Market Priced Higher; Watch the Fed; Tech Continues to Eat the World; Five BOLD Predictions.

Below we present major themes we believe will be in focus for 2020 as well as some fun predictions. We still do not see any storm clouds on the Horizon and could even see the global economy accelerate with easing trade tensions and if China has indeed bottomed.

We expect more muted but positive returns in 2020 after the large rally experienced by equity markets in 2019. While we believe there is upside to forecast S&P 500 earnings growth range of 5-9% (depending on the estimate), valuations are high. The P/E ratio of the S&P 500 is close to peak levels seen in 2018, although there is likely even more bifurcation between the multiples of growth and value stocks (Figure 1).

Figure 1: S&P 500 P/E Forward Multiple

A quick comparison between our Global Equity Growth portfolio and the S&P 500* highlights the opportunities we are finding the market. Despite a forward P/E ratio nearly four turns lower, we can achieve substantially similar EPS growth. Thus we believe our portfolio may have similar upside from earnings growth as well as expansion on the P/E multiple side.

Figure 2: Global Equity Growth multiples and earnings growth versus the S&P 500.

*Our published benchmark for the Global Equity Growth Fund is 75% MSCI World and 25% TSX Composite Index. Our comparison with the S&P is to highlight the relative attractiveness of the portfolio versus a widely followed index

Of course, the ebbs and flows of the market will be determined by a multitude of factors, such as Federal Reserve policy, GDP growth and trade deals. Let’s take a look at a few key themes to watch moving forward.

Federal Reserve Policy

The Fed flipflopped on its hawkish position in early 2019, reversing course on its interest rate hikes and ended up lowering the Fed Funds rate three times to its current range of 1.50-1.75%. This reversal likely caused the strong rebound in equities in the first half of 2019. More recently, in September, the Fed began purchasing Treasuries to support the repo market, an overnight lending market for financial companies. This has reversed the Fed’s balance sheet runoff and functioned as extra liquidity in financial markets. We suspect part of the October run in U.S. equities is due to this balance sheet expansion. The Fed has committed to support the repo market through April, but there is value in monitoring the actions with respect to finding clues for the market.

Figure 3: Federal Reserve Assets Held on Balance Sheet is expanding after an 18 month run-off

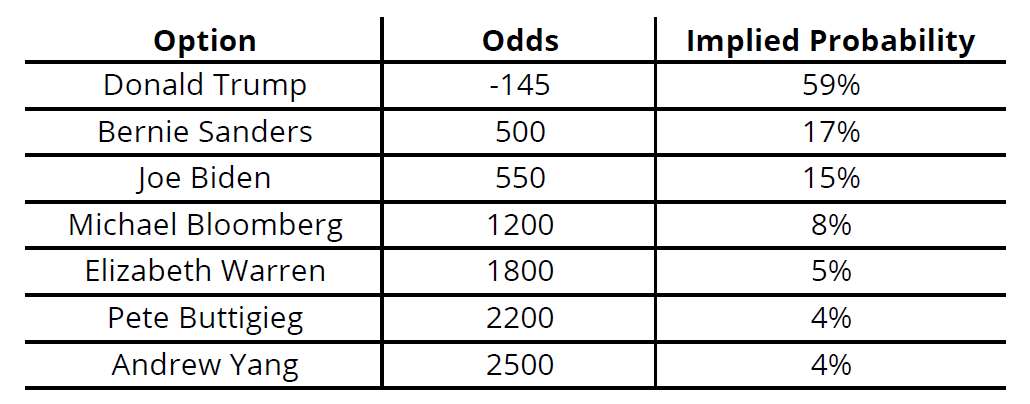

The Presidential Race

We will be following the betting lines for the presidential race as we move through the year as the eventual winner will likely have significant sway over the direction of the markets short term.

Figure 4: Betting lines for 2020 US Presidential Election.

We see three broad outcomes:

Trump victory. A Trump victory would likely be viewed positively by the stock market as it means a continuation of current policies, which have been supportive of higher stock market conditions (literally the ‘Devil You Know’ in this case). Trump is reportedly gearing up for another large tax cut for American corporations, which was the primary driver of the strong 2017 market rally and this would have a positive effect once again.

Biden/Bloomberg victory. If a moderate were to win the Democratic nomination, it would represent a strong de-risking event. While naturally moving towards more liberal policies, we believe either victor would still be friendly to corporations, with environmental policies likely seeing the most reform. As well, a Biden-led government would harken back to the Obama years, where markets rallied strongly, with only Obamacare policies significantly disrupting corporate profits.

Sanders/Warren. In our opinion, this would be the most negative outcome for equity markets. Either Sanders or Warren would likely look at tax, healthcare and technology reform as well as increased regulation of financial services.

Tech Continues to Eat the World

Google, Amazon and Facebook continue to re-invest in organic growth as large acquisitions are off the table due to anti-trust concerns. Capital spending plans of the majors are quite staggering, with Google, Amazon, Facebook and Microsoft projected to spend US$83B in 2019, up from about US$32B in 2017. While some of this money is undoubtedly aimed at ‘moonshot’ bets such as autonomous vehicles and augmented reality use cases, we expect the majority to be directly related to capacity growth and revenue-generating offshoots of existing apps or features.

Therein lies the beauty of internet-based technologies. With four billion people connected to the internet through home or mobile, capital spending can be leveraged over the entire population. Twenty years ago, in the dot com boom/bust, many products were aimed at PC or enterprise usage. Now, a new feature added to Instagram’s shopping commerce page can be utilized by the 150 million small businesses on Instagram to sell to its 1 billion users. Alphabet can add new features to increase its users’ dependability on Google Maps, and by getting more screen time, can eventually charge more for advertising when it decides to monetize the platform. Along with a host of smaller software companies that are solving individual pain points for millions of users, we believe technology will continue to be the growth engine of the U.S. market.

Figure 5: Capital Spending Projections

Five BOLD Predictions from the Murray Wealth Team

- Boeing 737 Max Remains Grounded Through Summer (Bruce). The FAA clearly did not do proper due diligence on the Plane. Extra caution is applied during the approval process as there are now rumours of wiring and engine issues. As well, cutbacks at the FAA itself may add to delays. This will allow high volume, low fare airlines to increase their fares as capacity growth is constrained.

- Donald Trump does a 180 on climate change after his Mar-Lago Resort is impeached by fall hurricanes (Mike). After rolling back a significant number of environmental policies over his first term, Trump changes tones with a single tweet.

- Amazon spins off AWS, its cloud infrastructure services business (Jamie). Tired of ceding market share to Microsoft and Google, Amazon spins out AWS to shareholders. Amazon Web Services is the leading cloud provider, with a 60% market share, but this figure has fallen from 78% three years ago as customers fear Amazon will use their own data against them and expand into their turf.

- Tapestry and Capri holdings merge to form a Global Affordable Luxury powerhouse (Mike) with brands Coach, Michael Kors, Kate Spade, Jimmy Choo, Versace and Stuart Weitzman. The reduced competition leads to greater efficiency and pricing power.

- The Maple Leafs win their first Stanley Cup in 51 years, beating the Colorado Avalanche in the final! (Jamie). We said BOLD, right?

The Murray Wealth Team wishes you all the best in 2020!

How Did We Do in 2019?

For completeness, let’s quickly review our 2019 outlook and examine how we did. Of course, our outlook is only relevant in the context of making our clients’ money so that is the lens through which we will view our predictions.

Click on the button below: