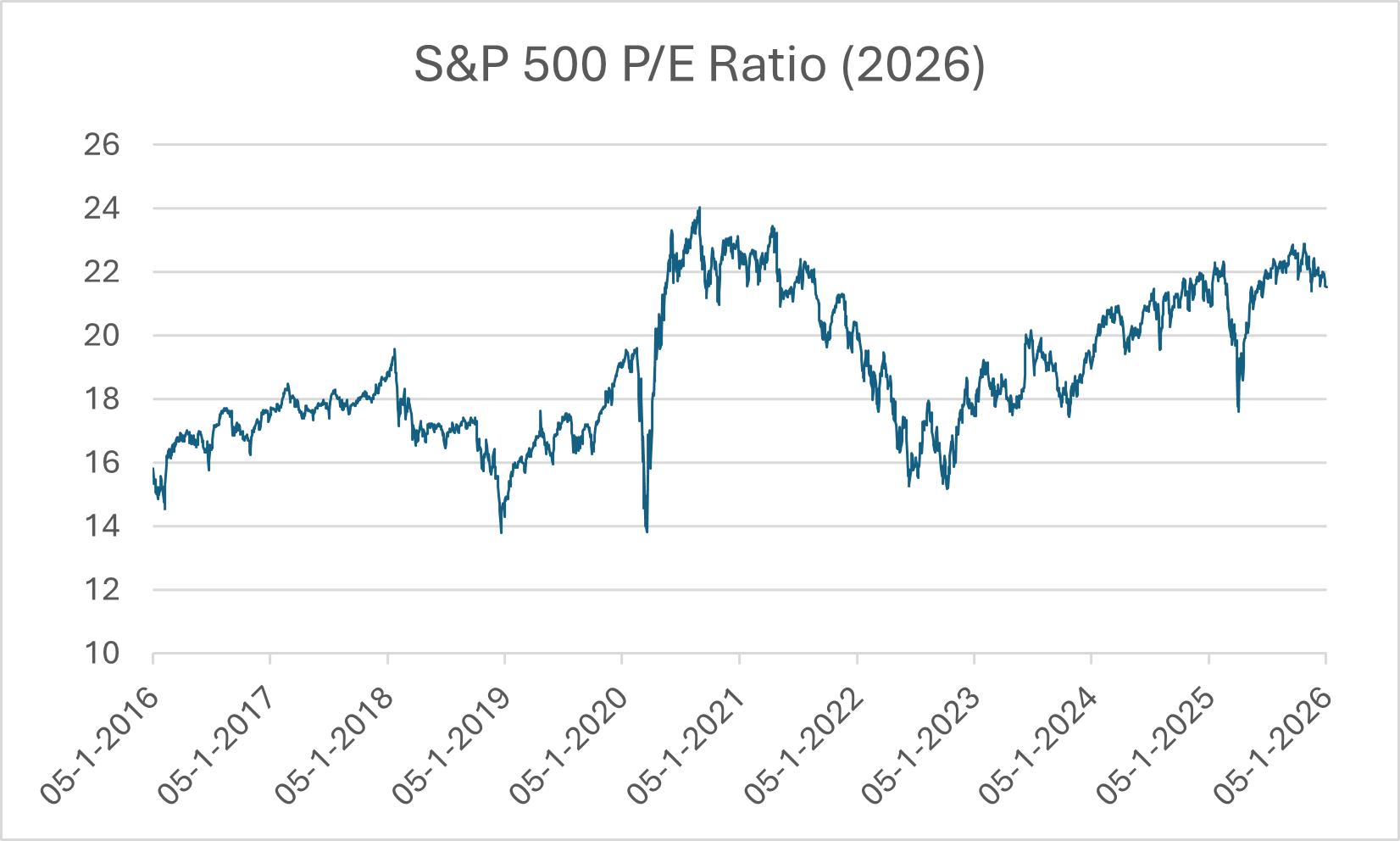

The benchmark S&P 500 index closed near all time highs, returning 16.4% in 2025. This makes the third year in a row with double digit returns and adds to a strong run since 2018 with 6 out 7 years eclipsing 10%. It is natural for an investor to wonder how this can continue from an initial glance, there are flashing lights. The forward P/E ratio for the S&P 500 is 22x, a level that often marks the top of the cycle, not the start. As well, index concentration (the top 10 constituents make up 39% of the index) is at extreme levels only seen in previous cycles.

