Global markets repriced quickly in March as geopolitical tensions resurfaced, driving volatility across asset classes and bringing energy markets back into focus. While these developments created short-term pressure, they also reinforced a more important and longer-term reality: not all regions are equally positioned in a supply-constrained world.

Disruptions to global energy flows highlighted how dependent many economies remain on external supply. In parts of Europe and Asia, this translated quickly into rising costs, supply strain and early signs of rationing. What appears as volatility in markets is, in many regions, a structural constraint.

By contrast, the Americas remain structurally advantaged. North and South America benefit from energy production capacity that exceeds internal demand, positioning the region as a net supplier in a tightening global system. Canada and the United States, alongside Brazil, Guyana and Mexico, are uniquely positioned in a resource-constrained world.

This advantage extends beyond hydrocarbons. The region holds significant reserves in natural gas, critical minerals, agriculture and freshwater. In a world increasingly defined by supply shocks, these factors matter. Despite ongoing political noise, North America remains one of the most resilient regions globally.

Market Outlook

March reinforced how quickly markets adjust when supply constraints emerge. Higher energy prices are now acting as a constraint on global growth and complicating the path forward for central banks. Inflation expectations have moved higher, reducing the likelihood of near-term rate cuts and reinforcing a higher-for-longer rate environment.

At the same time, underlying economic activity remains supported by sustained government spending, particularly in defense and technology. This combination continues to support long-term demand, even as macro conditions remain uncertain. Our approach remains disciplined. We focus on businesses aligned with structural growth drivers while managing exposure to short-term volatility.

Market Update

North American equity markets declined in March as investors pulled back from risk. The S&P 500 fell approximately 5 percent, led by weakness in large-cap technology names. The S&P/TSX Composite Index also moved lower, giving back some of February’s gains despite strength in energy.

Commodity markets were the focal point of volatility. Oil surged in response to tightening supply conditions, while gold, after reaching elevated levels earlier in the year, corrected as investors took profits and the market consolidated. In fixed income, yields moved higher as markets adjusted to persistent inflation and the likelihood of sustained higher rates.

