Thoughts on the Market: October Edition

Are we there yet?

Despite a good earnings season, markets moved lower in October on high expectations in the tech sector and deflated optimism regarding the reopening trade. Whether it was also the stalled stimulus deal, the resurgent second wave of COVID-19 or election night jitters is up for debate, but as we move through another winter with COVID-19 case counts rising, the market is priced for uncertainty.

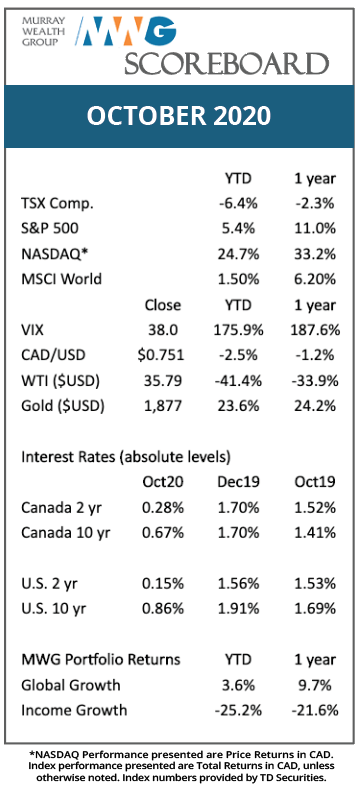

The Volatility Index (VIX, a measure of risk) rose to 38, an extreme level seen only in times of market duress. While the sell-off from Oct 14 to month-end approached 8%, companies have adapted business plans to survive in a COVID world and are better able to transact online. Thus, additional lockdowns won’t be the death knell for most companies, which have likely seen the worst in Q2/20. Those most affected will likely survive and thrive on the reopening.

The major tech companies all reported earnings during the month, and despite some mixed market reactions, we viewed the results as strong. Facebook and Google both reported better than expected revenue and are seeing growth re-accelerate post the COVID disruption. Amazon delivered $96B in sales and is set up to generate revenue of $450B in 2021 through its expanded logistics network. Microsoft’s cloud computing business, Azure, continues to grow +40% despite a $25B run rate of revenue. These are astounding numbers and they do not appear to be slowing down.

One area of continuing concern is the commercial real estate market. Urban office buildings remain largely deserted as the work-from-home ritual becomes more ingrained. With widespread vaccination still 9-12 months away, the comfort and convenience of the home office will remain more appealing to a segment of the population. Commercial lending is a large market, and with a big proportion being non-recourse debt (loans secured by a property or asset versus the whole company), additional pressure in this market is possible as lender patience and forgiveness wear thin. Office markets can take a long time to recover, and thus, we expect additional negative news from this sector.

GLOBAL EQUITY GROWTH FUND

The MWG Global Equity Growth Fund rose 0.7% in October, outpacing our benchmark by 3% and bringing its year-to-date return to 3.6%. Over the past twelve months, the portfolio has returned 9.7%. The top performers in October were Tapestry (+42%), Stelco (+28%), and Alliance Data (+23%), while Mastercard (-14%), Royal Caribbean (-13%) and Aon (-10%) were the laggards during the month.

We purchased additional shares in Stelco after a compelling presentation from its CEO. Stelco has a very clean balance sheet thanks to its 2017 restructuring. Moreover, the company’s reinvestment in its facilities has resulted in one of the most cost-efficient operations in North America. With a cost base of $400/ton, Stelco should be able to provide good full-cycle returns in what is a volatile industry. The quick math behind our $28 target price (current price is $14.50) is approximately $200/ton of profit for its 3 million tons of annual steel capacity if steel prices average $600/ton. This equates to $600M of cash flow. At 5x cash flow, Stelco would be valued at $3B vs. $1.5B today. As a kicker, the company holds a large land parcel adjacent to its Hamilton Works Steel Operation that is well-positioned for industrial real estate development and could be worth up to $5 per share.

INCOME GROWTH FUND

The MWG Income Growth Fund rose 1.2% in October, bringing its year-to-date return to -25.2%. Over the past twelve months, the portfolio has returned –21.6%. The top performers in October were Tapestry (42%), Chorus Aviation (32%) and Corus Entertainment (22%). The largest negative impacts were from BP (-11%), Restaurant Brands (-9%) and Gibson Energy (-9%).

The Income Growth portfolio continues to be negatively impacted by the economic effects of COVID-19 and the “hard” asset nature of the portfolio. Nevertheless, we believe our companies are financially strong and will rebound as economic activity normalizes. In the interim, the portfolio yields 6.3%.