Figure 1: S&P 500 P/E Ratio over time

Source: Murray Wealth Group, Refinitiv Workspace

November 2025 Portfolio Review

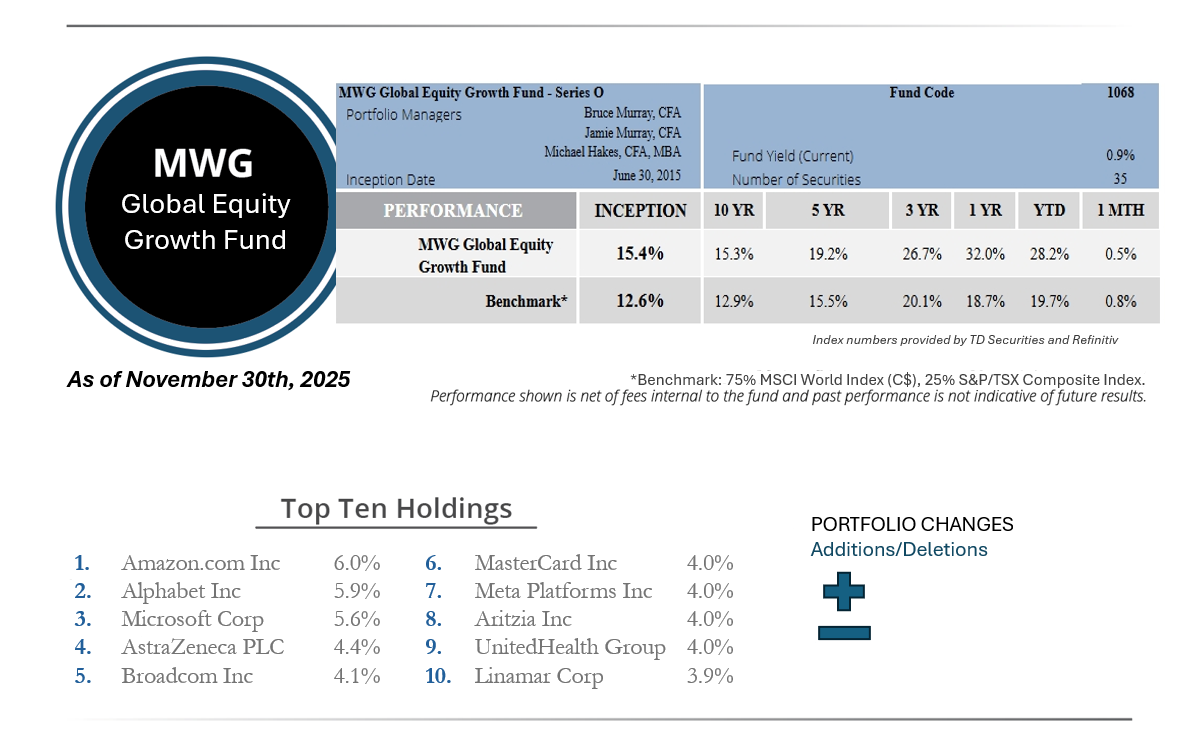

The MWG Global Equity Growth Fund Series O rose 0.5% in November, slightly behind the 0.8% rise in its benchmark and is now up 28.2% year to date. The Fund’s top three performers in the month were Eli Lilly (+24%), Alphabet (+13%) and Aritzia (+13%), while 3i Group (-28%), Hammond Power (-19%) and Docebo (-16%) were the largest detractors.