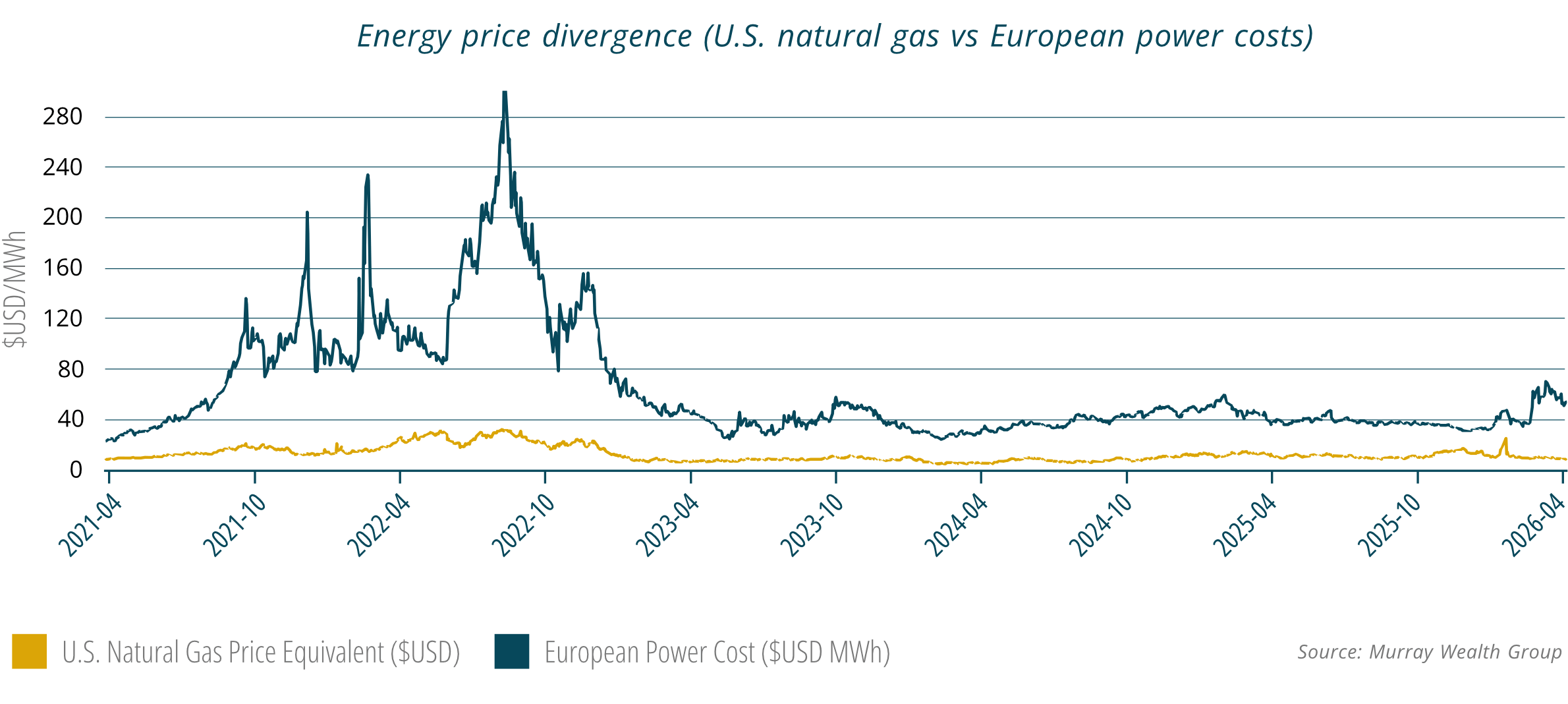

Figure 1. Energy price divergence (U.S. natural gas vs European power costs) highlighting structural supply advantages in North America.

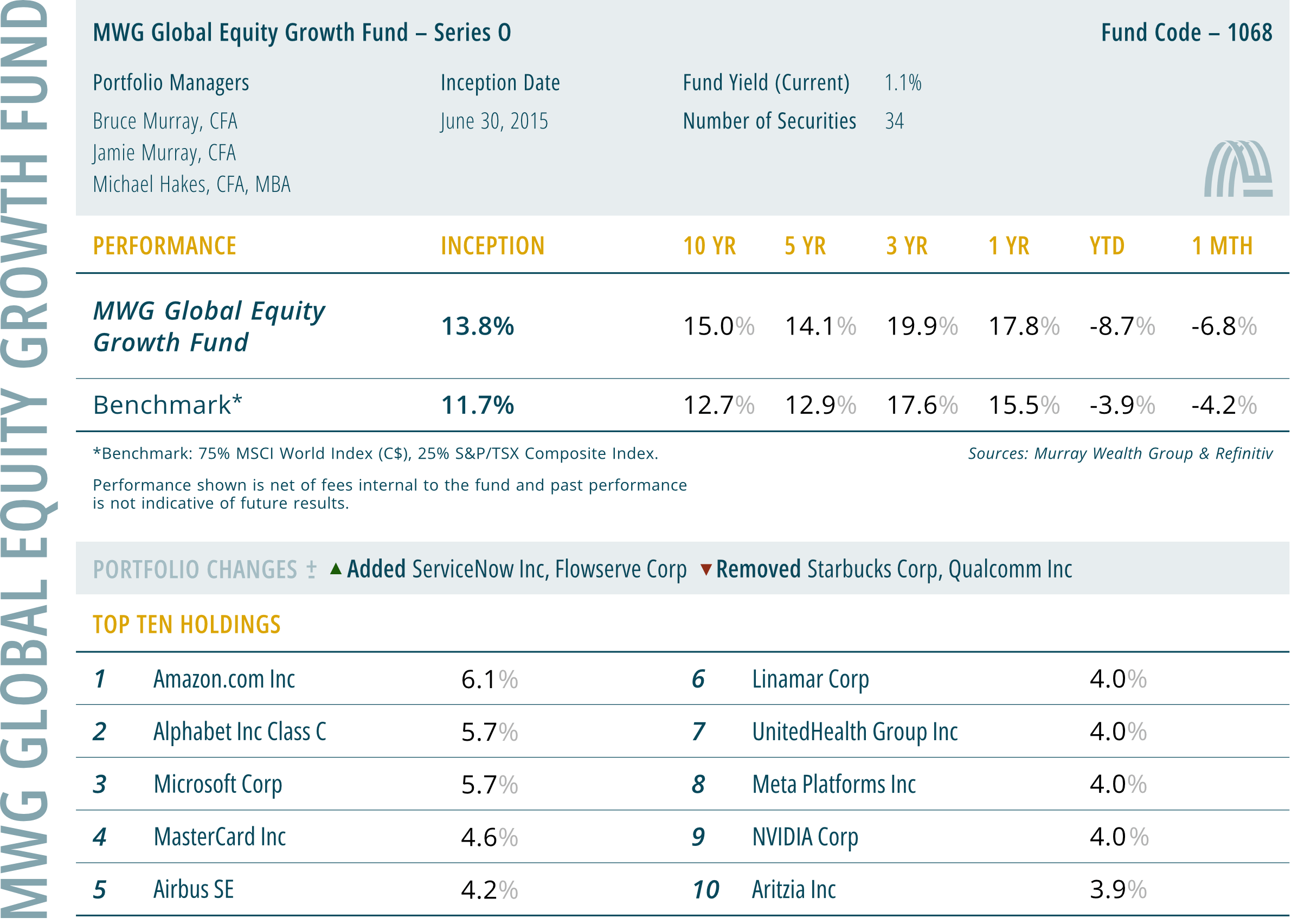

MWG Global Equity Growth Fund

The MWG Global Equity Growth Fund Series O declined 6.8 percent in March, compared to a 4.2 percent decline in the benchmark. The fund was down 8.7 percent year-to-date, compared to a 3.9 percent year-to-date return in the benchmark. Performance was supported by Tourmaline Oil (+5%), Amazon (+1%) and Flowserve (+1%). Detractors included Vital Farms (-31%), Herc Holdings (-27%) and 3i Group (-27%).

Figure 2. MWG Global Equity Growth Fund performance versus benchmark.

Portfolio Manager’s Summary

While March performance reflected broader market pressure, underlying business fundamentals remain intact. Early April data points continue to show acceleration in artificial intelligence investment, reinforcing one of the most important long-term growth drivers in the portfolio.

Certain cyclical exposures, including Air Canada and Herc Holdings, remain more sensitive to near-term economic conditions. However, the majority of holdings continue to demonstrate resilience, supported by strong positioning and durable demand.

We added two new positions during the month. ServiceNow was initiated following a meaningful pullback, creating a more attractive entry point for a business deeply embedded across enterprise systems. As AI adoption expands, we expect long-term usage and revenue growth to follow. We also added Flowserve, a leader in industrial flow control systems serving LNG, nuclear and refining industries, with strong recurring aftermarket revenue and clear margin expansion potential.

To fund these additions, we exited Starbucks and Qualcomm, where risk-reward dynamics became less favourable.

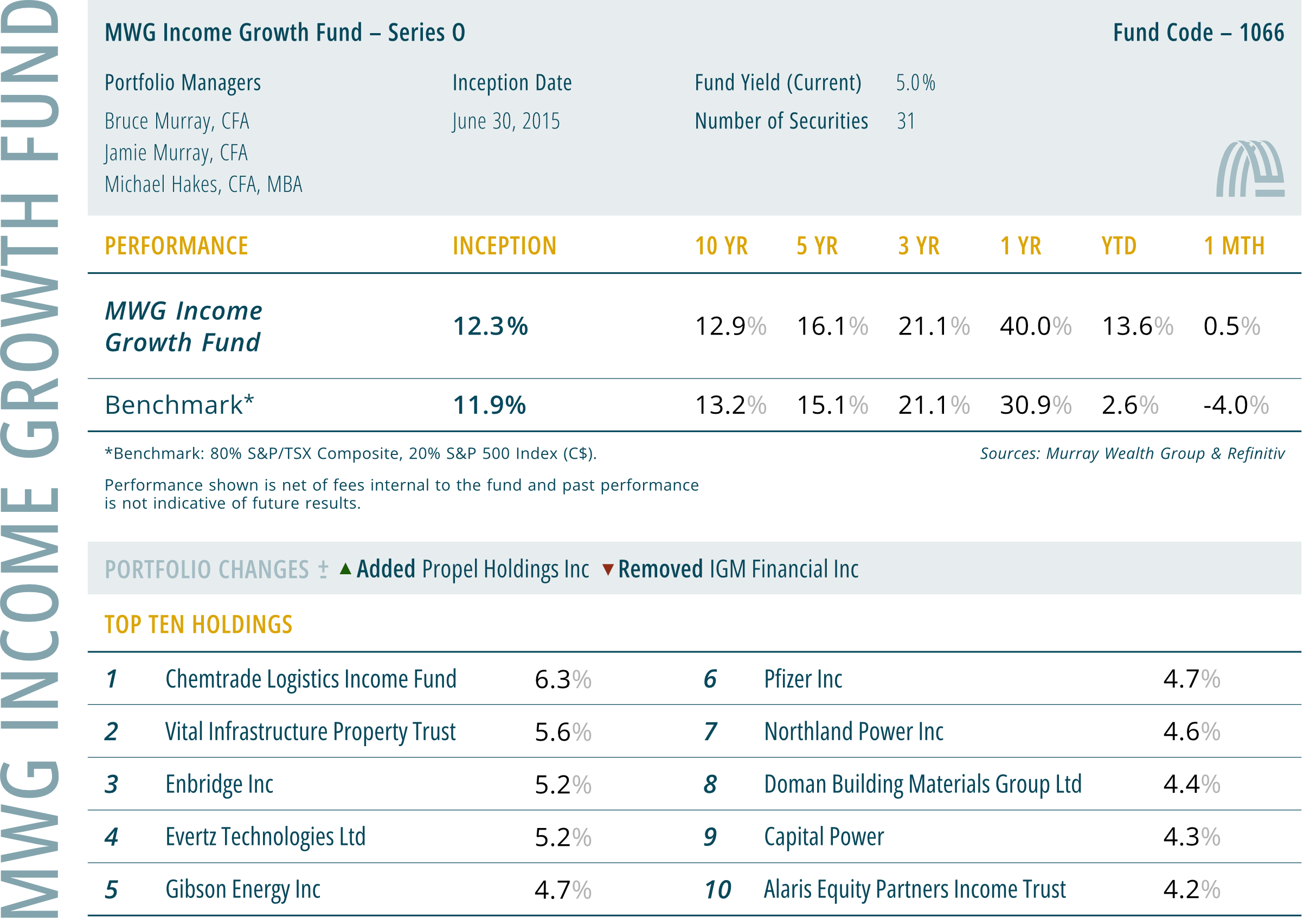

MWG Income Growth Fund

The MWG Income Growth Fund Series O rose 0.2 percent in March, outperforming the benchmark decline of 4.0 percent. The fund delivered a year-to-date return of 13.6 percent, compared to 2.6 percent in the benchmark. Strong performance was driven by BP (+24%), Whitecap Resources (+16%) and Canadian Natural Resources (+15%). Weakness was seen in Kingfisher (-23%), Opera (-9%) and IGM Financial (-8%).

The fund continues to benefit from exposure to hard assets, which provided stability during market volatility, offsetting weakness in more interest-sensitive sectors such as real estate and technology.

Figure 3. MWG Income Growth Fund performance versus benchmark

Portfolio Manager’s Summary

The Income Growth Fund remains well aligned with current conditions. Energy exposure continues to provide stability in a constrained global supply environment, while selective positioning supports long-term income generation and capital appreciation.

March reinforced how quickly markets can reprice risk when conditions shift. In this environment, discipline remains critical. Portfolio construction, valuation awareness and a focus on durable demand drivers continue to guide our approach.

We initiated a position in Propel Holdings, a specialized lender focused on underserved borrowers in the U.S. and U.K. markets. The company maintains a highly selective underwriting model and operates primarily in regions with more favourable regulatory conditions.

Recent weakness, driven in part by sentiment toward peers, created an attractive entry point. We believe Propel is well positioned to achieve its targeted earnings growth, supported by strong demand fundamentals and disciplined risk management. To fund this position, we exited IGM Financial while maintaining indirect exposure through Power Corporation.