October 2025 Portfolio Review

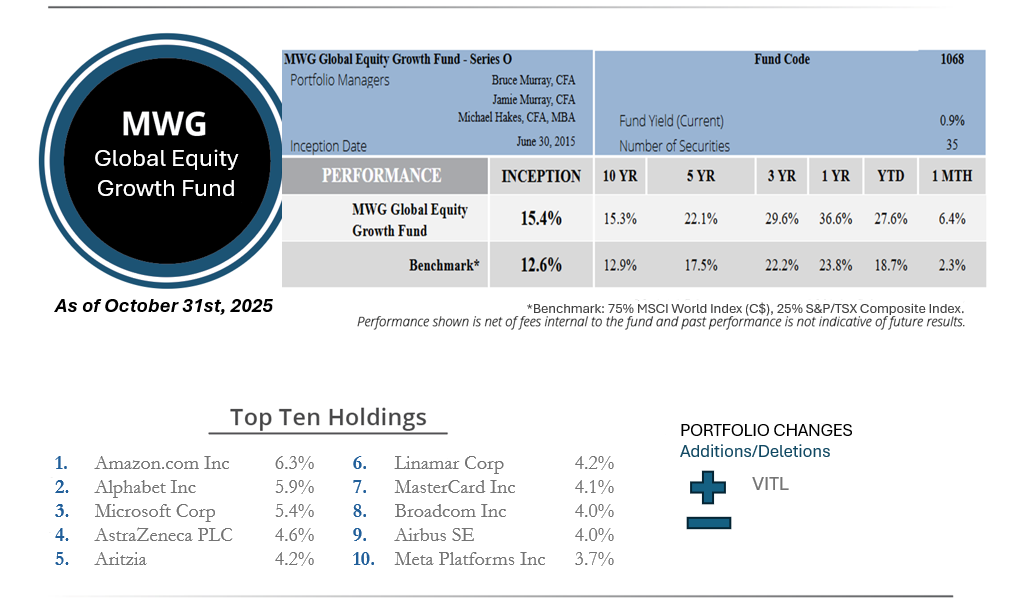

The MWG Global Equity Growth Fund Series O rose 6.4% in October, beating the 2.3% rise in its benchmark, and is now up 27.6% year to date. The Fund’s top three performers in the month were Hammond Power Solutions (+73%), Herc Holdings (+23%) and Thermo Fisher Scientific (+18%), while Meta (-11%), Docebo (-7%) and Aon (-4%) were the largest detractors.

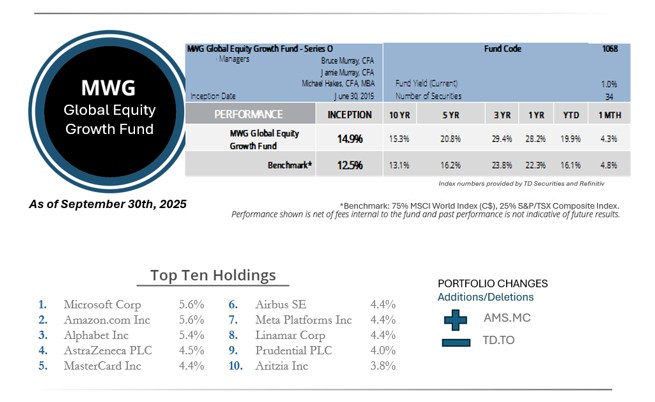

September 2025 Portfolio Review

The MWG Global Equity Growth Fund Series O rose 4.3% in September, slightly behind the 4.8% rise in its benchmark, and is now up 19.9% year to date. The Fund’s top three performers in the month were Hudbay Minerals (+29%), Major Drilling (+20%) and Alphabet (+16%), while Docebo (-11%), lululemon (-10%) and Air Canada (-10%) were the largest detractors.

August 2025 Portfolio Review

Read

Riding the Wayve: The impact of autonomous vehicles on Uber, Nvidia and Microsoft

As Waymo (An Alphabet/Google company), Tesla and Uber jockey for leadership in the high growth autonomous vehicle (AV) market, we continue to track the technological shifts shaping its rapid evolution. AV technology will affect several holdings in our Global Equity Growth Fund, but most exposed are our shares in Uber (currently a 3% weight in the Fund).

Read

Amazon: A Compelling Opportunity at an Unjustified Discount

In August, we increased our target weight for Amazon (AMZN) in our Global Equity Growth Fund to 6%, making it the largest single position in the portfolio. This decision is rooted in a significant dislocation in the market. Despite impressive top-line growth, Amazon’s stock has lagged its mega-cap peers. Since 2020, its shares have posted the lowest returns among the “Magnificent Seven” (ex-Nvidia, the remaining five members have averaged 143%), creating a valuation discount relative to both technology and retail competitors. We believe this discount is unwarranted, as Amazon’s growth outlook is superior to its peers, driven by two powerful and profitable engines: Amazon Web Services (AWS) and its maturing Retail and Advertising business.

Read

What’s NU? Why we bought Nu Holdings

Nu Holdings is our most recent purchase in our Global Equity Growth Fund. Nu Holdings (“Nubank”) has built its success on a simple but powerful concept: offer a no-fee, low-cost, credit card with an easy-to-use digital platform. Since its founding in 2013, this model has allowed the company to grow rapidly in Brazil, where it now serves over 50 million cardholders. By removing fees and focusing on user-friendly technology, Nubank has become the go-to bank for millions of people who were underserved by traditional banks.

Read

Our thesis on Power Corporation

Read

Eli Lilly (LLY) — Investor Visit Recap: What Matters Now

Read

The Long-Term View on Chemtrade Logistics Income Fund

By: Jamie Murray, CFA

Chemtrade Logistics Income Fund (CHE.UN) is a compelling, under-the-radar turnaround story that we believe is deeply misunderstood by the market.

The company produces essential chemicals used in a wide range of industries. The company’s products are the “boring but essential” chemicals that are critical for everything from disinfecting drinking water and manufacturing paper to refining gasoline and producing high-value semiconductor equipment. The stability of these end-markets, together with Chemtrade’s operational capabilities, forms a durable foundation for its business.

Read

Why we bought Hammond Power Solutions

We have been accumulating Hammond Power Solutions stock since April as a long-term play on the rising demand for electrical infrastructure that is being driven by Artificial Intelligence (AI) and the electrification of transportation. As a leading manufacturer of dry-type transformers in North America with a reputation built over a century, HPS is well-positioned for the future.

Read

Why we bought PHX Energy Services

In June 2025, we initiated a position in PHX Energy Services for the Income Growth Fund, following our second meeting with the company’s highly experienced management team within the year. The company’s founder, John Hooks, remains Executive Chairman, and both the current CEO and CFO have been with PHX since the late 1990s. This long-tenured leadership is a distinct advantage in that it provides the company with significant stability and deep industry knowledge.

Read

Canada’s Gas Superstar: Why we bought Tourmaline Oil Corp.

By: Bruce Murray

We recently purchased shares in Tourmaline Oil Corp. in our Global Equity Growth Fund. Founded in 2008 by Mike Rose, one of Canada’s most astute energy entrepreneurs, Tourmaline (TOU.TO) has rapidly grown into Canada’s largest producer of natural gas and a leading owner of midstream gas processing facilities.

Read

On our Radar: The Genius Act, Stablecoins, and Their Impact on Payment Networks

Read

Three Earnings Reports to Watch

As earnings season gets into full swing, investors will be closely monitoring reports from several key companies. We understand that quarterly earnings provide a momentary snapshot of business performance and always take a long-term view of three to five year earning power and valuation. However, not all earnings reports carry the same weight. This quarter, some reports are more than just a scorecard; they’re potential turning points. For the companies below, which are facing leadership changes and fundamental threats to their business models, these results should help shape the investment narrative going forward.

Read

MWG Focus Stock: Kingfisher PLC: An update with Kingfisher

Thoughts on the Market: June Edition

GLOBAL EQUITY GROWTH FUND

The MWG Global Equity Growth Fund Series O rose 5.7% in June, beating the 3.4% rise in its benchmark, and is now up 8.8% year to date. The Fund’s top three performers in the month were Hammond Power Systems (+27%), Hudbay Minerals (+18%) and Nvidia (+16%), while Accenture (6%), Adyen (-5%) and Aon (-5%) were the largest detractors.

Portfolio Managers’ Summary

Markets continued their sharp rebound from the April tariff tantrum this past month, led by AI enablers such as Nvidia, Meta, Qualcomm and Broadcom, all of which returned +10% in June, as well as beneficiaries of capital investment in data centers like electrical systems company Hammond Power Systems.

Copper prices also approached record levels, benefiting mining companies Hudbay and Major Drilling. Major Drilling indicated that major global miners will raise exploration spending by 20% year-over-year, which should provide a good tailwind for revenue.

During the month, we started a position in Tourmaline while exiting our position in Whitecap.

INCOME GROWTH FUND

The MWG Income Growth Fund Series O increased 3.0% in June, in line with the 3.2% return for its benchmark. The Fund is up 5.4% year-to-date. Kering (+10%), Exchange Income (+9%) and Whitecap Resources (+8%) were the top performers, while PHX Energy Services (-7%), Enbridge (3%) and Rio Tinto (-3%) were the top detractors. The Fund’s yield was 5.9% at month-end.

Portfolio Managers’ Summary

Ongoing war and geopolitical turmoil in the Middle East led to a resurgence in the energy sector in June, following a weak pricing period after OPEC announced plans for higher output levels.

The Canadian Dollar has increased from multi-year lows in winter 2025 as tariff concerns eased and the US Dollar weakened globally. We believe lower tariffs and a stronger Canadian dollar will set up the Bank of Canada for additional interest rate cuts this fall. This should benefit companies that pay sustainable and growing dividends like those in the fund.

In June, we added a very small starter position in PHX Energy Services, a leading drilling services contractor with a 9% yield.

This Month’s Portfolio Update is written by our Head of Research, Jamie Murray, CFA.

The purpose is to provide insight into our portfolio construction and how our research shapes our investment decisions. As always, we welcome any feedback or questions you may have on these monthly commentaries.

Thoughts on the Market: May Edition

The “One, Big, Beautiful Tax Bill” narrowly passed Congress and is now in the Senate. Many Canadian investors are understandably concerned with tax treaty changes that could mean higher withholding taxes paid on U.S. source dividends. While the urge to (again) sell U.S. holdings and move investments back home is pervasive, we believe time is on our side. Consider the following:

Read

Thoughts on the Market: April Edition

What a difference a tweet makes.

Tariffs went global at the start of April, with “Liberation Day” swiftly turning into “Liquidation Day.” The selloff between April 2-8 was one of the sharpest in history as the S&P 500 fell 14.7% in two trading sessions and the intraday move at the open of April 8. This was quickly reversed by an announcement of a 90-day pause on reciprocal tariffs on all countries but China. We provided an update on our market thoughts in our April 4 Investor Update, which argued that cooler heads would prevail, and our April 17 update, which highlighted the opportunity that comes when buying extreme fear as indicated by the VIX. Thus far, these appear prescient as the S&P 500 went on to record its longest daily winning streak since 2004. Moving forward, we expect the market to continue climbing higher as companies are indicating that the tariffs are either manageable or likely to be revised for key industries if deemed untenable.

Thoughts on the Market: March Edition

The trade war has gone global. It appears that Trump is following the same playbook with his overseas contemporaries as he did with his North American ones. Step 1 is creating a fake national emergency to enact executive legislative powers (Canada & fentanyl, Europe/Asia & trade deficits). Step 2 is proposing egregiously high tariff rates. Step 3 is delaying at the eleventh hour, as we just witnessed with a 90-day implementation pause on all countries… except China. This aligns with the view we expressed in our note to clients on April 4, 2025, as we believe the U.S. will need and want support from allies to isolate China.

Thoughts on the Market: February Edition

As the Canadian economy and companies are under the threat of tariffs, markets entered March with the expectation that tariffs would not be widely applied. However, there was an acknowledgment that policy uncertainty is a growing risk within the economy. For instance, on February 28, U.S. Treasury Secretary Bessent indicated that Canada and Mexico should impose tariffs on Chinese goods in conjunction with the U.S. This followed President Trump’s announcement of tariffs on Canada two days earlier, tariffs that had initially been set for April 2, then moved to March 4. As of this writing, USMCA goods are exempt until April 2, with additional steel and aluminum tariffs (for all countries) slated to take effect on March 12, 2025.

Thoughts on the Market: January Edition

Justin Trudeau may be nearing the end of his tenure with a new Liberal leadership race in progress and a federal election on the horizon, yet his recent actions deserve recognition. In the face of a February 4th threat from the United States of widespread tariffs on Canadian exports, Trudeau decisively called the bluff. Following Canada’s announcement of plans for counter-tariffs, the U.S. quickly retracted its proposal and extended the deadline by a month. While the possibility of a tariff war remains, with nothing off the table when it comes to President Trump – the post hoc comment by U.S. economic officials, “This isn’t a trade war, this is a drug war,” comes across as particularly hollow given previous remarks about trade deficits and references to a “51st State.” It likely won’t be long before policymakers shift their focus to Europe, where tax policy issues could take precedence, potentially sparing Canada from broad tariff measures for the time being.nt policy, will likely be dilutive to equity holders.

December Portfolio Update | 2024

Thoughts on the Market: December Edition

We closed out 2024 with a second consecutive annual return of 25% for the benchmark S&P 500. As in 2023, size mattered, as evidenced by the 62% return for the ten largest companies in the Index. The other 490 companies, which still include some big winners like Walmart (+73%), Netflix (+88%), GE (+66%) and American Express (+40%), to name a few, rose 12% on average. The market exited the year with a P/E ratio of 21x. Read

November Portfolio Update | 2024

Thoughts on the Market: November Edition

Trump 2.0

The sweeping Republican win in the United States election was a clear signal that voters demand change. Despite numerous reasons not to vote for Trump, the vote shifted red across most of the country. Figure 1 illustrates this shift in margin in terms of raw votes. Notably, large metro centers like New York City, Southern California, Chicago, Houston, Miami, and Minneapolis are some of the darkest red areas on the map. Please see the full article from NPR.

October Portfolio Update | 2024

Thoughts on the Market: October Edition

Interest Rates are down. Interest Rates are up.

The U.S. interest rate cuts widely telegraphed by the Federal Reserve began in earnest in September with a 50 basis point cut (50 basis points, or bps, is equal to 0.5%) to the overnight rate, followed by a 25 bps cut in early November. Overnight rates are the rates the Fed and other central banks use to achieve their monetary goals and drive floating rate products like prime rate and variable rate mortgages After two years of elevated overnight rates, the decrease has brought some reprieve to short-term holders. Additional rate cuts will flow through as they occur.

September Portfolio Update | 2024

Thoughts on the Market: September Edition

Equity markets charged ahead in September, reaching all-time highs, thanks to a broad-based rally that saw 8 out of 10 sectors end the month higher. It was a welcome reprieve from more typical recent September market performance, as the past four Septembers have been decisively negative across North American equity markets (Figure 1).

Figure 1: September Returns were poor between 2020-2023

Source: MWG, Refinitiv Workspace

Markets are looking for further evidence of a soft landing, a scenario where employment remains strong and inflationary pressures fade. Under this scenario, The U.S. Federal Reserve could maintain a measured pace in lowering overnight funding rates, slowly taking its foot off the economic brake pedal but finding some comfort in inflation expectations l remaining subdued. The September U.S. jobs market update highlighted a slight rebound in labour conditions as evidenced by the unemployment rate falling from 4.2% to 4.1%.